egcitest

Engle-Granger cointegration test

Syntax

Description

h = egcitest(Y)egcitest forms test statistics by regressing the

response data Y(:,1) onto the predictor data

Y(:,2:end), and then it tests the residuals for a unit root.

StatTbl = egcitest(Tbl)

The response variable in the regression is the first table variable, and all other

variables are the predictor variables. To select a different response variable for the

regression, use the ResponseVariable name-value argument. To select

different predictor variables, use the PredictorNames name-value

argument.

[___] = egcitest(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)egcitest returns the output argument combination for the

corresponding input arguments.

Some options control the number of tests to conduct. The following conditions apply when

egcitest conducts multiple tests:

For example, egcitest(Tbl,ResponseVariable="GDP",Alpha=0.025,Lags=[0

1]) chooses GDP as the response variable from the table

Tbl and conducts two tests at a level of significance of 0.025. The

first test includes 0 lag in the residual regression, and the second test

includes 1 lag in the residual regression.

[___,

additionally returns the following structures of regression statistics, which are required

to form the test statistic:reg1,reg2] = egcitest(___)

reg1– Statistics resulting from the cointegrating regression of the specified response variableResponseVariableonto the specified predictor variablesPredictorVariablesreg2– Statistics resulting from the residual regression implemented by the specified unit root testRReg

Examples

Test a multivariate time series for cointegration using the default values of the Engle-Granger cointegration test. Input the time series data as a numeric matrix.

Load data of Canadian inflation and interest rates Data_Canada.mat, which contains the series in the matrix Data.

load Data_Canada

series'ans = 5×1 cell

{'(INF_C) Inflation rate (CPI-based)' }

{'(INF_G) Inflation rate (GDP deflator-based)'}

{'(INT_S) Interest rate (short-term)' }

{'(INT_M) Interest rate (medium-term)' }

{'(INT_L) Interest rate (long-term)' }

Test the interest rate series for cointegration by using the Engle-Granger cointegration test. Use default options and return the rejection decision and -value.

h = egcitest(Data(:,3:end))

h = logical

0

egcitest uses the test by default, and it fails to reject the null hypothesis (h = 0) of no cointegration among the interest rate series.

Load data of Canadian inflation and interest rates Data_Canada.mat.

load Data_CanadaTest the interest rate series for cointegration by using the Engle-Granger cointegration test. Use default options and return the rejection decision, -value, -test statistic, and critical value.

[h,pValue,stat,cValue] = egcitest(Data(:,3:end))

h = logical

0

pValue = 0.0526

stat = -3.9321

cValue = -3.9563

Conduct the Engle-Granger cointegration test on a multivariate time series using default options, which use the first table variable as the response, all other table variables as predictors, and includes a constant term in the cointegrating regression. Return a table of test results.

Load data of Canadian inflation and interest rates Data_Canada.mat. Convert the table DataTable to a timetable.

load Data_Canada

dates = datetime(dates,12,31);

TT = table2timetable(DataTable,RowTimes=dates);

TT.Observations = [];Conduct the Engel-Granger cointegration test by passing the timetable to egcitest and using default options. For the cointegrating regression, egcitest uses the CPI-based inflation rate as the response variable and all other variables in the timetable as predictors.

StatTbl = egcitest(TT)

StatTbl=1×9 table

h pValue stat cValue Lags Alpha Test CReg RReg

_____ _________ _______ _______ ____ _____ ______ _____ _______

Test 1 true 0.0023851 -6.2491 -4.7673 0 0.05 {'t1'} {'c'} {'ADF'}

StatTbl is a table of test results. The rows correspond to variables in the input timetable TT, and the columns correspond to the rejection decision, and corresponding -value, decision statistics, and specified test options. In this case, the test rejects the null hypothesis in favor of the alternative of cointegration among all the table variables.

By default, egcitest includes all input table variables in the cointegration test. To select a response variable for the cointegrating regression, set the ResponseVariable option. To select predictor variables, set the PredictorVariables option.

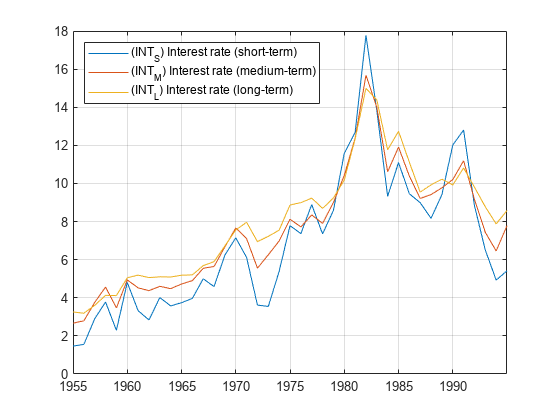

Load data of Canadian inflation and interest rates Data_Canada.mat. Convert the table DataTable to a timetable of the interest rate series only.

load Data_Canada dates = datetime(dates,12,31); idxINT = contains(DataTable.Properties.VariableNames,"INT"); TT = table2timetable(DataTable(:,idxINT),RowTimes=dates); TT.Observations = [];

Plot the interest rate series.

figure plot(TT.Time,TT.Variables) legend(series(idxINT),Location="northwest") grid on

Reproduce row 1 of Table II in [3] by testing for cointegration, specifying the default variable assignments for the cointegrating regression and deterministic terms (response variable is INT_S, the other interest rates and are predictors, and the model has a constant ), and specifying the and tests. Return the cointegrating regression statistics.

[StatTbl,reg] = egcitest(TT,Test=["t1" "t2"]); StatTbl

StatTbl=2×9 table

h pValue stat cValue Lags Alpha Test CReg RReg

_____ ________ _______ _______ ____ _____ ______ _____ _______

Test 1 false 0.052627 -3.9321 -3.9563 0 0.05 {'t1'} {'c'} {'ADF'}

Test 2 true 0.020157 -25.454 -22.115 0 0.05 {'t2'} {'c'} {'ADF'}

The test (Test 1) fails to reject the null hypothesis, but the test (Test 2) rejects the null hypothesis in favor of the presence of cointegration.

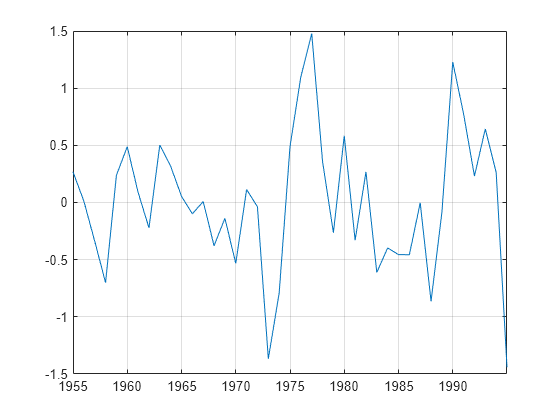

Plot the estimated cointegrating relation using the regression statistics from the test , where .

c = reg(2).coeff(1);

b = reg(2).coeff(2:3);

figure

plot(TT.Time,TT.Variables*[1; -b] - c)

grid on

Input Arguments

Name-Value Arguments

Output Arguments

Tips

To draw valid inferences from the test, determine a suitable value for

Lags. For more details, see theadftestTips and thepptestTips.Samples with less than approximately 20 through 40 observations (depending on the dimension of the data

numDims) can yield unreliable critical values, and therefore unreliable inferences. See [3].If a test result suggests that the time series are cointegrated, you can use the residuals as data for the error-correction term in a VEC representation of the variables. Follow this procedure:

Alternative Functionality

App

The Econometric Modeler app enables you to conduct the Engle-Granger cointegration test.

References

[2] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

Version History

Introduced in R2011a