PanelModel

Description

PanelModel is an object that encapsulates a fitted panel

(longitudinal) data regression model. A panel data regression model describes the linear

relationship between a response variable and predictor variables, in which the data set is a

random, observational sample of n subjects measured over

T time points. The model accommodates a linear random effect

(heterogeneity), which you can use to control for, and study,

unobserved, subject-specific, phenomena associated with the response variable.

Use the properties of a PanelData object to investigate the fitted panel

data regression model. The object properties include information about coefficient and effect

estimates, associated variances and covariances, and inferences.

Creation

Create a PanelModel object by using the fitrepanel function.

fitrepanel fits a random effects panel data

regression model to data. That is, the observed and unobserved effects are independent (not to

be confused with the random effects of a linear mixed-effects model, as computed by the

fitlme function).

Properties

Examples

Fit a random effects panel data regression model to data using default options. The data is in wide format.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

The variable Data is a 3-D numeric array containing the predictor and response variables. Each row is a time point in the sampling period, each column is a subject in the sample, and each page is a variable. The final variable in Data is the response variable (log wages series), while all other variables are predictors.

Create separate variables for the predictor and response data.

X = Data(:,:,1:(end-1)); Y = Data(:,:,end);

X is a 15-by-1000-by-11 numeric array of predictor data and Y is a 15-by-1000 numeric matrix. For example, X(10,501,3) is the education experience of subject 501 in 2015.

Create a binary numeric variable for whether the subject is female (coded as 1), by using predictor 2, and a binary numeric variable for whether the subject is married (coded as 1), by using predictor 9.

X(:,:,2) = double(X(:,:,2) == 1); X(:,:,9) = double(X(:,:,9) == 1);

Assume that the subject effect (heterogeneity) is not associated with the predictor variables. Fit a random effects panel data regression model to the data. Use default options.

EstMdl = fitrepanel(X,Y);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

-----------------------------------------------------------

x1 | 0.0485 0.0003 154.4327 0

x2 | -0.3381 0.0324 -10.4265 0.0000

x3 | 0.1003 0.0036 28.0246 0.0000

x4 | -0.1370 0.0389 -3.5231 0.0004

x5 | -0.0620 0.0047 -13.1530 0.0000

x6 | 0.0087 0.0053 1.6637 0.0962

x7 | -0.0390 0.0112 -3.4902 0.0005

x8 | -0.0191 0.0071 -2.6853 0.0072

x9 | -0.0516 0.0107 -4.8406 0.0000

x10 | 0.0741 0.0051 14.6575 0.0000

x11 | 0.0016 0.0003 5.7319 0.0000

DisturbanceVariance | 0.0302

EffectVariance | 0.0947

fitrepanel displays an estimation summary to the command line. Row xj contains, for predictor j, the coefficient estimate, standard error, and statistic for a two-tailed test that the coefficient is 0 with its -value. All predictor variables are significant except for x6 and x7.

Display the fitted model.

EstMdl

EstMdl =

PanelModel with properties:

Coefficients: [11×1 double]

CoefficientCovariance: [11×11 double]

DisturbanceVariance: 0.0302

EffectVariance: 0.0947

Effects: [4.5484 4.3304 4.6605 4.9304 4.9176 4.5704 3.8183 4.7566 4.4485 4.1725 4.6417 4.5086 4.7519 4.4794 4.2617 4.7618 4.5002 4.3778 4.1206 3.8693 3.9290 4.5513 4.5366 4.2080 4.6091 4.2711 4.6690 3.7448 3.9863 … ] (1×1000 double)

LogLikelihood: 4.9624e+03

Summary: [13×4 table]

Type: "RandomEffects"

EstMdl is a PanelModel object. You can access its properties using dot notation.

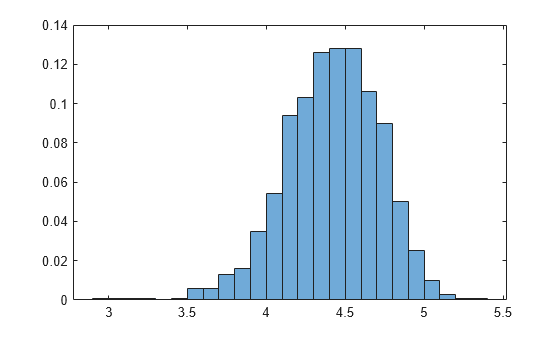

Plot the empirical distribution of the heterogeneity.

effects = EstMdl.Effects;

histogram(effects,Normalization="probability")

Fit a random effects panel data regression model to data and obtain robust estimates.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

Create separate variables for the predictor and response data.

X = Data(:,:,1:(end-1)); [T,n,p] = size(X); Y = Data(:,:,end);

Create a binary numeric variable for whether the subject is female (coded as 1), by using predictor 2, and a binary numeric variable for whether the subject is married (coded as 1), by using predictor 9.

X(:,:,2) = double(X(:,:,2) == 1); X(:,:,9) = double(X(:,:,9) == 1);

Simulate heteroscedasticity in the system by using unmeasured, subject-specific predictor variables such that, for each subject , and . For each subject, simulate values.

rng(1,"twister") Z = zeros(T,n); for j = 1:n lambda = randi(50); Z(:,j) = poissrnd(lambda,T,1); end

Add the simulated predictor data to the response data with coefficient .

YSim = Y + 2*Z;

Assume that the heterogeneity is not associated with the predictor variables. Fit a random effects panel data regression model to the predictor data without and the simulated response data. Use default options.

EstMdl = fitrepanel(X,YSim);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

----------------------------------------------------------

x1 | 0.0196 0.0190 1.0279 0.3040

x2 | 1.4279 3.0659 0.4657 0.6414

x3 | -0.1095 0.3385 -0.3236 0.7462

x4 | -2.0201 3.6775 -0.5493 0.5828

x5 | 0.3700 0.2763 1.3392 0.1805

x6 | -0.2306 0.3087 -0.7472 0.4550

x7 | 0.9527 0.6997 1.3616 0.1733

x8 | 0.1847 0.4256 0.4341 0.6642

x9 | 0.3463 0.6632 0.5223 0.6015

x10 | -0.0337 0.2965 -0.1137 0.9094

x11 | 0.0070 0.0161 0.4345 0.6640

DisturbanceVariance | 101.9401

EffectVariance | 859.3624

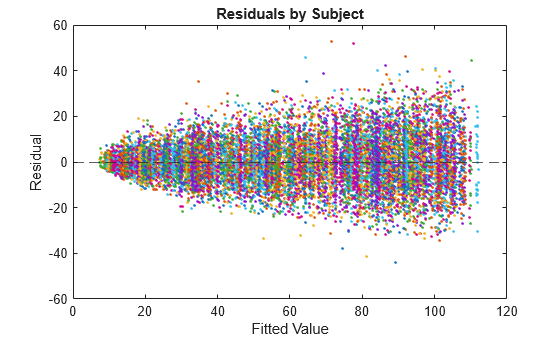

Compute model residuals , and plot them against the fitted responses. Color the residuals according to subject ID.

betahat = reshape(EstMdl.Coefficients,1,1,p); alphahat = EstMdl.Effects; Yhat = sum(X.*betahat,3) + alphahat; Residuals = YSim - Yhat; figure plot(Yhat,Residuals,'.') hold on yline(0,"--") hold off title("Residuals by Subject") ylabel("Residual") xlabel("Fitted Value")

The residuals scatter more widely as the fitted values increase. This behavior is indicative of heteroscedasticity. Also, residuals appear clustered by groups.

Refit the model; compute robust covariance estimates.

EstMdlRobust = fitrepanel(X,YSim,RobustCovariance=true);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

----------------------------------------------------------

x1 | 0.0196 0.0191 1.0222 0.3067

x2 | 1.4279 2.8975 0.4928 0.6222

x3 | -0.1095 0.3417 -0.3205 0.7486

x4 | -2.0201 3.5807 -0.5642 0.5726

x5 | 0.3700 0.2755 1.3431 0.1792

x6 | -0.2306 0.3215 -0.7174 0.4731

x7 | 0.9527 0.6701 1.4218 0.1551

x8 | 0.1847 0.4344 0.4253 0.6706

x9 | 0.3463 0.6501 0.5327 0.5942

x10 | -0.0337 0.2976 -0.1133 0.9098

x11 | 0.0070 0.0159 0.4414 0.6589

DisturbanceVariance | 101.9401

EffectVariance | 859.3624

The coefficient estimates between the regular and robust runs are the same; the difference between the runs is in the inferences.

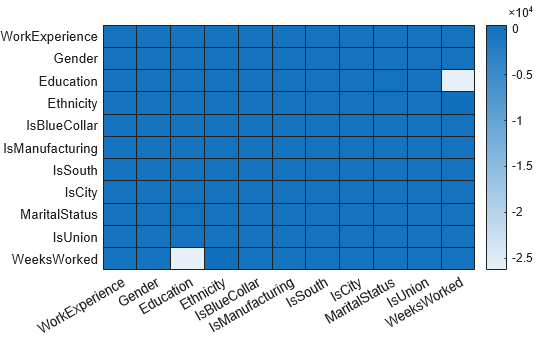

Plot a heatmap of the difference between the estimated coefficient covariance matrix.

seriesSim = series(1:p); heatmap(seriesSim,seriesSim,(EstMdlRobust.CoefficientCovariance-EstMdl.CoefficientCovariance)./EstMdl.CoefficientCovariance)

The estimated covariance of the coefficients of Education and WeeksWorked shows the greatest relative difference between the robust and non-robust analyses.

Alternative Functionality

When your longitudinal data set is the result of a controlled experiment study, fit a

linear mixed-effects model (LinearMixedModel object) by using fitlme.

References

Version History

Introduced in R2026a

See Also

fitrepanel | fitlme | fitrm | fitlmematrix