creditMigrationCopula Simulation Workflow

This example shows a common workflow for using a creditMigrationCopula object for a portfolio of counterparty credit ratings.

Step 1. Create a creditMigrationCopula object with a 4-factor model.

Load the saved portfolio data.

load CreditMigrationData.mat;Scale the bond prices for portfolio positions for each bond.

migrationValues = migrationPrices .* numBonds;

Create a creditMigrationCopula object with a 4-factor model using creditMigrationCopula.

cmc = creditMigrationCopula(migrationValues,ratings,transMat,... lgd,weights,'FactorCorrelation',factorCorr)

cmc =

creditMigrationCopula with properties:

Portfolio: [250×5 table]

FactorCorrelation: [4×4 double]

RatingLabels: [8×1 string]

TransitionMatrix: [8×8 double]

VaRLevel: 0.9500

UseParallel: "off"

PortfolioValues: []

Step 2. Set the VaRLevel to 99%.

Set the VarLevel property for the creditMigrationCopula object to 99% (the default is 95%).

cmc.VaRLevel = 0.99;

Step 3. Display the Portfolio property for information about migration values, ratings, LGDs, and weights.

Display the Portfolio property containing information about migration values, ratings, LGDs, and weights. The columns in the migration values are in the same order of the ratings, with the default rating in the last column.

head(cmc.Portfolio)

ID MigrationValues Rating LGD Weights

__ ____________________________________________________________________________ ______ ______ ___________________________________

1 13301 13280 13216 13082 12421 11939 10180 11700 "A" 0.6509 0 0 0 0.5 0.5

2 2944 2939 2923.8 2892.6 2737.1 2624 2218.2 3000 "BBB" 0.8283 0 0.55 0 0 0.45

3 9797.5 9787.9 9754.2 9681.2 9320.5 9050 7976.8 9100 "AA" 0.6041 0 0.7 0 0 0.3

4 4760.4 4754.3 4735.7 4696.9 4502.7 4359.7 3824.8 4400 "BB" 0.6509 0 0.55 0 0 0.45

5 10524 10509 10466 10376 9923.5 9591.5 8362.1 10100 "BBB" 0.4966 0 0 0.75 0 0.25

6 6192.8 6183.2 6154.2 6094.3 5795.1 5576.4 4782.7 6200 "BB" 0.8283 0 0 0 0.65 0.35

7 5736.9 5727.5 5699.3 5640.7 5349.5 5137.6 4367.4 5200 "BB" 0.6041 0 0 0 0.65 0.35

8 5065.3 5062.7 5056.4 5038.8 4956.2 4892.2 4491.9 4800 "BB" 0.4873 0.5 0 0 0 0.5

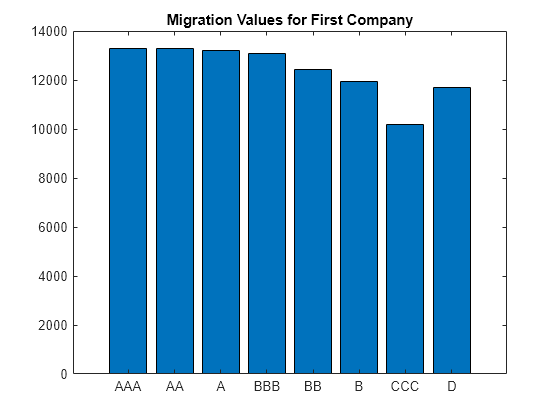

Step 4. Display migration values for a counterparty.

For example, you can display the migration values for the first counterparty. Note that the value for default is higher than some of the non-default ratings. This is because the migration value for the default rating is a reference value (for example, face value, forward value at current rating, or other) that is multiplied by the recovery rate during the simulation to get the value of the asset in the event of default. The recovery rate is 1-LGD when the LGD input to creditMigrationCopula is a constant LGD value (the LGD input has one column). The recovery rate is a random quantity when the LGD input to creditMigrationCopula is specified as a mean and standard deviation for a beta distribution (the LGD input has two columns).

bar(cmc.Portfolio.MigrationValues(1,:))

xticklabels(cmc.RatingLabels)

title("Migration Values for First Company")

Step 5. Run a simulation.

Use the simulate function to simulate 100,000 scenarios.

cmc = simulate(cmc,1e5)

cmc =

creditMigrationCopula with properties:

Portfolio: [250×5 table]

FactorCorrelation: [4×4 double]

RatingLabels: [8×1 string]

TransitionMatrix: [8×8 double]

VaRLevel: 0.9900

UseParallel: "off"

PortfolioValues: [2.0082e+06 1.9950e+06 1.9933e+06 2.0009e+06 1.9819e+06 1.9955e+06 1.9962e+06 1.9966e+06 2.0018e+06 2.0036e+06 1.9873e+06 1.9929e+06 2.0015e+06 1.9875e+06 1.9962e+06 2.0070e+06 2.0054e+06 2.0037e+06 2.0032e+06 … ] (1×100000 double)

Step 6. Generate a report for the portfolio risk.

Use the portfolioRisk function to obtain a report for risk measures and confidence intervals for EL, Std, VaR, and CVaR.

[portRisk,RiskConfidenceInterval] = portfolioRisk(cmc)

portRisk=1×4 table

EL Std VaR CVaR

______ _____ _____ _____

4515.9 12963 57176 83975

RiskConfidenceInterval=1×4 table

EL Std VaR CVaR

________________ ______________ ______________ ______________

4435.6 4596.3 12907 13021 55739 58541 82137 85812

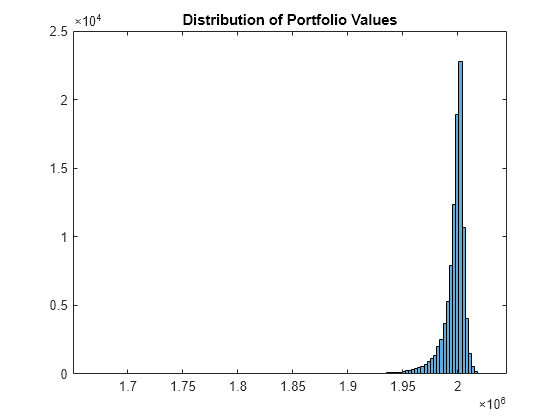

Step 7. Visualize the distribution.

View a histogram of the portfolio values.

figure

h = histogram(cmc.PortfolioValues,125);

title("Distribution of Portfolio Values");

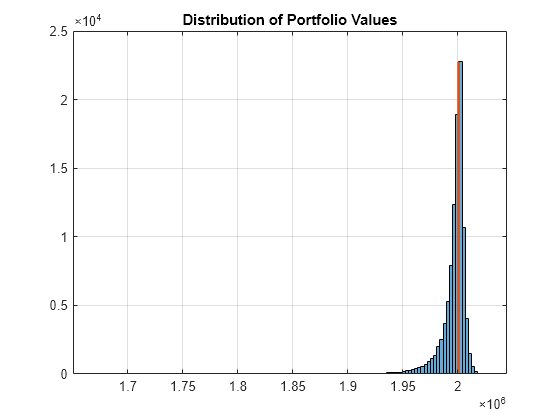

Step 8. Overlay the value if all counterparties maintain current credit ratings.

Overlay the value that the portfolio object (cmc) takes if all counterparties maintain their current credit ratings.

CurrentRatingValue = portRisk.EL + mean(cmc.PortfolioValues); hold on plot([CurrentRatingValue CurrentRatingValue],[0 max(h.Values)],'LineWidth',2); grid on

Step 9. Generate a risk contributions report.

Use the riskContribution function to display the risk contribution. The risk contributions, EL and CVaR, are additive. If you sum each of these two metrics over all the counterparties, you get the values reported for the entire portfolio in the portfolioRisk table.

rc = riskContribution(cmc); disp(rc(1:10,:))

ID EL Std VaR CVaR

__ ______ ______ ______ ______

1 15.521 41.153 238.72 279.18

2 8.49 18.838 92.074 122.19

3 6.0937 20.069 113.22 181.53

4 6.6964 55.885 272.23 313.25

5 23.583 73.905 360.32 573.39

6 10.722 114.97 445.94 728.38

7 1.8393 84.754 262.32 490.39

8 11.711 39.768 175.84 253.29

9 2.2154 4.4038 22.797 31.039

10 1.7453 2.5545 9.8801 17.603

Step 10. Simulate the risk exposure with a t copula.

To use a t copula with 10 degrees of freedom, use the simulate function with optional input arguments. Save the results to a new creditMigrationCopula object (cmct).

cmct = simulate(cmc,1e5,'Copula','t','DegreesOfFreedom',10)

cmct =

creditMigrationCopula with properties:

Portfolio: [250×5 table]

FactorCorrelation: [4×4 double]

RatingLabels: [8×1 string]

TransitionMatrix: [8×8 double]

VaRLevel: 0.9900

UseParallel: "off"

PortfolioValues: [2.0021e+06 2.0007e+06 1.9834e+06 2.0025e+06 2.0002e+06 2.0021e+06 2.0039e+06 2.0023e+06 2.0017e+06 2.0101e+06 2.0002e+06 2.0080e+06 2.0007e+06 2.0052e+06 1.9969e+06 2.0071e+06 2.0045e+06 1.9979e+06 2.0021e+06 … ] (1×100000 double)

Step 11. Generate a report for the portfolio risk for the t copula.

Use the portfolioRisk function to obtain a report for risk measures and confidence intervals for EL, Std, VaR, and CVaR.

[portRisk2,RiskConfidenceInterval2] = portfolioRisk(cmct)

portRisk2=1×4 table

EL Std VaR CVaR

____ _____ _____ __________

4544 17034 72270 1.2391e+05

RiskConfidenceInterval2=1×4 table

EL Std VaR CVaR

________________ ______________ ______________ ________________________

4438.5 4649.6 16960 17109 69769 75382 1.1991e+05 1.2791e+05

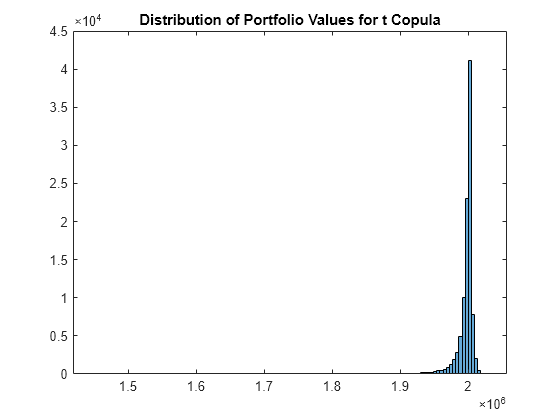

Step 12. Visualize the distribution for the t copula.

View a histogram of the portfolio values.

figure

h = histogram(cmct.PortfolioValues,125);

title("Distribution of Portfolio Values for t Copula");

Step 13. Overlay the value if all counterparties maintain current credit ratings for t copula.

Overlay the value that the portfolio object (cmct) takes if all counterparties maintain their current credit ratings.

CurrentRatingValue2 = portRisk2.EL + mean(cmct.PortfolioValues); hold on plot([CurrentRatingValue2 CurrentRatingValue2],[0 max(h.Values)],'LineWidth',2); grid on

See Also

creditMigrationCopula | simulate | portfolioRisk | riskContribution | confidenceBands | getScenarios | asrf