gctest

Block-wise Granger causality and block exogeneity tests

Syntax

Description

The gctest function conducts a block-wise Granger causality test by accepting sets of time series data representing the "cause" and "effect" multivariate response variables in the test. gctest supports the inclusion of optional endogenous conditioning variables in the model for the test.

To conduct the leave-one-out, exclude-all, and block-wise Granger causality tests on the response variables of a fully specified VAR model (represented by a varm model object), see gctest.

h = gctest(Y1,Y2)gctest function conducts tests in the vector autoregression (VAR)

framework and treats the input arrays as response (endogenous) variables during

testing.

h = gctest(Y1,Y2,Y3)Y3 is endogenous in the underlying VAR model, but

gctest does not consider it a "cause" or an "effect" in the

test.

StatTbl = gctest(Tbl)

To select different Granger-cause or effect variables for the test, use the

CauseVariables or EffectVariables name-value

argument.

___ = gctest(___,

specifies options using one or more name-value arguments. For example,

Name,Value)gctest(Y1,Y2,Test="f",NumLags=2) specifies conducting an

F test that compares the residual sum of squares between restricted

and unrestricted VAR(2) models for all response variables.

gctest returns the output argument combination for the

corresponding input arguments.

Examples

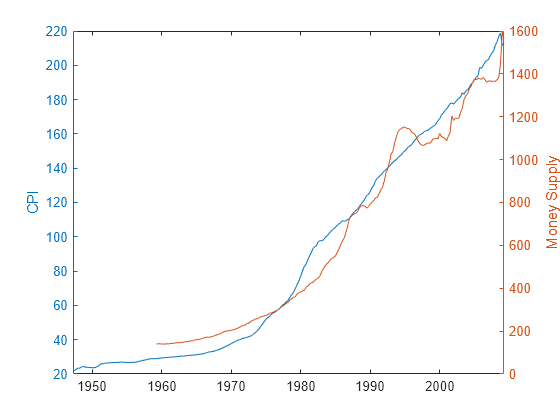

Conduct a Granger causality test to assess whether the M1 money supply has an impact on the predictive distribution of the consumer price index (CPI). Supply data as numeric vectors.

Load the US macroeconomic data set Data_USEconModel.mat.

load Data_USEconModelThe data set includes the MATLAB® timetable DataTimeTable, which contains 14 variables measured from Q1 1947 through Q1 2009. M1SL is the table variable containing the M1 money supply, and CPIAUCSL is the table variable containing the CPI. For more details, enter Description at the command line.

Visually assess whether the series are stationary by plotting them in the same figure.

figure; yyaxis left plot(DataTimeTable.Time,DataTimeTable.CPIAUCSL) ylabel("CPI"); yyaxis right plot(DataTimeTable.Time,DataTimeTable.M1SL); ylabel("Money Supply");

Both series are nonstationary.

Stabilize the series by converting them to rates.

m1slrate = price2ret(DataTimeTable.M1SL); inflation = price2ret(DataTimeTable.CPIAUCSL);

Assume that a VAR(1) model is an appropriate multivariate model for the rates. Conduct a default Granger causality test to assess whether the M1 money supply rate Granger-causes the inflation rate.

h = gctest(m1slrate,inflation)

h = logical

1

The test decision h is 1, which indicates the rejection of the null hypothesis that the M1 money supply rate does not Granger-cause inflation.

Time series undergo feedback when they Granger-cause each other. Assess whether the US inflation and M1 money supply rates undergo feedback.

Load the US macroeconomic data set Data_USEconModel.mat. Convert the price series to returns.

load Data_USEconModel

inflation = price2ret(DataTimeTable.CPIAUCSL);

m1slrate = price2ret(DataTimeTable.M1SL);Conduct a Granger causality test to assess whether the inflation rate Granger-causes the M1 money supply rate. Assume that an underlying VAR(1) model is appropriate for the two series. The default level of significance for the test is 0.05. Because this example conducts two tests, decrease by half for each test to achieve a family-wise level of significance of 0.05.

hIRgcM1 = gctest(inflation,m1slrate,Alpha=0.025)

hIRgcM1 = logical

1

The test decision hIRgcM1 = 1 indicates rejection of the null hypothesis of noncausality. There is enough evidence to suggest that the inflation rate Granger-causes the M1 money supply rate at 0.025 level of significance.

Conduct another Granger causality test to assess whether the M1 money supply rate Granger-causes the inflation rate.

hM1gcIR = gctest(m1slrate,inflation,Alpha=0.025)

hM1gcIR = logical

0

The test decision hM1gcIR = 0 indicates that the null hypothesis of noncausality should not be rejected. There is not enough evidence to suggest that the M1 money supply rate Granger-causes the inflation rate at 0.025 level of significance.

Because not enough evidence exists to suggest that the inflation rate Granger-causes the M1 money supply rate, the two series do not undergo feedback.

Assess whether the US gross domestic product (GDP) Granger-causes CPI conditioned on the M1 money supply.

Load the US macroeconomic data set Data_USEconModel.mat.

load Data_USEconModelThe variables GDP and GDPDEF of DataTimeTable are the US GDP and its deflator with respect to year 2000 dollars, respectively. Both series are nonstationary.

Convert the M1 money supply and CPI to rates. Convert the US GDP to the real GDP rate.

m1slrate = price2ret(DataTimeTable.M1SL); inflation = price2ret(DataTimeTable.CPIAUCSL); rgdprate = price2ret(DataTimeTable.GDP./DataTimeTable.GDPDEF);

Assume that a VAR(1) model is an appropriate multivariate model for the rates. Conduct a Granger causality test to assess whether the real GDP rate has an impact on the predictive distribution of the inflation rate, conditioned on the M1 money supply. The inclusion of a conditional variable forces gctest to conduct a 1-step Granger causality test.

h = gctest(rgdprate,inflation,m1slrate)

h = logical

0

The test decision h is 0, which indicates failure to reject the null hypothesis that the real GDP rate is not a 1-step Granger-cause of inflation when you account for the M1 money supply rate.

gctest includes the M1 money supply rate as a response variable in the underlying VAR(1) model, but it does not include the M1 money supply in the computation of the test statistics.

Conduct the test again, but without conditioning on the M1 money supply rate.

h = gctest(rgdprate,inflation)

h = logical

0

The test result is the same as before, suggesting that the real GDP rate does not Granger-cause inflation at all periods in a forecast horizon and regardless of whether you account for the M1 money supply rate in the underlying VAR(1) model.

By default, gctest assumes an underlying VAR(1) model for all specified response variables. However, a VAR(1) model might be an inappropriate representation of the data. For example, the model might not capture all the serial correlation present in the variables.

To specify a more complex underlying VAR model, you can increase the number of lags by specifying the NumLags name-value argument of gctest.

Consider the Granger causality tests conducted in Conduct 1-Step Granger Causality Test Conditioned on Variable. Load the US macroeconomic data set Data_USEconModel.mat. Convert the M1 money supply and CPI to rates. Convert the US GDP to the real GDP rate.

load Data_USEconModel

m1slrate = price2ret(DataTimeTable.M1SL);

inflation = price2ret(DataTimeTable.CPIAUCSL);

rgdprate = price2ret(DataTimeTable.GDP./DataTimeTable.GDPDEF);Preprocess the data by removing all missing observations (indicated by NaN).

idx = sum(isnan([m1slrate inflation rgdprate]),2) < 1;

m1slrate = m1slrate(idx);

inflation = inflation(idx);

rgdprate = rgdprate(idx);

T = numel(m1slrate); % Total sample sizeFit VAR models, with lags ranging from 1 to 4, to the real GDP and inflation rate series. Initialize each fit by specifying the first four observations. Store the Akaike information criteria (AIC) of the fits.

numseries = 2; numlags = (1:4)'; nummdls = numel(numlags); % Partition time base. maxp = max(numlags); % Maximum number of required presample responses idxpre = 1:maxp; idxest = (maxp + 1):T; % Preallocation EstMdl(1:nummdls) = varm(numseries,0); aic = zeros(nummdls,1); % Fit VAR models to data. Y0 = [rgdprate(idxpre) inflation(idxpre)]; % Presample Y = [rgdprate(idxest) inflation(idxest)]; % Estimation sample for j = 1:numel(numlags) Mdl = varm(numseries,numlags(j)); Mdl.SeriesNames = ["rGDP" "Inflation"]; EstMdl(j) = estimate(Mdl,Y,Y0=Y0); results = summarize(EstMdl(j)); aic(j) = results.AIC; end p = numlags(aic == min(aic))

p = 3

A VAR(3) model yields the best fit.

Assess whether the real GDP rate Granger-causes inflation. gctest removes observations from the beginning of the input data to initialize the underlying VAR() model for estimation. Prepend only the required = 3 presample observations to the estimation sample. Specify the concatenated series as input data. Return the -value of the test.

rgdprate3 = [Y0((end - p + 1):end,1); Y(:,1)]; inflation3 = [Y0((end - p + 1):end,2); Y(:,2)]; [h,pvalue] = gctest(rgdprate3,inflation3,NumLags=p)

h = logical

1

pvalue = 7.7741e-04

The -value is approximately 0.0008, indicating the existence of strong evidence to reject the null hypothesis of noncausality, that is, that the three real GDP rate lags in the inflation rate equation are jointly zero. Given the VAR(3) model, there is enough evidence to suggest that the real GDP rate Granger-causes at least one future value of the inflation rate.

Alternatively, you can conduct the same test by passing the estimated VAR(3) model (represented by the varm model object in EstMdl(3)), to the object function gctest. Specify a block-wise test and the "cause" and "effect" series names.

h = gctest(EstMdl(3),Type="block-wise", ... Cause="rGDP",Effect="Inflation")

H0 Decision Distribution Statistic PValue CriticalValue

____________________________________________ ___________ ____________ _________ __________ _____________

"Exclude lagged rGDP in Inflation equations" "Reject H0" "Chi2(3)" 16.799 0.00077741 7.8147

h = logical

1

If you are testing integrated series for Granger causality, then the Wald test statistic does not follow a or distribution, and test results can be unreliable. However, you can implement the Granger causality test in [5] by specifying the maximum integration order among all the variables in the system using the Integration name-value argument.

Consider the Granger causality tests conducted in Conduct 1-Step Granger Causality Test Conditioned on Variable. Load the US macroeconomic data set Data_USEconModel.mat and take the log of real GDP and CPI.

load Data_USEconModel

cpi = log(DataTimeTable.CPIAUCSL);

rgdp = log(DataTimeTable.GDP./DataTimeTable.GDPDEF);Assess whether the real GDP Granger-causes CPI. Assume the series are , or order-1 integrated. Also, specify an underlying VAR(3) model and the test. Return the test statistic and -value.

[h,pvalue,stat] = gctest(rgdp,cpi,NumLags=3, ... Integration=1,Test="f")

h = logical

1

pvalue = 0.0031

stat = 4.7557

The -value = 0.0031, indicating the existence of strong evidence to reject the null hypothesis of noncausality, that is, that the three real GDP lags in the CPI equation are jointly zero. Given the VAR(3) model, there is enough evidence to suggest that real GDP Granger-causes at least one future value of the CPI.

In this case, the test augments the VAR(3) model with an additional lag. In other words, the model is a VAR(4) model. However, gctest tests only whether the first three lags are 0.

Since R2023a

Time series are block exogenous if they do not Granger-cause any other variables in a multivariate system. Test whether the effective federal funds rate is block exogenous with respect to the real GDP, personal consumption expenditures, and inflation rates. Provide data in a timetable.

Load the US macroeconomic data set Data_USEconModel.mat. Convert the price series to returns; specify durations between sampling times relative to years.

load Data_USEconModel DataTimeTable.RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF; EffectVariables = ["CPIAUCSL" "RGDP" "PCEC"]; DTTRet = price2ret(DataTimeTable,DataVariables=EffectVariables, ... Units="years");

Test whether the federal funds rate is nonstationary by conducting an augmented Dickey-Fuller test. Specify that the alternative model has a drift term and an test.

StatTblADFTest = adftest(DataTimeTable,DataVariable="FEDFUNDS",Model="ard")

StatTblADFTest=1×8 table

h pValue stat cValue Lags Alpha Model Test

_____ ________ _______ _______ ____ _____ _______ ______

Test 1 false 0.071419 -2.7257 -2.8751 0 0.05 {'ARD'} {'T1'}

The test decision h = 0 indicates that the null hypothesis that the series has a unit root should not be rejected, at 0.05 significance level.

To stabilize the federal funds rate series, apply the first difference to it.

DTTRet.DFEDFUNDS = diff(DataTimeTable.FEDFUNDS);

Assume a 4-D VAR(3) model for the four series. Assess whether the federal funds rate is block exogenous with respect to the real GDP, personal consumption expenditures, and inflation rates. Supply the data in the timetable DTTRet, and conduct an -based Wald test.

StatTblGCTEST = gctest(DTTRet,CauseVariables="DFEDFUNDS", ... EffectVariables=EffectVariables,NumLags=2,Test="f")

StatTblGCTEST=1×6 table

h pValue stat cValue alpha test

_____ __________ ______ ______ _____ ____

Test 1 true 3.9311e-10 10.465 2.1426 0.05 "f"

The test decision hgc = 1 indicates that the null hypothesis that the federal funds rate is block exogenous should be rejected. This result suggests that the federal funds rate Granger-causes at least one of the other variables in the system.

To determine which variables the federal funds rate Granger-causes, you can run a leave-one-out test. For more details, see gctest function of the VAR model object varm.

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Granger, C. W. J. "Investigating Causal Relations by Econometric Models and Cross-Spectral Methods." Econometrica. Vol. 37, 1969, pp. 424–459.

[2] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[3] Dolado, J. J., and H. Lütkepohl. "Making Wald Tests Work for Cointegrated VAR Systems." Econometric Reviews. Vol. 15, 1996, pp. 369–386.

[4] Lütkepohl, Helmut. New Introduction to Multiple Time Series Analysis. New York, NY: Springer-Verlag, 2007.

[5] Toda, H. Y., and T. Yamamoto. "Statistical Inferences in Vector Autoregressions with Possibly Integrated Processes." Journal of Econometrics. Vol. 66, 1995, pp. 225–250.