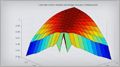

Multiperiod Goal Based Wealth Management Using Reinforcement Learning

Determining the asset allocation of a fund is not a trivial task, particularly over longer time horizons and in a multiperiod portfolio rebalancing framework. Traditional approaches used to solve the optimal asset allocation are often based on strong model assumptions. Reinforcement learning is an area of machine learning where the portfolio problem can be defined with greater flexibility, and that may help produce better trading and asset allocation strategies.

This talk demonstrates how reinforcement learning can be used to solve a multiperiod asset allocation problem. We show how MATLAB® can be used to:

- Define portfolio wealth states and reinforcement learning actions from a frontier of portfolio strategies

- Model reward functions and train Q-learning and custom agents

- Simulate portfolios with the trained agents within specified environments

Published: 7 Nov 2023