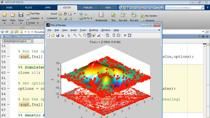

MATLAB for Portfolio Construction: Smart Beta

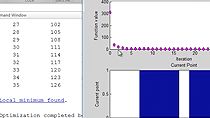

Standard asset allocation problems such as mean variance or conditional value-at-risk can be easily developed and solved using MATLAB® and Financial Toolbox™. Other portfolio construction methods that may have a custom risk measurement or satisfy a different trading style or mandate can also be solved using MATLAB and toolboxes such as Optimization Toolbox™.

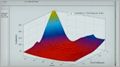

Many modern investors are following a new approach called Smart Beta - finding alternative weights for indices that are not based around market capitalization. One of these approaches is risk parity, where a portfolio is constructed with each asset having equal contributions to total portfolio risk.

Published: 10 Mar 2016