计算金融

通过将 Deep Learning Toolbox™ 与 Financial Toolbox™、Financial Instruments Toolbox™、Econometrics Toolbox™ 和 Risk Management Toolbox™ 结合使用,将深度学习应用于金融工作流,包括产品定价、交易和风险管理。

精选示例

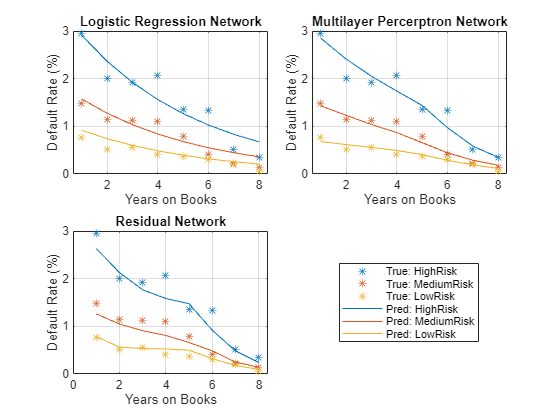

Compare Deep Learning Networks for Credit Default Prediction

Create, train, and compare three deep learning networks for predicting credit default probability.

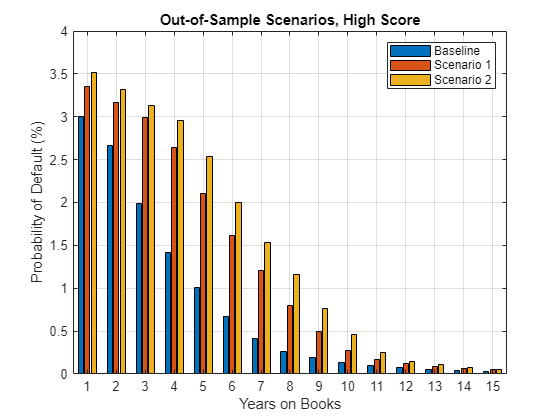

Interpret and Stress-Test Deep Learning Networks for Probability of Default

Train a credit risk for probability of default (PD) prediction using a deep neural network. The example also shows how to use the locally interpretable model-agnostic explanations (LIME) and Shapley values interpretability techniques to understand the predictions of the model. In addition, the example analyzes model predictions for out-of-sample values and performs a stress-testing analysis.

Hedge Options Using Reinforcement Learning Toolbox

Outperform the traditional BSM approach using an optimal option hedging policy.

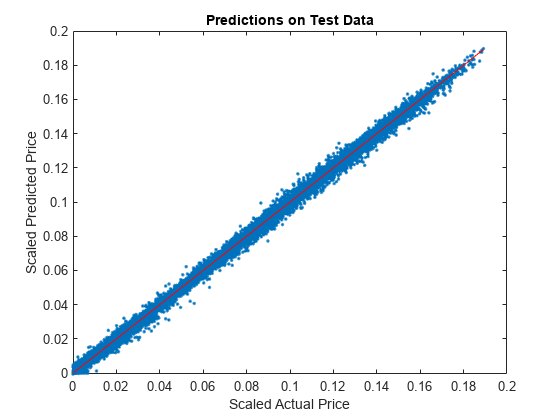

Use Deep Learning to Approximate Barrier Option Prices with Heston Model

Use Deep Learning Toolbox™ to train a network and obtain predictions on barrier option prices with a Heston model.

Backtest Strategies Using Deep Learning

Construct trading strategies using a deep learning model and then backtest the strategies using the Financial Toolbox™ backtesting framework. The example uses Deep Learning Toolbox™ to train a predictive model from a set of time series and demonstrates the steps necessary to convert the model output into trading signals. It builds a variety of trading strategies that backtest the signal data over a 5-year period.

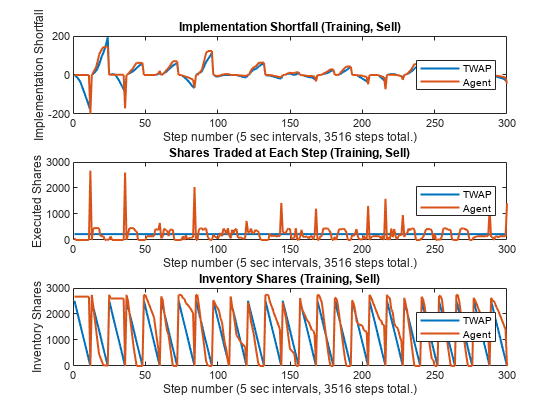

Deep Reinforcement Learning for Optimal Trade Execution

Use the Reinforcement Learning Toolbox™ and Deep Learning Toolbox™ to design agents for optimal trade execution.

Multiperiod Goal-Based Wealth Management Using Reinforcement Learning

A reinforcement learning (RL) approach to maximize the probability of obtaining an investor's wealth goal at the end of the investment horizon. This problem is known in the literature as goal-based wealth management (GBWM). In GBWM, risk is not necessarily measured using the standard deviation, the value-at-risk, or any other common risk metric. Instead, risk is understood as the likelihood of not attaining an investor's goal. This alternative concept of risk implies that, sometimes, in order to increase the probability of attaining an investor’s goal, the optimal portfolio’s traditional risk (that is, standard deviation) must increase if the portfolio is underfunded. In other words, for the investor’s view of risk to decrease, the traditional view of risk must increase if the portfolio’s wealth is too low.

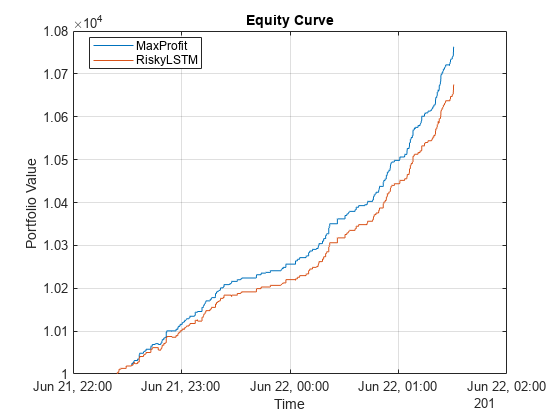

Backtest Deep Learning Model for Algorithmic Trading of Limit Order Book Data

Apply a backtest strategy to measure the performance of a long short-term memory (LSTM) neural network, which is trained and validated on limit order book (LOB) data of a security.