Fitting the Diebold Li Model

This example shows how to construct a Diebold Li model of the US yield curve for each month from 1990 to 2010. This example also demonstrates how to forecast future yield curves by fitting an autoregressive model to the time series of each parameter.

This example is based on the following paper:

https://www.nber.org/papers/w10048

Load the Data

The data used are monthly Treasury yields from 1990 through 2010 for tenors of 1 Mo, 3 Mo, 6 Mo, 1 Yr, 2 Yr, 3 Yr, 5 Yr, 7 Yr, 10 Yr, 20 Yr, 30 Yr.

Daily data can be found here:

Data is stored in a MATLAB® data file as a timetable.

opts = detectImportOptions("dailyYieldData.xlsx"); opts = setvartype(opts,"double"); opts = setvartype(opts,"Time","datetime"); dailyData = readtimetable("dailyYieldData.xlsx", opts)

dailyData=5256×11 timetable

Time x1M x3M x6M x1Y x2Y x3Y x5Y x7Y x10Y x20Y x30Y

___________ ___ ______ ______ ______ ______ ______ ______ ______ ______ ____ ______

02-Jan-1990 NaN 0.0783 0.0789 0.0781 0.0787 0.079 0.0787 0.0798 0.0794 NaN 0.08

03-Jan-1990 NaN 0.0789 0.0794 0.0785 0.0794 0.0796 0.0792 0.0804 0.0799 NaN 0.0804

04-Jan-1990 NaN 0.0784 0.079 0.0782 0.0792 0.0793 0.0791 0.0802 0.0798 NaN 0.0804

05-Jan-1990 NaN 0.0779 0.0785 0.0779 0.079 0.0794 0.0792 0.0803 0.0799 NaN 0.0806

08-Jan-1990 NaN 0.0779 0.0788 0.0781 0.079 0.0795 0.0792 0.0805 0.0802 NaN 0.0809

09-Jan-1990 NaN 0.078 0.0782 0.0778 0.0791 0.0794 0.0792 0.0805 0.0802 NaN 0.081

10-Jan-1990 NaN 0.0775 0.0778 0.0777 0.0791 0.0795 0.0792 0.08 0.0803 NaN 0.0811

11-Jan-1990 NaN 0.078 0.078 0.0777 0.0791 0.0795 0.0794 0.0801 0.0804 NaN 0.0811

12-Jan-1990 NaN 0.0774 0.0781 0.0776 0.0793 0.0798 0.0799 0.0807 0.081 NaN 0.0817

16-Jan-1990 NaN 0.0789 0.0799 0.0792 0.081 0.0813 0.0811 0.0818 0.082 NaN 0.0825

17-Jan-1990 NaN 0.0797 0.0797 0.0791 0.0809 0.0811 0.0811 0.0817 0.0819 NaN 0.0825

18-Jan-1990 NaN 0.0804 0.0808 0.0805 0.0825 0.0828 0.0827 0.0831 0.0832 NaN 0.0835

19-Jan-1990 NaN 0.08 0.0801 0.08 0.082 0.0823 0.082 0.0824 0.0826 NaN 0.0829

22-Jan-1990 NaN 0.0799 0.0799 0.0798 0.0818 0.082 0.0819 0.0825 0.0827 NaN 0.0831

23-Jan-1990 NaN 0.0793 0.0797 0.0797 0.0818 0.082 0.0818 0.0823 0.0826 NaN 0.0829

24-Jan-1990 NaN 0.0793 0.0799 0.08 0.082 0.0829 0.0828 0.0834 0.0838 NaN 0.0841

⋮

Extract data for the last day of each month.

Estimationdataset = retime(dailyData, "monthly", "lastvalue")

Estimationdataset=252×11 timetable

Time x1M x3M x6M x1Y x2Y x3Y x5Y x7Y x10Y x20Y x30Y

___________ ___ ______ ______ ______ ______ ______ ______ ______ ______ ____ ______

01-Jan-1990 NaN 0.08 0.0813 0.0808 0.0828 0.0836 0.0835 0.0839 0.0843 NaN 0.0846

01-Feb-1990 NaN 0.0804 0.0814 0.0812 0.0843 0.0845 0.0844 0.0854 0.0851 NaN 0.0854

01-Mar-1990 NaN 0.0807 0.0824 0.0835 0.0864 0.0869 0.0865 0.087 0.0865 NaN 0.0863

01-Apr-1990 NaN 0.0807 0.0844 0.0858 0.0896 0.0905 0.0904 0.0906 0.0904 NaN 0.09

01-May-1990 NaN 0.0801 0.0812 0.0822 0.085 0.0853 0.0856 0.0864 0.086 NaN 0.0858

01-Jun-1990 NaN 0.08 0.0802 0.0805 0.0824 0.0832 0.0835 0.0846 0.0843 NaN 0.0841

01-Jul-1990 NaN 0.0774 0.0772 0.0772 0.0791 0.0804 0.0813 0.0828 0.0836 NaN 0.0842

01-Aug-1990 NaN 0.0763 0.0774 0.0776 0.0807 0.0826 0.085 0.0877 0.0886 NaN 0.0899

01-Sep-1990 NaN 0.0737 0.0754 0.0769 0.0802 0.0819 0.0847 0.0873 0.0882 NaN 0.0896

01-Oct-1990 NaN 0.0734 0.0746 0.0743 0.0777 0.0797 0.0824 0.085 0.0865 NaN 0.0878

01-Nov-1990 NaN 0.0724 0.0736 0.0731 0.0753 0.0767 0.0791 0.0818 0.0826 NaN 0.084

01-Dec-1990 NaN 0.0663 0.0673 0.0682 0.0715 0.074 0.0768 0.08 0.0808 NaN 0.0826

01-Jan-1991 NaN 0.0637 0.0649 0.0651 0.0705 0.073 0.0762 0.0789 0.0803 NaN 0.0821

01-Feb-1991 NaN 0.0622 0.0632 0.0641 0.0704 0.0726 0.0766 0.0789 0.0802 NaN 0.0819

01-Mar-1991 NaN 0.0592 0.0605 0.0628 0.0702 0.073 0.0773 0.0796 0.0805 NaN 0.0824

01-Apr-1991 NaN 0.0568 0.0583 0.0606 0.068 0.0715 0.0763 0.0788 0.0802 NaN 0.082

⋮

EstimationData = table2array(Estimationdataset)

EstimationData = 252×11

NaN 0.0800 0.0813 0.0808 0.0828 0.0836 0.0835 0.0839 0.0843 NaN 0.0846

NaN 0.0804 0.0814 0.0812 0.0843 0.0845 0.0844 0.0854 0.0851 NaN 0.0854

NaN 0.0807 0.0824 0.0835 0.0864 0.0869 0.0865 0.0870 0.0865 NaN 0.0863

NaN 0.0807 0.0844 0.0858 0.0896 0.0905 0.0904 0.0906 0.0904 NaN 0.0900

NaN 0.0801 0.0812 0.0822 0.0850 0.0853 0.0856 0.0864 0.0860 NaN 0.0858

NaN 0.0800 0.0802 0.0805 0.0824 0.0832 0.0835 0.0846 0.0843 NaN 0.0841

NaN 0.0774 0.0772 0.0772 0.0791 0.0804 0.0813 0.0828 0.0836 NaN 0.0842

NaN 0.0763 0.0774 0.0776 0.0807 0.0826 0.0850 0.0877 0.0886 NaN 0.0899

NaN 0.0737 0.0754 0.0769 0.0802 0.0819 0.0847 0.0873 0.0882 NaN 0.0896

NaN 0.0734 0.0746 0.0743 0.0777 0.0797 0.0824 0.0850 0.0865 NaN 0.0878

NaN 0.0724 0.0736 0.0731 0.0753 0.0767 0.0791 0.0818 0.0826 NaN 0.0840

NaN 0.0663 0.0673 0.0682 0.0715 0.0740 0.0768 0.0800 0.0808 NaN 0.0826

NaN 0.0637 0.0649 0.0651 0.0705 0.0730 0.0762 0.0789 0.0803 NaN 0.0821

NaN 0.0622 0.0632 0.0641 0.0704 0.0726 0.0766 0.0789 0.0802 NaN 0.0819

NaN 0.0592 0.0605 0.0628 0.0702 0.0730 0.0773 0.0796 0.0805 NaN 0.0824

⋮

dates = Estimationdataset.Properties.RowTimes;

Diebold Li Model

Diebold and Li start with the Nelson Siegel model

and rewrite it to be the following:

The above model allows the factors to be interpreted in the following way: Beta1 corresponds to the long term/level of the yield curve, Beta2 corresponds to the short term/slope, and Beta3 corresponds to the medium term/curvature. determines the maturity at which the loading on the curvature is maximized, and governs the exponential decay rate of the model.

Diebold and Li advocate setting to maximize the loading on the medium term factor, Beta3, at 30 months. This also transforms the problem from a nonlinear fitting to a simple linear regression.

% Explicitly set the time factor lambda. lambda_t = .0609; % Construct a matrix of the factor loadings. % Tenors associated with the data. TimeToMat = [3 6 9 12 24 36 60 84 120 240 360]'; X = [ones(size(TimeToMat)) (1 - exp(-lambda_t*TimeToMat))./(lambda_t*TimeToMat) ... ((1 - exp(-lambda_t*TimeToMat))./(lambda_t*TimeToMat) - exp(-lambda_t*TimeToMat))]; % Plot the factor loadings. plot(TimeToMat,X) title("Factor Loadings for Diebold Li Model with Time Factor of .0609") xlabel("Maturity (months)") ylim([0 1.1]) legend(["Beta1","Beta2","Beta3"],"location","east")

Fit the Model

A DieboldLi object is developed to facilitate fitting the model from yield data. The DieboldLi object inherits from the IRCurve object, so the getZeroRates, getDiscountFactors, getParYields, getForwardRates, and toRateSpec methods are all implemented. Additionally, the method fitYieldsFromBetas is implemented to estimate the Beta parameters given a lambda parameter for observed market yields.

The DieboldLi object is used to fit a Diebold Li model for each month from 1990 through 2010.

% Preallocate the Betas. Beta = zeros(size(EstimationData,1),3); % Loop through and fit each end of month yield curve. for jdx = 1:size(EstimationData,1) tmpCurveModel = DieboldLi.fitBetasFromYields(dates(jdx),lambda_t*12,dates(jdx) + calmonths(TimeToMat),EstimationData(jdx,:)'); Beta(jdx,:) = [tmpCurveModel.Beta1 tmpCurveModel.Beta2 tmpCurveModel.Beta3]; end

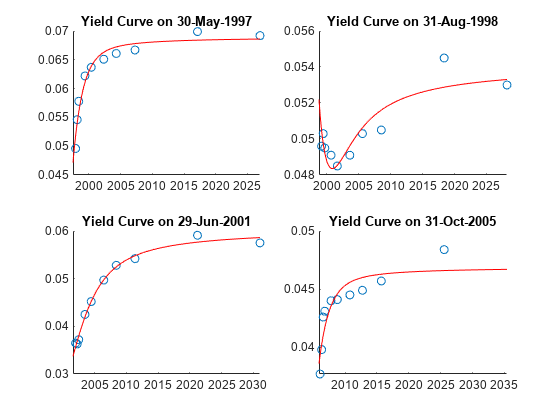

The Diebold Li fits on selected dates are included here. While this example uses EOM data, the time stamps are for the first of each month.

PlotSettles = datetime([1997, 1998, 2001, 2005], [5,8,6,10], 1); lambda_annual = lambda_t*12; for jdx = 1:length(PlotSettles) subplot(2,2,jdx) tmpIdx = find(PlotSettles(jdx)==dates); tmpCurveModel = DieboldLi.fitBetasFromYields(PlotSettles(jdx),lambda_annual, ... PlotSettles(jdx)+calmonths(TimeToMat),EstimationData(tmpIdx,:)'); scatter(PlotSettles(jdx)+calmonths(TimeToMat),EstimationData(tmpIdx,:)) hold on PlottingDates = PlotSettles(jdx)+calmonths(1:360)'; plot(PlottingDates,tmpCurveModel.getParYields(PlottingDates),"r-") hold off title("Yield Curve on " + datestr(dateshift(PlotSettles(jdx), "end", "month"))) end

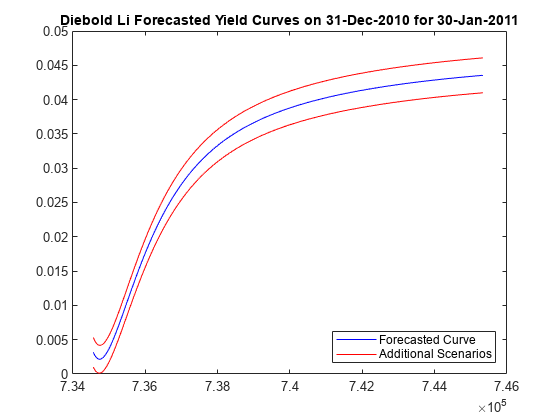

Forecasting

The Diebold Li model can be used to forecast future yield curves. Diebold and Li propose fitting an AR(1) model to the time series of each Beta parameter. This fitted model is then used to forecast future values of each parameter, and by extension, future yield curves.

For this example the MATLAB function fitlm is used to estimate the parameters for an AR(1) model for each Beta.

The confidence intervals for the regression fit are also used to generate two additional yield curve forecasts that serve as additional possible scenarios for the yield curve.

You can adjust The MonthsLag variable to make different period ahead forecasts. For example, changing the value from 1 to 6 would change the forecast from a 1 month ahead to a 6 months ahead forecast.

MonthsLag = 1; ForecastBeta = zeros(1,3); ForecastBeta_Down = zeros(1,3); ForecastBeta_Up = zeros(1,3); for k = 1:3 % for each Beta currentFit = fitlm( Beta(1:end-MonthsLag,k), Beta(MonthsLag+1:end,k)); tmpBeta = currentFit.Coefficients.Estimate; bint = coefCI(currentFit); ForecastBeta(k) = [1 Beta(end,k)]*tmpBeta; ForecastBeta_Down(k) = [1 Beta(end,k)]*bint(:,1); ForecastBeta_Up(k) = [1 Beta(end,k)]*bint(:,2); end % Forecasted yield curve figure Settle = dates(end) + calmonths(MonthsLag); DieboldLi_Forecast = DieboldLi("ParYield",Settle,[ForecastBeta lambda_annual]); DieboldLi_Forecast_Up = DieboldLi("ParYield",Settle,[ForecastBeta_Up lambda_annual]); DieboldLi_Forecast_Down = DieboldLi("ParYield",Settle,[ForecastBeta_Down lambda_annual]); PlottingDates = Settle+calmonths(1:360)'; plot(PlottingDates,DieboldLi_Forecast.getParYields(PlottingDates),"b-") hold on plot(PlottingDates,DieboldLi_Forecast_Up.getParYields(PlottingDates),"r-") plot(PlottingDates,DieboldLi_Forecast_Down.getParYields(PlottingDates),"r-") hold off title("Diebold Li Forecasted Yield Curves on " + datestr(dates(end)) + " for " + datestr(Settle)) legend(["Forecasted Curve","Additional Scenarios"],"location","southeast")

Bibliography

This example is based on the following paper:

[1] Francis X. Diebold, Canlin Li. "Forecasting the Term Structure of Government Bond Yields." Journal of Econometrics, Volume 130, Issue 2, February 2006, pp. 337–364.

See Also

convfactor | bndfutprice | bndfutimprepo | tfutbyprice | tfutbyyield | tfutimprepo | tfutpricebyrepo | tfutyieldbyrepo | bnddurp | bnddury