summarize

Summarize Markov-switching dynamic regression model estimation results

Since R2021b

Description

summarize( displays a summary of the

Markov-switching dynamic regression model Mdl)Mdl.

If

Mdlis an estimated model returned byestimate, thensummarizedisplays estimation results to the MATLAB® Command Window. The display includes:A model description

Estimated transition probabilities

Fit statistics, which include the effective sample size, number of estimated submodel parameters and constraints, loglikelihood, and information criteria (AIC and BIC)

A table of submodel estimates and inferences, which includes coefficient estimates with standard errors, t-statistics, and p-values.

If

Mdlis an unestimated Markov-switching model returned bymsVAR,summarizeprints the standard object display (the same display thatmsVARprints during model creation).

results = summarize(___)

If

Mdlis an estimated Markov-switching model,resultsis a table containing the submodel estimates and inferences.If

Mdlis an unestimated model,resultsis anmsVARobject that is equal toMdl.

Examples

Consider a two-state Markov-switching dynamic regression model of the postwar US real GDP growth rate, as estimated in [1].

Create Partially Specified Model for Estimation

Create a Markov-switching dynamic regression model for the naive estimator by specifying a two-state discrete-time Markov chain with an unknown transition matrix and AR(0) (constant only) submodels for both regimes. Label the regimes.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(0,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Mdl is a partially specified msVAR object. NaN-valued elements of the Switch and SubModels properties indicate estimable parameters.

Create Fully Specified Model Containing Initial Values

The estimation procedure requires initial values for all estimable parameters. Create a fully specified Markov-switching dynamic regression model that has the same structure as Mdl, but set all estimable parameters to initial values. This example uses arbitrary initial values.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1); mdl02 = arima('Constant',-1,'Variance',1); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Mdl0 is a fully specified msVAR object.

Load and Preprocess Data

Load the US GDP data set.

load Data_GDPData contains quarterly measurements of the US real GDP in the period 1947:Q1–2005:Q2. The estimation period in [1] is 1947:Q2–2004:Q2. For more details on the data set, enter Description at the command line.

Transform the data to an annualized rate series:

Convert the data to a quarterly rate within the estimation period.

Annualize the quarterly rates.

qrate = diff(Data(2:230))./Data(2:229); % Quarterly rate arate = 100*((1 + qrate).^4 - 1); % Annualized rate

Estimate Model

Fit the model Mdl to the annualized rate series arate. Specify Mdl0 as the model containing the initial estimable parameter values.

EstMdl = estimate(Mdl,Mdl0,arate);

EstMdl is an estimated (fully specified) Markov-switching dynamic regression model. EstMdl.Switch is an estimated discrete-time Markov chain model (dtmc object), and EstMdl.Submodels is a vector of estimated univariate VAR(0) models (varm objects).

Display the estimated state-specific dynamic models.

EstMdlExp = EstMdl.Submodels(1)

EstMdlExp =

varm with properties:

Description: "1-Dimensional VAR(0) Model"

SeriesNames: "Y1"

NumSeries: 1

P: 0

Constant: 4.90146

AR: {}

Trend: 0

Beta: [1×0 matrix]

Covariance: 12.087

EstMdlRec = EstMdl.Submodels(2)

EstMdlRec =

varm with properties:

Description: "1-Dimensional VAR(0) Model"

SeriesNames: "Y1"

NumSeries: 1

P: 0

Constant: 0.0084884

AR: {}

Trend: 0

Beta: [1×0 matrix]

Covariance: 12.6876

Display the estimated state transition matrix.

EstP = EstMdl.Switch.P

EstP = 2×2

0.9088 0.0912

0.2303 0.7697

Display an estimation summary containing parameter estimates and inferences.

summarize(EstMdl)

Description

1-Dimensional msVAR Model with 2 Submodels

Switch

Estimated Transition Matrix:

0.909 0.091

0.230 0.770

Fit

Effective Sample Size: 228

Number of Estimated Parameters: 2

Number of Constrained Parameters: 0

LogLikelihood: -639.496

AIC: 1282.992

BIC: 1289.851

Submodels

Estimate StandardError TStatistic PValue

_________ _____________ __________ ___________

State 1 Constant(1) 4.9015 0.23023 21.289 1.4301e-100

State 2 Constant(1) 0.0084884 0.2359 0.035983 0.9713

Create the following fully specified Markov-switching model the DGP.

State transition matrix: .

State 1: , where .

State 2: , where .

State 3:, where .

PDGP = [0.5 0.2 0.3; 0.2 0.6 0.2; 0.2 0.1 0.7];

mcDGP = dtmc(PDGP);

constant1 = [-1; -1];

constant2 = [-1; 2];

constant3 = [1; 2];

AR1 = [-0.5 0.1; 0.2 -0.75];

AR3 = [0.5 0.1; 0.2 0.75];

Sigma1 = [0.5 0; 0 1];

Sigma2 = eye(2);

Sigma3 = [1 -0.1; -0.1 2];

mdl1DGP = varm(Constant=constant1,AR={AR1},Covariance=Sigma1);

mdl2DGP = varm(Constant=constant2,Covariance=Sigma2);

mdl3DGP = varm(Constant=constant3,AR={AR3},Covariance=Sigma3);

mdlDGP = [mdl1DGP; mdl2DGP; mdl3DGP];

MdlDGP = msVAR(mcDGP,mdlDGP);Generate a random response path of length 1000 from the DGP.

rng(1) % For reproducibiliy

Y = simulate(MdlDGP,1000);Create a partially specified Markov-switching model that has the same structure as the DGP, but the transition matrix, and all submodel coefficients and innovations covariance matrices are unknown and estimable.

mc = dtmc(nan(3)); mdlar = varm(2,1); mdlc = varm(2,0); Mdl = msVAR(mc,[mdlar; mdlc; mdlar]);

Initialize the estimation procedure by fully specifying a Markov-switching model that has the same structure as Mdl, but has the following parameter values:

A randomly drawn transition matrix

Randomly drawn constant vectors for each model

AR self lags of 0.1 and cross lags of 0

The identify matrix for the innovations covariance

P0 = randi(10,3,3);

mc0 = dtmc(P0);

constant01 = randn(2,1);

constant02 = randn(2,1);

constant03 = randn(2,1);

AR0 = 0.1*eye(2);

Sigma0 = eye(2);

mdl01 = varm(Constant=constant01,AR={AR0},Covariance=Sigma0);

mdl02 = varm(Constant=constant02,Covariance=Sigma0);

mdl03 = varm(Constant=constant03,AR={AR0},Covariance=Sigma0);

submdl0 = [mdl01; mdl02; mdl03];

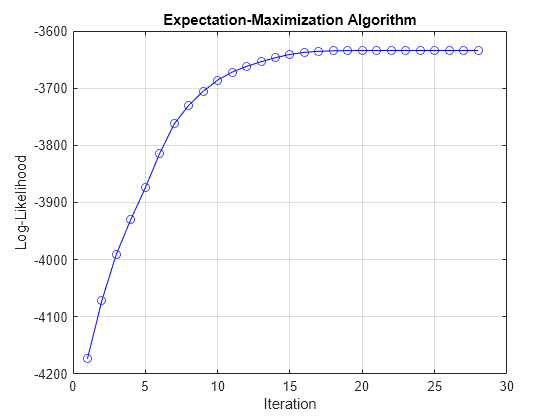

Mdl0 = msVAR(mc0,submdl0);Fit the Markov-switching model to the simulated series. Plot the loglikelihood after each iteration of the EM algorithm.

EstMdl = estimate(Mdl,Mdl0,Y,IterationPlot=true);

The plot displays the evolution of the loglikelihood with increasing iterations of the EM algorithm. The procedure terminates when one of the stopping criteria is satisfied.

Display an estimation summary of the model.

summarize(EstMdl)

Description

2-Dimensional msVAR Model with 3 Submodels

Switch

Estimated Transition Matrix:

0.501 0.245 0.254

0.204 0.549 0.247

0.188 0.102 0.710

Fit

Effective Sample Size: 999

Number of Estimated Parameters: 14

Number of Constrained Parameters: 0

LogLikelihood: -3634.005

AIC: 7296.010

BIC: 7364.704

Submodels

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 1 Constant(1) -0.98929 0.023779 -41.603 0

State 1 Constant(2) -1.0884 0.030164 -36.083 4.1957e-285

State 1 AR{1}(1,1) -0.48446 0.01547 -31.316 2.8121e-215

State 1 AR{1}(2,1) 0.1835 0.019624 9.3509 8.6868e-21

State 1 AR{1}(1,2) 0.083953 0.0070162 11.966 5.3839e-33

State 1 AR{1}(2,2) -0.72972 0.0089002 -81.989 0

State 2 Constant(1) -0.9082 0.030103 -30.17 5.9064e-200

State 2 Constant(2) 1.9514 0.030483 64.016 0

State 3 Constant(1) 1.1212 0.044427 25.237 1.5818e-140

State 3 Constant(2) 1.9561 0.0593 32.986 1.2831e-238

State 3 AR{1}(1,1) 0.48965 0.023149 21.152 2.6484e-99

State 3 AR{1}(2,1) 0.22688 0.030899 7.3427 2.0936e-13

State 3 AR{1}(1,2) 0.095847 0.012005 7.9838 1.4188e-15

State 3 AR{1}(2,2) 0.72766 0.016024 45.41 0

Display an estimation summary separately for each state.

summarize(EstMdl,1)

Description

2-Dimensional VAR Submodel, State 1

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 1 Constant(1) -0.98929 0.023779 -41.603 0

State 1 Constant(2) -1.0884 0.030164 -36.083 4.1957e-285

State 1 AR{1}(1,1) -0.48446 0.01547 -31.316 2.8121e-215

State 1 AR{1}(2,1) 0.1835 0.019624 9.3509 8.6868e-21

State 1 AR{1}(1,2) 0.083953 0.0070162 11.966 5.3839e-33

State 1 AR{1}(2,2) -0.72972 0.0089002 -81.989 0

summarize(EstMdl,2)

Description

2-Dimensional VAR Submodel, State 2

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 2 Constant(1) -0.9082 0.030103 -30.17 5.9064e-200

State 2 Constant(2) 1.9514 0.030483 64.016 0

summarize(EstMdl,3)

Description

2-Dimensional VAR Submodel, State 3

Submodel

Estimate StandardError TStatistic PValue

________ _____________ __________ ___________

State 3 Constant(1) 1.1212 0.044427 25.237 1.5818e-140

State 3 Constant(2) 1.9561 0.0593 32.986 1.2831e-238

State 3 AR{1}(1,1) 0.48965 0.023149 21.152 2.6484e-99

State 3 AR{1}(2,1) 0.22688 0.030899 7.3427 2.0936e-13

State 3 AR{1}(1,2) 0.095847 0.012005 7.9838 1.4188e-15

State 3 AR{1}(2,2) 0.72766 0.016024 45.41 0

Consider the model for the US GDP growth rate in Estimate Markov-Switching Dynamic Regression Model.

Create a Markov-switching dynamic regression model for the naive estimator.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(0,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Create a fully specified Markov-switching dynamic regression model that has the same structure as Mdl, but set all estimable parameters to initial values.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1); mdl02 = arima('Constant',-1,'Variance',1); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Load the US GDP data set. Preprocess the data.

load Data_GDP qrate = diff(Data(2:230))./Data(2:229); % Quarterly rate arate = 100*((1 + qrate).^4 - 1); % Annualized rate

Fit the model Mdl to the annualized rate series arate. Specify Mdl0 as the model containing the initial estimable parameter values.

EstMdl = estimate(Mdl,Mdl0,arate);

Return an estimation summary table.

results = summarize(EstMdl)

results=2×4 table

Estimate StandardError TStatistic PValue

_________ _____________ __________ ___________

State 1 Constant(1) 4.9015 0.23023 21.289 1.4301e-100

State 2 Constant(1) 0.0084884 0.2359 0.035983 0.9713

results is a table containing estimates and inferences for all submodel coefficients.

Identify significant coefficient estimates.

results.Properties.RowNames(results.PValue < 0.05)

ans = 1×1 cell array

{'State 1 Constant(1)'}

Input Arguments

Output Arguments

Algorithms

estimate implements

a version of Hamilton's Expectation-Maximization (EM) algorithm, as described in [3]. The standard errors, loglikelihood, and

information criteria are conditional on optimal parameter values in the estimated transition

matrix Mdl.Switch. In particular, standard errors do not account for

variation in estimated transition probabilities.

References

[2] Hamilton, J. D. "Analysis of Time Series Subject to Changes in Regime." Journal of Econometrics. Vol. 45, 1990, pp. 39–70.

[3] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[4] Hamilton, J. D. "Macroeconomic Regimes and Regime Shifts." In Handbook of Macroeconomics. (H. Uhlig and J. Taylor, eds.). Amsterdam: Elsevier, 2016.

Version History

Introduced in R2021b