fitrepanel

Syntax

Description

EstMdl = fitrepanel(X,Y)EstMdl, from fitting the model to the input panel data in wide

format. X is a

T-by-n-by-p array of predictor

data and Y is a T-by-n matrix of

response data, where T is the greatest number of sampling time points

among subjects, n is the number of sampled subjects, and

p is the number of predictor variables. A data set in wide format must

be organized as follows:

Rows correspond to time points in the sample. In other words, row t contains all p measurements for all n subjects at time t.

Columns correspond to sampled subjects. In other words, column c contains all p measurements over all T time points of subject c.

For

X, pages correspond to predictor variables. In other words, page k contains measurements of predictor k for all n subjects and T time points in the sample. None of the predictors can represent an intercept. Among subjects, sampled time points correspond (fitrepanelassumes all subjects are measured simultaneously).

EstMdl is a panel data regression model PanelModel.

EstMdl = fitrepanel(X,Y,groups)X is an

m-by-p matrix of predictor data and

Y is an m-by-1 vector of response data, where

m is the number of observations (for example, m =

Tn for a balanced panel data set). Each row is an observation (all

measurements) associated with a particular subject at a particular time, and each column is

a variable. The groups input specifies to which subject the observation

belongs. For a subject, larger row indices indicate measurements taken later in the

sample.

EstMdl = fitrepanel(Tbl,PredictorVariables=predictorVariables,GroupVariable=groupVariable)Tbl. Panel data in a table is in

long format. The Tbl input argument has

m rows; each row is an observation. The

predictorVariables input specifies which table variables are

predictor variables. groupVariable specifies to which subject the

measurements in the rows of the data belong. The last table variable is the response

variable.

EstMdl = fitrepanel(___,Name=Value)fitrepanel(Tbl,PredictorVariables=predictors,GroupVariable="Country",ResponseVariable="LogGDP",FitEffects=false,Method="ssm")

specifies that the table variable LogGDP contains the response data,

the table variable Country contains the subject identifiers, and the

arbitrary string vector predictors contains the predictor variable names

in the table. This syntax skips fitting the unobserved effects and estimates the parameters

by using maximum likelihood in the state-space model framework.

Examples

Fit a random effects panel data regression model to data using default options. The data is in wide format.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

The variable Data is a 3-D numeric array containing the predictor and response variables. Each row is a time point in the sampling period, each column is a subject in the sample, and each page is a variable. The final variable in Data is the response variable (log wages series), while all other variables are predictors.

Create separate variables for the predictor and response data.

X = Data(:,:,1:(end-1)); Y = Data(:,:,end);

X is a 15-by-1000-by-11 numeric array of predictor data and Y is a 15-by-1000 numeric matrix. For example, X(10,501,3) is the education experience of subject 501 in 2015.

Create a binary numeric variable for whether the subject is female (coded as 1), by using predictor 2, and a binary numeric variable for whether the subject is married (coded as 1), by using predictor 9.

X(:,:,2) = double(X(:,:,2) == 1); X(:,:,9) = double(X(:,:,9) == 1);

Assume that the subject effect (heterogeneity) is not associated with the predictor variables. Fit a random effects panel data regression model to the data. Use default options.

EstMdl = fitrepanel(X,Y);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

-----------------------------------------------------------

x1 | 0.0485 0.0003 154.4327 0

x2 | -0.3381 0.0324 -10.4265 0.0000

x3 | 0.1003 0.0036 28.0246 0.0000

x4 | -0.1370 0.0389 -3.5231 0.0004

x5 | -0.0620 0.0047 -13.1530 0.0000

x6 | 0.0087 0.0053 1.6637 0.0962

x7 | -0.0390 0.0112 -3.4902 0.0005

x8 | -0.0191 0.0071 -2.6853 0.0072

x9 | -0.0516 0.0107 -4.8406 0.0000

x10 | 0.0741 0.0051 14.6575 0.0000

x11 | 0.0016 0.0003 5.7319 0.0000

DisturbanceVariance | 0.0302

EffectVariance | 0.0947

fitrepanel displays an estimation summary to the command line. Row xj contains, for predictor j, the coefficient estimate, standard error, and statistic for a two-tailed test that the coefficient is 0 with its -value. All predictor variables are significant except for x6 and x7.

Display the fitted model.

EstMdl

EstMdl =

PanelModel with properties:

Coefficients: [11×1 double]

CoefficientCovariance: [11×11 double]

DisturbanceVariance: 0.0302

EffectVariance: 0.0947

Effects: [4.5484 4.3304 4.6605 4.9304 4.9176 4.5704 3.8183 4.7566 4.4485 4.1725 4.6417 4.5086 4.7519 4.4794 4.2617 4.7618 4.5002 4.3778 4.1206 3.8693 3.9290 4.5513 4.5366 4.2080 4.6091 4.2711 4.6690 3.7448 3.9863 … ] (1×1000 double)

LogLikelihood: 4.9624e+03

Summary: [13×4 table]

Type: "RandomEffects"

EstMdl is a PanelModel object. You can access its properties using dot notation.

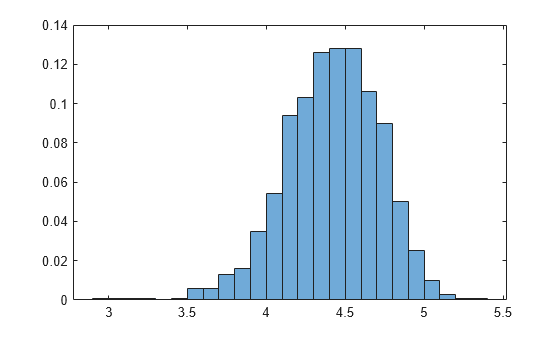

Plot the empirical distribution of the heterogeneity.

effects = EstMdl.Effects;

histogram(effects,Normalization="probability")

Fit a random effects panel data regression model to data using default options. The data is in long format.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

Load and Extract Data

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

The variable Data is a 3-D numeric array containing the predictor and response variables. Each row is a time point in the sampling period, each column in a subject is the sample, and each page is a variable. The final variable in Data is the response variable (log wages series), while all other variables are predictors. This data format is wide.

Create separate variables for the predictor and response data.

X = Data(:,:,1:(end-1)); Y = Data(:,:,end); [T,n,p] = size(X)

T = 15

n = 1000

p = 11

X is a 15-by-1000-by-11 numeric array of predictor data and Y is a 15-by-1000 numeric matrix. For example, X(10,501,3) is the education experience of subject 501 in 2015.

Convert Data to Long Format

Data in long format must have the following characteristics:

The response data is a -by-1 vector, where is the number of periods in time time base and is the number of subjects. In this example, the long-format response data is a 15000-by-1 vector.

The predictor data is a -by- matrix, where is the number of predictors. In this example, the long-format predictor data is a 15000-by-11 matrix.

The software must be able to identify to which subject the observation belongs by a -by-1 vector of subject IDs.

For each subject, the software assumes that observations in higher rows were sampled later.

Convert the response data to long format by stacking the columns of Y using linear indexing with a single colon.

YLong = Y(:); size(YLong)

ans = 1×2

15000 1

For selected subjects, verify that the responses are arranged by blocks of subjects, increasing by sampling time within each block. To choose a subject to check, use the control.

j =3; % Subject index YSubj = Y(1:T,j); YLongSubj = YLong((T*(j-1)+1):(T*j)); sum(YSubj - YLongSubj)

ans = 0

Convert the predictor data to long format by stacking the columns of X and setting its pages to columns using reshape.

XLong = reshape(X,T*n,11); size(XLong)

ans = 1×2

15000 11

XLong is arranged such that all subject-specified measurements are blocked together and stacked, and within-subject blocks of observations are arranged in increasing order by sampling time.

For selected subjects, verify that the predictor data are arranged by blocks of subjects, increasing by sampling time within each block. To choose a subject to check, use the control.

j =  6;

XSubj = squeeze(X(1:T,j,:));

XLongSubj = XLong((T*(j-1)+1):(T*j),:);

sum(sum(XSubj - XLongSubj))

6;

XSubj = squeeze(X(1:T,j,:));

XLongSubj = XLong((T*(j-1)+1):(T*j),:);

sum(sum(XSubj - XLongSubj))ans = 0

Observations are arranged by blocks of subjects. Create a numeric vector, which identifies each subject, by repeating each integer in the interval times, and then stacking the results.

Groups = repmat(1:n,T,1); Groups = Groups(:);

Preprocess Data

Create a binary numeric variable for whether the subject is female (coded as 1), by using predictor 2, and a binary numeric variable for whether the subject is married (coded as 1), by using predictor 9.

XLong(:,2) = double(XLong(:,2) == 1); XLong(:,9) = double(XLong(:,9) == 1);

Fit the Model to Data

Fit a random effects panel data regression model of the log wage series (LogWage) to all other variables in the timetable except the subject ID (Group). Specify the predictor and grouping variables; fitrepanel assumes the final variable is the response variable.

Assume that the heterogeneity is not associated with the predictor variables. Fit a random effects panel data regression model to the long-format data. Specify the grouping variable. Use default options.

EstMdl = fitrepanel(XLong,YLong,Groups);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

-----------------------------------------------------------

x1 | 0.0485 0.0003 154.4327 0

x2 | -0.3381 0.0324 -10.4265 0.0000

x3 | 0.1003 0.0036 28.0246 0.0000

x4 | -0.1370 0.0389 -3.5231 0.0004

x5 | -0.0620 0.0047 -13.1530 0.0000

x6 | 0.0087 0.0053 1.6637 0.0962

x7 | -0.0390 0.0112 -3.4902 0.0005

x8 | -0.0191 0.0071 -2.6853 0.0072

x9 | -0.0516 0.0107 -4.8406 0.0000

x10 | 0.0741 0.0051 14.6575 0.0000

x11 | 0.0016 0.0003 5.7319 0.0000

DisturbanceVariance | 0.0302

EffectVariance | 0.0947

The results are the same as the results from the model fit to data in wide format.

Fit a random effects panel data regression model to data using default options. The data is in a timetable.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

The variable DataTimeTable is a timetable containing the data. LogWage is the response variable, Group is the subject ID (grouping) variable, and all other variables are predictors. Each row is an observation for a subject at a time point in the sampling period (in other words, this data format is wide).

Display the head and size of the timetable of data.

head(DataTimeTable)

Time WorkExperience Gender Education Ethnicity IsBlueCollar IsManufacturing IsSouth IsCity MaritalStatus IsUnion WeeksWorked Group LogWage

____ ______________ ______ _________ _________ ____________ _______________ _______ ______ _____________ _______ ___________ _____ _______

2006 29 female 12 0 1 0 0 0 nevermarried 0 48 1 6.7956

2007 30 female 12 0 1 0 0 0 nevermarried 0 49 1 6.6592

2008 31 female 12 0 1 0 0 0 nevermarried 0 51 1 6.9801

2009 32 female 12 0 0 0 0 0 nevermarried 0 45 1 7.2397

2010 33 female 12 0 0 0 0 0 nevermarried 0 25 1 7.123

2011 34 female 12 0 0 0 0 0 nevermarried 0 42 1 6.9183

2012 35 female 12 0 0 0 0 0 nevermarried 0 48 1 7.1639

2013 36 female 12 0 0 0 0 0 nevermarried 0 49 1 7.0534

size(DataTimeTable)

ans = 1×2

15000 13

Create a new timetable TT containing a binary numeric variable for whether the subject is female, by using Gender, and a binary numeric variable for whether the subject is married, by using MaritalStatus. Then, remove the corresponding variables from TT.

TT = DataTimeTable; TT.IsFemale = double(TT.Gender == "female"); TT = movevars(TT,"IsFemale","Before","Gender"); TT.Gender = []; TT.IsMarried = double(TT.MaritalStatus == "married"); TT = movevars(TT,"IsMarried","Before","MaritalStatus"); TT.MaritalStatus = [];

Fit a random effects panel data regression model of the log wage series (LogWage) to all other variables in the timetable except the subject ID (Group). Specify the predictor and grouping variable names; fitrepanel assumes the final variable is the response variable.

prednames = TT.Properties.VariableNames(1:end-2);

EstMdl = fitrepanel(TT,PredictorVariables=prednames,GroupVariable="Group");Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

-----------------------------------------------------------

WorkExperience | 0.0485 0.0003 154.4327 0

IsFemale | -0.3381 0.0324 -10.4265 0.0000

Education | 0.1003 0.0036 28.0246 0.0000

Ethnicity | -0.1370 0.0389 -3.5231 0.0004

IsBlueCollar | -0.0620 0.0047 -13.1530 0.0000

IsManufacturing | 0.0087 0.0053 1.6637 0.0962

IsSouth | -0.0390 0.0112 -3.4902 0.0005

IsCity | -0.0191 0.0071 -2.6853 0.0072

IsMarried | -0.0516 0.0107 -4.8406 0.0000

IsUnion | 0.0741 0.0051 14.6575 0.0000

WeeksWorked | 0.0016 0.0003 5.7319 0.0000

DisturbanceVariance | 0.0302

EffectVariance | 0.0947

The results are the same as the results from the model fit to data in wide format.

Estimate a random effects panel data regression model of log wages as a function of a set of predictors by viewing the model as a linear state-space model.

By default, fitrepanel uses GLS to estimate the model. Alternatively, you can specify that fitrepanel view the model as a linear state-space, and apply maximum likelihood to estimate the parameters.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

Create a new timetable TT containing a binary numeric variable for whether the subject is female, by using Gender, and a binary numeric variable for whether the subject is married, by using MaritalStatus. Then, remove the corresponding variables from TT.

TT = DataTimeTable; TT.IsFemale = double(TT.Gender == "female"); TT = movevars(TT,"IsFemale","Before","Gender"); TT.Gender = []; TT.IsMarried = double(TT.MaritalStatus == "married"); TT = movevars(TT,"IsMarried","Before","MaritalStatus"); TT.MaritalStatus = [];

Fit a random effects panel data regression model of the log wage series (LogWage) to all other variables in the processed timetable TT except the subject ID. Specify the state-space model estimation method.

varnames = TT.Properties.VariableNames; prednames = varnames(~ismember(varnames,["Group" "LogWage"])); EstMdl = fitrepanel(TT,PredictorVariables=prednames,GroupVariable="Group",Method="ssm");

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (SSM)

| Estimator SE tStat pValue

-----------------------------------------------------------

WorkExperience | 0.0485 0.0003 154.4004 0

IsFemale | -0.3381 0.0325 -10.3976 0.0000

Education | 0.1003 0.0036 27.9469 0.0000

Ethnicity | -0.1370 0.0390 -3.5132 0.0004

IsBlueCollar | -0.0620 0.0047 -13.1543 0.0000

IsManufacturing | 0.0088 0.0053 1.6647 0.0960

IsSouth | -0.0389 0.0112 -3.4838 0.0005

IsCity | -0.0191 0.0071 -2.6810 0.0073

IsMarried | -0.0516 0.0107 -4.8464 0.0000

IsUnion | 0.0741 0.0051 14.6588 0.0000

WeeksWorked | 0.0016 0.0003 5.7332 0.0000

DisturbanceVariance | 0.0302 0.0004 84.7569 0

EffectVariance | 0.0953 0.0040 23.7771 0.0000

The results are nearly the same as the results from the model fit using GLS. This similarity occurs because, in this problem, maximum likelihood and GLS are asymptotically equal.

Fit a random effects panel data regression model to data; fix the random effects variance to a known value.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

Create a new timetable TT containing a binary numeric variable for whether the subject is female, by using Gender, and a binary numeric variable for whether the subject is married, by using MaritalStatus. Then, remove the corresponding variables from TT.

TT = DataTimeTable; TT.IsFemale = double(TT.Gender == "female"); TT = movevars(TT,"IsFemale","Before","Gender"); TT.Gender = []; TT.IsMarried = double(TT.MaritalStatus == "married"); TT = movevars(TT,"IsMarried","Before","MaritalStatus"); TT.MaritalStatus = [];

Fit a random effects panel data regression model of the log wage series (LogWage) to all other variables in the timetable except the subject ID (Group). Specify the predictor and grouping variable names. Fix the random effects variance to 0.05, 0.1, and then 0.2. Suppress the estimation display.

prednames = TT.Properties.VariableNames(1:end-2); sigma2alpha = [0.05 0.1 0.5 1]; m = numel(sigma2alpha); Coefficients = cell(3,1); DisturbanceVariance = zeros(3,1); for j = 1:m EstMdl = fitrepanel(TT,PredictorVariables=prednames,GroupVariable="Group", ... EffectVariance=sigma2alpha(j),Display=false); Coefficients{j} = EstMdl.Coefficients; DisturbanceVariance(j) = EstMdl.DisturbanceVariance; end cell2mat(Coefficients')

ans = 11×4

0.0486 0.0485 0.0484 0.0483

-0.3376 -0.3381 -0.3387 -0.3388

0.1003 0.1004 0.1004 0.1004

-0.1378 -0.1370 -0.1359 -0.1357

-0.0621 -0.0620 -0.0618 -0.0618

0.0082 0.0088 0.0094 0.0096

-0.0451 -0.0385 -0.0294 -0.0278

-0.0231 -0.0189 -0.0148 -0.0143

-0.0413 -0.0523 -0.0653 -0.0673

0.0744 0.0741 0.0740 0.0740

0.0016 0.0016 0.0016 0.0016

DisturbanceVariance

DisturbanceVariance = 4×1

0.0302

0.0302

0.0302

0.0302

The estimates are nearly the same among the effects variance settings, which shows that the estimators are robust to moderate to extreme levels of the effects variance.

Fit a random effects panel data regression model to data and obtain robust estimates.

Load the simulated, balanced panel data set Data_SimulatedBalancedPanel.mat, which is available when you open this example. The data set contains 12 microeconomic measurements of 1000 randomly selected people taken yearly from 2006 through 2020. The response variable in the model is a series of log wages, while all other variables in the data are predictors.

load Data_SimulatedBalancedPanelFor details on the data set, enter Description at the command line.

Create separate variables for the predictor and response data.

X = Data(:,:,1:(end-1)); [T,n,p] = size(X); Y = Data(:,:,end);

Create a binary numeric variable for whether the subject is female (coded as 1), by using predictor 2, and a binary numeric variable for whether the subject is married (coded as 1), by using predictor 9.

X(:,:,2) = double(X(:,:,2) == 1); X(:,:,9) = double(X(:,:,9) == 1);

Simulate heteroscedasticity in the system by using unmeasured, subject-specific predictor variables such that, for each subject , and . For each subject, simulate values.

rng(1,"twister") Z = zeros(T,n); for j = 1:n lambda = randi(50); Z(:,j) = poissrnd(lambda,T,1); end

Add the simulated predictor data to the response data with coefficient .

YSim = Y + 2*Z;

Assume that the heterogeneity is not associated with the predictor variables. Fit a random effects panel data regression model to the predictor data without and the simulated response data. Use default options.

EstMdl = fitrepanel(X,YSim);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

----------------------------------------------------------

x1 | 0.0196 0.0190 1.0279 0.3040

x2 | 1.4279 3.0659 0.4657 0.6414

x3 | -0.1095 0.3385 -0.3236 0.7462

x4 | -2.0201 3.6775 -0.5493 0.5828

x5 | 0.3700 0.2763 1.3392 0.1805

x6 | -0.2306 0.3087 -0.7472 0.4550

x7 | 0.9527 0.6997 1.3616 0.1733

x8 | 0.1847 0.4256 0.4341 0.6642

x9 | 0.3463 0.6632 0.5223 0.6015

x10 | -0.0337 0.2965 -0.1137 0.9094

x11 | 0.0070 0.0161 0.4345 0.6640

DisturbanceVariance | 101.9401

EffectVariance | 859.3624

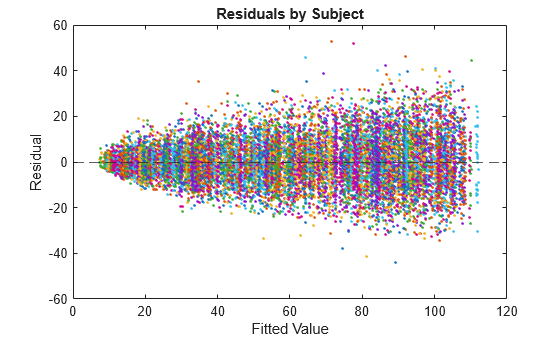

Compute model residuals , and plot them against the fitted responses. Color the residuals according to subject ID.

betahat = reshape(EstMdl.Coefficients,1,1,p); alphahat = EstMdl.Effects; Yhat = sum(X.*betahat,3) + alphahat; Residuals = YSim - Yhat; figure plot(Yhat,Residuals,'.') hold on yline(0,"--") hold off title("Residuals by Subject") ylabel("Residual") xlabel("Fitted Value")

The residuals scatter more widely as the fitted values increase. This behavior is indicative of heteroscedasticity. Also, residuals appear clustered by groups.

Refit the model; compute robust covariance estimates.

EstMdlRobust = fitrepanel(X,YSim,RobustCovariance=true);

Panel data information:

Number of cross-sectional units (N): 1000

Number of periods (T): 15

Number of observations: 15000

Method of estimation: random effects (GLS)

| Estimator SE tStat pValue

----------------------------------------------------------

x1 | 0.0196 0.0191 1.0222 0.3067

x2 | 1.4279 2.8975 0.4928 0.6222

x3 | -0.1095 0.3417 -0.3205 0.7486

x4 | -2.0201 3.5807 -0.5642 0.5726

x5 | 0.3700 0.2755 1.3431 0.1792

x6 | -0.2306 0.3215 -0.7174 0.4731

x7 | 0.9527 0.6701 1.4218 0.1551

x8 | 0.1847 0.4344 0.4253 0.6706

x9 | 0.3463 0.6501 0.5327 0.5942

x10 | -0.0337 0.2976 -0.1133 0.9098

x11 | 0.0070 0.0159 0.4414 0.6589

DisturbanceVariance | 101.9401

EffectVariance | 859.3624

The coefficient estimates between the regular and robust runs are the same; the difference between the runs is in the inferences.

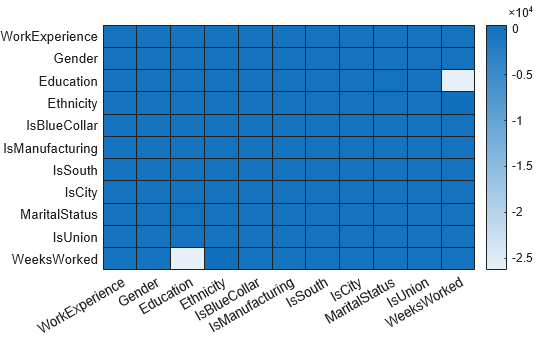

Plot a heatmap of the difference between the estimated coefficient covariance matrix.

seriesSim = series(1:p); heatmap(seriesSim,seriesSim,(EstMdlRobust.CoefficientCovariance-EstMdl.CoefficientCovariance)./EstMdl.CoefficientCovariance)

The estimated covariance of the coefficients of Education and WeeksWorked shows the greatest relative difference between the robust and non-robust analyses.

Input Arguments

Name-Value Arguments

Output Arguments

More About

A panel data set contains measurements of

n subjects measured at most T times over a sampling

time frame. Panel data is a type of longitudinal data resulting from an observational study,

rather than a controlled experiment. This distinction impacts regression procedures used to

analyze these types of data sets. (To analyze longitudinal data, see fitlme, fitlmematrix, and fitrm.)

You can format panel data sets in two ways: wide and long. In what follows, an observation is all measurements (predictors xi, i = 1,…,p and response y data) of a subject (gk, k = 1,...,n) at a particular time (tj, j = 1,…,T).

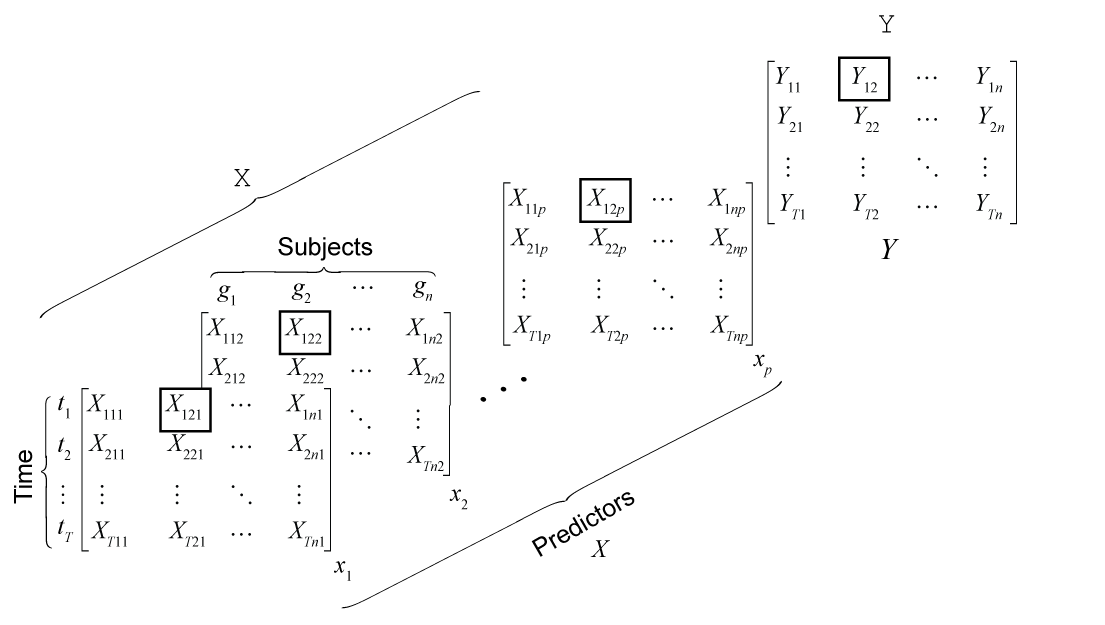

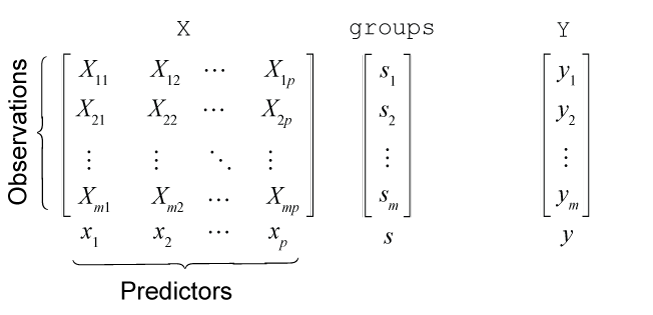

In wide format, the predictor data set X

(input X) is a

T-by-n-by-p 3-D numeric array,

where rows correspond to contemporaneous sampling times in increasing order by row, columns

correspond to individual subjects, and pages correspond to predictor variables. The response

data set Y (input Y) in wide format is a

T-by-n matrix. This figure illustrates the predictor

and response data in wide format.

For a data set in this format, you can clearly infer the sampling time and subject by

its row and column, respectively. An observation of subject

gk at time

tj is the set

{X(,

j,k,:)Y(}. For

example, in the figure, the boxed values comprise the observation of subject

g2 at time

t1.j,k)

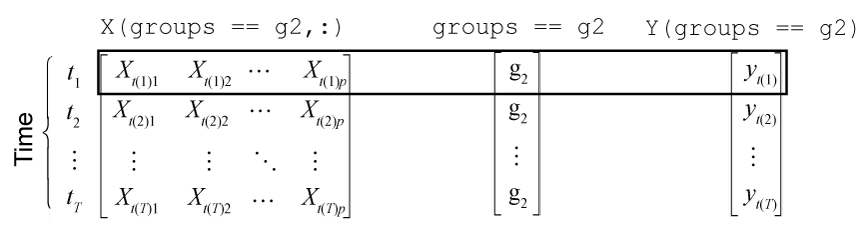

In long format, the predictor data set X is an m-by-p matrix, where the total sample size. Each row contains all predictor measurements of a particular subject at a particular time, and each column is a predictor variable. The response data set y is an m-by-1 vector, where each row is the response of the corresponding subject at the corresponding time. For data in this format, one cannot infer to which subject and sampling time each observation belongs. A variable of subject identifiers (group variable), an m-by-1 vector, is required. For each subject, observations are recorded in increasing order by row. This figure illustrates the predictor and response data in long format.

Row j of the subject identifier vector

sj is in the set

{g1,g2,…,gn}.

This figure illustrates the variables for all observations of subject

g2 (s =

g2, coded as g2). In the

figure, tj =

t(j). Because only those observations belonging to

subject g2 are displayed, the row indices are not

clear, but the sampling times are clear and, therefore, labeled.

An observation of subject gk at time

tj is the set

{Xgk(,

j,:)Ygk(}, where j)Xgk = X(groups ==

g and k,:)Ygk =

Y(groups == g. For example,

in the figure, the boxed values comprise the observation of subject

g2 at time

t1.k)

Panel data functionality accepts data in matrices, tables, and timetables. A panel data

set in a table or timetable is in long format; the Time variable of a

timetable specifies the sampling times of the observations.

Regardless of format, when the data set contains measurements for all subjects and sampling times, the data set is balanced. Otherwise, the data set is unbalanced.

Algorithms

References

Version History

Introduced in R2026a