simulate

Monte Carlo simulation of conditional variance models

Syntax

Description

V = simulate(Mdl,numobs,Name=Value)simulate(Mdl,100,NumPaths=1000,V0=v0) returns a numeric

matrix of 1000, 100-period simulated conditional variance paths from

Mdl and specifies the numeric vector of presample

conditional variances v0 to initialize each returned

path.

To produce a conditional simulation, specify response data in the simulation

horizon by using the YF name-value argument.

Tbl = simulate(Mdl,numobs,Presample=Presample,Name=Value)Tbl containing the random

conditional variance and response series, which results from simulating the

model Mdl. simulate uses the table

or timetable of innovations or conditional variance presample data

Presample to initialize the model. If you specify

Presample, you must specify the variable containing the

presample innovation or conditional variance data by using the

PresampleInnovationVariable or

PresampleVarianceVariable name-value argument.

Examples

Simulate conditional variance and response paths from a GARCH(1,1) model. Return results in numeric matrices.

Specify a GARCH(1,1) model with known parameters.

Mdl = garch(Constant=0.01,GARCH=0.7,ARCH=0.2);

Simulate 500 sample paths, each with 100 observations.

rng("default") % For reproducibility [V,Y] = simulate(Mdl,100,NumPaths=500);

V and Y are 100-by-500 matrices of 500 simulated paths of conditional variances and responses, respectively.

figure tiledlayout(2,1) nexttile plot(V) title("Simulated Conditional Variances") nexttile plot(Y) title("Simulated Responses")

The simulated responses look like draws from a stationary stochastic process.

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated conditional variances.

lower = prctile(V,2.5,2); middle = median(V,2); upper = prctile(V,97.5,2); figure plot(1:100,lower,"r:",1:100,middle,"k", ... 1:100,upper,"r:",LineWidth=2) legend("95% Confidence interval","Median") title("Approximate 95% Intervals")

The intervals are asymmetric due to positivity constraints on the conditional variance.

Simulate conditional variance and response paths from an EGARCH(1,1) model.

Specify an EGARCH(1,1) model with known parameters.

Mdl = egarch(Constant=0.001,GARCH=0.7,ARCH=0.2, ...

Leverage=-0.3);Simulate 500 sample paths, each with 100 observations.

rng("default") % For reproducibility [V,Y] = simulate(Mdl,100,NumPaths=500); figure tiledlayout(2,1) nexttile plot(V) title("Simulated Conditional Variances") nexttile plot(Y) title("Simulated Responses (Innovations)")

The simulated responses look like draws from a stationary stochastic process.

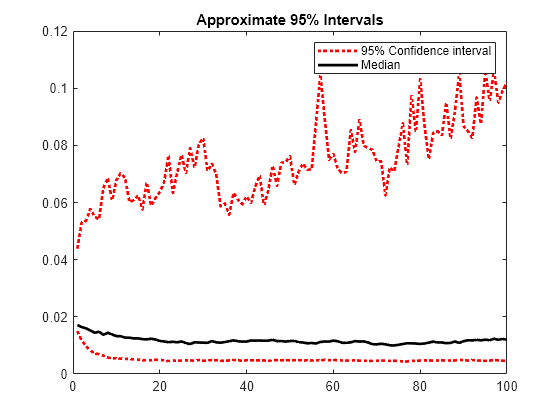

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated conditional variances.

lower = prctile(V,2.5,2); middle = median(V,2); upper = prctile(V,97.5,2); figure plot(1:100,lower,"r:",1:100,middle,"k", ... 1:100, upper,"r:",LineWidth=2) legend("95% Confidence interval","Median") title("Approximate 95% Intervals")

The intervals are asymmetric due to positivity constraints on the conditional variance.

Simulate conditional variance and response paths from a GJR(1,1) model.

Specify a GJR(1,1) model with known parameters.

Mdl = gjr(Constant=0.001,GARCH=0.7,ARCH=0.2, ...

Leverage=0.1);Simulate 500 sample paths, each with 100 observations.

rng("default") % For reproducibility [V,Y] = simulate(Mdl,100,NumPaths=500); figure tiledlayout(2,1) nexttile plot(V) title("Simulated Conditional Variances") nexttile plot(Y) title("Simulated Responses (Innovations)")

The simulated responses look like draws from a stationary stochastic process.

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated conditional variances.

lower = prctile(V,2.5,2); middle = median(V,2); upper = prctile(V,97.5,2); figure plot(1:100,lower,"r:",1:100,middle,"k", ... 1:100, upper,"r:",LineWidth=2) legend("95% Confidence interval","Median") title("Approximate 95% Intervals")

The intervals are asymmetric due to positivity constraints on the conditional variance.

Since R2023a

Simulate conditional variances of the average weekly closing NASDAQ returns for 100 weeks. Use the simulations to make forecasts and approximate 95% forecast intervals. Compare the forecasts among GARCH(1,1), EGARCH(1,1), and GJR(1,1) fits. Supply timetables of presample data.

Load the U.S. equity indices data Data_EquityIdx.mat.

load Data_EquityIdxThe timetable DataTimeTable contains the daily NASDAQ closing prices, among other indices.

Compute the weekly average closing prices of all timetable variables.

DTTW = convert2weekly(DataTimeTable,Aggregation="mean");Compute the weekly returns.

DTTRet = price2ret(DTTW); DTTRet.Interval = []; T = height(DTTRet)

T = 626

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable, relative to the NASDAQ returns series.

DTTRet = rmmissing(DTTRet,DataVariables="NASDAQ");

numobs = height(DTTRet)numobs = 626

Because all sample times have observed NASDAQ returns, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTTRet,"weeks")areTimestampsRegular = logical

1

areTimestampsSorted = issorted(DTTRet.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 1 indicates that the timestamps of DTTRet represent a regular weekly sample. areTimestampsSorted = 1 indicates that the timestamps are sorted.

Fit GARCH(1,1), EGARCH(1,1), and GJR(1,1) models to the entire data set.

Mdl = cell(3,1); % Preallocation Mdl{1} = garch(1,1); Mdl{2} = egarch(1,1); Mdl{3} = gjr(1,1); EstMdl = cellfun(@(x)estimate(x,DTTRet,ResponseVariable="NASDAQ", ... Display="off"),Mdl,UniformOutput=false);

EstMdl is 3-by-1 cell vector. Each cell is a different type of estimated conditional variance model, e.g., EstMdl{1} is an estimated GARCH(1,1) model.

Simulate 1000 samples paths with 100 observations each. Infer conditional variances and residuals to use as a presample for the forecast simulation.

T0 = 100; DTTSim = cell(3,1); % Preallocation PS = cell(3,1); for j = 1:3 rng("default") % For reproducibility PS{j} = infer(EstMdl{j},DTTRet,ResponseVariable="NASDAQ"); DTTSim{j} = simulate(EstMdl{j},T0,NumPaths=1000, ... Presample=PS{j},PresampleInnovationVariable="Y_Residual", ... PresampleVarianceVariable="Y_Variance"); end

DTTSim is a 3-by-1 cell vector, and each cell contains a 100-by-2 timetable of 1000 simulated paths of conditional variances and responses generated from the corresponding estimated model.

Plot the simulation mean forecasts and approximate 95% forecast intervals, along with the conditional variances inferred from the data.

lower = cellfun(@(x)prctile(x.Y_Variance,2.5,2),DTTSim,UniformOutput=false); upper = cellfun(@(x)prctile(x.Y_Variance,97.5,2),DTTSim,UniformOutput=false); mn = cellfun(@(x)mean(x.Y_Variance,2),DTTSim,UniformOutput=false); datesPlot = DTTRet.Time(end - 50:end); datesFH = DTTRet.Time(end) + caldays(1:100)'; h = zeros(3,4); figure for j = 1:3 col = zeros(1,3); col(j) = 1; h(j,1) = plot(datesPlot,PS{j}.Y_Variance(end-50:end),Color=col); hold on h(j,2) = plot(datesFH,mn{j},Color=col,LineWidth=3); h(j,3:4) = plot([datesFH datesFH],[lower{j} upper{j}],":", ... Color=col,LineWidth=2); end hGCA = gca; plot(datesFH([1 1]),hGCA.YLim,"k--"); axis tight; h = h(:,1:3); legend(h(:),'GARCH - Inferred','EGARCH - Inferred','GJR - Inferred',... 'GARCH - Sim. Mean','EGARCH - Sim. Mean','GJR - Sim. Mean',... 'GARCH - 95% Fore. Int.','EGARCH - 95% Fore. Int.',... 'GJR - 95% Fore. Int.','Location','NorthEast') title('Simulated Conditional Variance Forecasts') hold off

Input Arguments

Name-Value Arguments

Output Arguments

References

[1] Bollerslev, T. “Generalized Autoregressive Conditional Heteroskedasticity.” Journal of Econometrics. Vol. 31, 1986, pp. 307–327.

[2] Bollerslev, T. “A Conditionally Heteroskedastic Time Series Model for Speculative Prices and Rates of Return.” The Review of Economics and Statistics. Vol. 69, 1987, pp. 542–547.

[3] Box, G. E. P., G. M. Jenkins, and G. C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[4] Enders, W. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, 1995.

[5] Engle, R. F. “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation.” Econometrica. Vol. 50, 1982, pp. 987–1007.

[6] Glosten, L. R., R. Jagannathan, and D. E. Runkle. “On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks.” The Journal of Finance. Vol. 48, No. 5, 1993, pp. 1779–1801.

[7] Hamilton, J. D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[8] Nelson, D. B. “Conditional Heteroskedasticity in Asset Returns: A New Approach.” Econometrica. Vol. 59, 1991, pp. 347–370.