Framework for Standardized Approach to Calculating Counterparty Credit Risk: Introduction

The Standardized Approach for Counterparty Credit Risk (SA-CCR) is a framework determining the exposure at default (EAD) of derivative contracts for regulatory capital purposes. SA-CCR determines the EAD through a series of calculations that include:

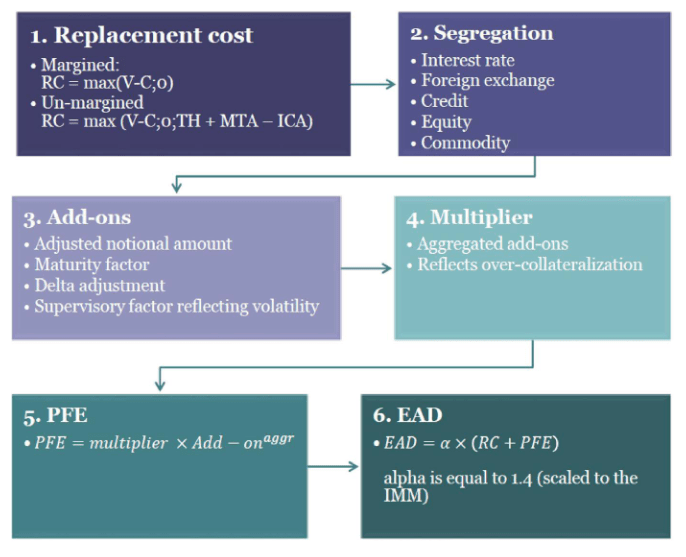

Replacement cost — The current value of the derivative contract if it is in-the-money (positive value). For out-of-the-money contracts (negative value), the replacement cost (RC) is zero. The RC represents the immediate cost that would be incurred if the counterparty were to default.

Asset class segregation — Derivatives are categorized into different asset classes, such as interest rate, credit, equity, foreign exchange, and commodities. Each asset class has its own set of risk factors and supervisory factors that are used to calculate the Add-on.

Add-ons — This component accounts for potential future exposure (PFE) due to changes in market factors affecting the value of the derivative contract over its remaining lifetime. The Add-on is calculated based on asset class-specific parameters provided by the regulatory framework.

Multiplier — The factor is applied to the sum of the RC and Add-on to account for the potential that the exposure may be underestimated. The regulatory value of alpha is fixed at 1.4.

PFE — Potential Future Exposure (PFE) is an estimate of the increase in exposure to a counterparty in a derivative transaction that could occur over the remaining life of the contract due to changes in market conditions.

EAD — Once the RC and the Add-on are calculated, they are combined with the alpha multiplier to determine the exposure at default (EAD), which is then used in the calculation of regulatory capital requirements.

Derivative instruments are financial tools whose value is derived from another asset or group of assets, known as the underlying. They are primarily used to hedge risks associated with these underliers, as changes in the underlying's value directly affect the derivative's value. Counterparty credit risk is the risk that a party in a derivative transaction may default on its obligation before final settlement. This risk, creating off-balance sheet exposures, must be quantified as EAD for capital adequacy calculations.

The formula for EAD is

where:

alpha is

1.4.RC is the replacement cost.

PFE is the amount for potential future exposure.

SA-CCR Transactional Elements

For an explanation of the elements of the SA-CCR as a regulatory framework, see SA-CCR Transactional Elements.

ISDA SA-CCR CRIF

International Swaps and Derivatives Association (ISDA®) SA-CCR Common Risk Interchange Format (CRIF) is designed to facilitate the exchange of counterparty credit risk information between market participants and regulatory authorities. For more information, see ISDA SA-CCR CRIF File Specifications.

SA-CCR Workflow

To implement the SA-CCR framework using Financial Instruments Toolbox™, use this workflow:

Create an ISDA SA-CCR Common Risk Interchange Format (CRIF) data file.

Create a

saccrobject.Compute replacement costs using

rc.Compute Add-ons for additional factors applied to PFEs using

addOnandaggregate.Compute PFEs and multipliers using

pfe.Compute EADs using

ead.Aggregate results using

aggregateandaggregateByCounterparty.

Data for SA-CCR Examples

The data contains the following trades:

Tr001— Asset class (IR), 10 Year Interest Rate Swap in EURTr002— Asset class (FX), EUR/GBP Forward FX Swap (Trade Decomposition "1b")Tr003— Asset class (CR_SN), Single name CDS on Spain (Short Protection)Tr004— Asset class (CR_IX), CDS iTraxx Europe Crossover Index Receiver OptionTr005— Asset class (EQ_SN), Long Call Option on AAPLTr006— Asset class(EQ_IX), Long Put Option on S&P500 IndexTr007_SOpt— Asset class (CO), Long Put Option on CORN (sold option with premium paid)Tr008— Asset class (EQ_IX), Long Variance Swap on EURO STOXX 50 (EQUITY_VOL trade)Tr009— Asset class (IR), 10 Year FedFunds / 3M SOFR Basis Swap (USD_BASIS trade)Tr010— Asset class (CO), Short WTI Crude Futures Put OptionTr011— Asset class (CO), Long Gold Futures Call OptionTr012— Asset class (CO), Long Bitcoin Futures Call Option

The data contains the following collateral positions:

ColPos01— (CASH, Domestic Currency)ColPos02— (CASH, Foreign Currency)ColPos03— (BOND, Sovereign AAA)ColPos04— (EQUITY, Main Index)ColPos05— (GOLD)

The data contains the following portfolios:

Port_001: Portfolio containing the following:

- Trades: Tr001

- Netting Sets: None

- Collateral Sets: None

- Collateral Positions: None

Port_002: Portfolio containing the following:

- Trades: Tr002

- Netting Sets: None

- Collateral Sets: None

- Collateral Positions: None

Port_003: Portfolio containing the following:

- Trades: Tr003, Tr004

- Netting Sets: None

- Collateral Sets: None

- Collateral Positions: None

Port_004: Portfolio containing the following:

- Trades: Tr001, Tr002, Tr003, Tr004, Tr005, Tr006, Tr007

- Netting Sets: None

- Collateral Sets: None

- Collateral Positions: None

Port_005: Portfolio containing the following:

- Trades: Tr001, Tr002, Tr003, Tr004, Tr005, Tr006, Tr007

- Netting Sets: N001

- Collateral Sets: None

- Collateral Positions: None

Port_006: Portfolio containing the following:

- Trades: Tr001, Tr002, Tr003, Tr004, Tr005, Tr006, Tr007

- Netting Sets: N001

- Collateral Sets: CSA01

- Collateral Positions: None

Port_007: Portfolio containing the following:

- Trades: Tr001, Tr002, Tr003, Tr004, Tr005, Tr006, Tr007

- Netting Sets: N001

- Collateral Sets: CSA01

- Collateral Positions: ColPos01, ColPos02, ColPos03

Port_008: Portfolio containing the following:

- Trades: Tr008, Tr009

- Netting Sets: N002

- Collateral Sets: CSA02

- Collateral Positions: ColPos04, ColPos05

Port_009: Portfolio containing the following:

- Trades: Tr010, Tr011, Tr012

- Netting Sets: N003

- Collateral Sets: CA03

- Collateral Positions: None

- Counterparty ID: Exchange

SA-CCR Examples

The example data is used in the following examples:

Create saccr Object and Compute Regulatory Values for Interest-Rate Swap

Create saccr Object and Compute Regulatory Values for Forward FX Swap

Create saccr Object and Compute Regulatory Values for Two CDS Trades

Create saccr Object and Compute Regulatory Values for Multiple Asset Classes

Create saccr Object and Compute Regulatory Values for Multiple Asset Classes with Netting Set