estimate

Fit Markov-switching dynamic regression model to data

Syntax

Description

EstMdl = estimate(Mdl,Mdl0,Y)Mdl. estimate fits the model to the response

data Y, and initializes the estimation procedure by treating the

parameter values of the fully specified Markov-switching dynamic regression model

Mdl0 as initial values. estimate uses a

version of the expectation-maximization (EM) algorithm described by Hamilton [3].

Examples

Consider a two-state Markov-switching dynamic regression model of the postwar US real GDP growth rate, as estimated in [1].

Create Partially Specified Model for Estimation

Create a Markov-switching dynamic regression model for the naive estimator by specifying a two-state discrete-time Markov chain with an unknown transition matrix and AR(0) (constant only) submodels for both regimes. Label the regimes.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(0,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Mdl is a partially specified msVAR object. NaN-valued elements of the Switch and SubModels properties indicate estimable parameters.

Create Fully Specified Model Containing Initial Values

The estimation procedure requires initial values for all estimable parameters. Create a fully specified Markov-switching dynamic regression model that has the same structure as Mdl, but set all estimable parameters to initial values. This example uses arbitrary initial values.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1); mdl02 = arima('Constant',-1,'Variance',1); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Mdl0 is a fully specified msVAR object.

Load and Preprocess Data

Load the US GDP data set.

load Data_GDPData contains quarterly measurements of the US real GDP in the period 1947:Q1–2005:Q2. The estimation period in [1] is 1947:Q2–2004:Q2. For more details on the data set, enter Description at the command line.

Transform the data to an annualized rate series:

Convert the data to a quarterly rate within the estimation period.

Annualize the quarterly rates.

qrate = diff(Data(2:230))./Data(2:229); % Quarterly rate arate = 100*((1 + qrate).^4 - 1); % Annualized rate

Estimate Model

Fit the model Mdl to the annualized rate series arate. Specify Mdl0 as the model containing the initial estimable parameter values.

EstMdl = estimate(Mdl,Mdl0,arate);

EstMdl is an estimated (fully specified) Markov-switching dynamic regression model. EstMdl.Switch is an estimated discrete-time Markov chain model (dtmc object), and EstMdl.Submodels is a vector of estimated univariate VAR(0) models (varm objects).

Display the estimated state-specific dynamic models.

EstMdlExp = EstMdl.Submodels(1)

EstMdlExp =

varm with properties:

Description: "1-Dimensional VAR(0) Model"

SeriesNames: "Y1"

NumSeries: 1

P: 0

Constant: 4.90146

AR: {}

Trend: 0

Beta: [1×0 matrix]

Covariance: 12.087

EstMdlRec = EstMdl.Submodels(2)

EstMdlRec =

varm with properties:

Description: "1-Dimensional VAR(0) Model"

SeriesNames: "Y1"

NumSeries: 1

P: 0

Constant: 0.0084884

AR: {}

Trend: 0

Beta: [1×0 matrix]

Covariance: 12.6876

Display the estimated state transition matrix.

EstP = EstMdl.Switch.P

EstP = 2×2

0.9088 0.0912

0.2303 0.7697

Display an estimation summary containing parameter estimates and inferences.

summarize(EstMdl)

Description

1-Dimensional msVAR Model with 2 Submodels

Switch

Estimated Transition Matrix:

0.909 0.091

0.230 0.770

Fit

Effective Sample Size: 228

Number of Estimated Parameters: 2

Number of Constrained Parameters: 0

LogLikelihood: -639.496

AIC: 1282.992

BIC: 1289.851

Submodels

Estimate StandardError TStatistic PValue

_________ _____________ __________ ___________

State 1 Constant(1) 4.9015 0.23023 21.289 1.4301e-100

State 2 Constant(1) 0.0084884 0.2359 0.035983 0.9713

Consider the model and data in Estimate Markov-Switching Dynamic Regression Model.

Create the partially specified model for estimation.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(0,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Create the fully specified model containing initial parameter values for the estimation procedure.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1); mdl02 = arima('Constant',-1,'Variance',1); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Load and preprocess the data.

load Data_GDP

qrate = diff(Data(2:230))./Data(2:229);

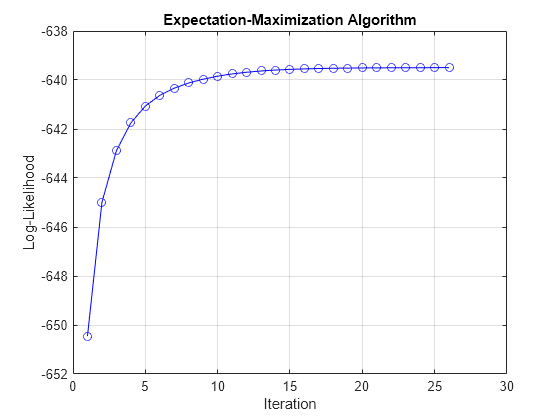

arate = 100*((1 + qrate).^4 - 1); Fit the model to the data. Plot the loglikelihood versus the iteration step when the estimation procedure terminates.

EstMdl = estimate(Mdl,Mdl0,arate,'IterationPlot',true);

Assess estimation accuracy using simulated data from a known data-generating process (DGP). This example uses arbitrary parameter values.

Create Model for DGP

Create a fully specified, two-state discrete-time Markov chain model for the switching mechanism.

P = [0.7 0.3; 0.1 0.9]; mc = dtmc(P);

For each state, create a fully specified AR(1) model for the response process.

% Constants C1 = 5; C2 = -2; % Autoregression coefficients AR1 = 0.4; AR2 = 0.2; % Variances V1 = 4; V2 = 2; % AR Submodels dgp1 = arima('Constant',C1,'AR',AR1,'Variance',V1); dgp2 = arima('Constant',C2,'AR',AR2,'Variance',V2);

Create a fully specified Markov-switching dynamic regression model for the DGP.

DGP = msVAR(mc,[dgp1,dgp2]);

Simulate Response Paths from DGP

Generate 10 random response paths of length 1000 from the DGP.

rng(1); % For reproducibility N = 10; n = 1000; Data = simulate(DGP,n,'Numpaths',N);

Data is a 1000-by-10 matrix of simulated responses.

Create Model for Estimation

Create a partially specified Markov-switching dynamic regression model that has the same structure as the data-generating process, but specify an unknown transition matrix and unknown submodel coefficients.

PEst = NaN(2); mcEst = dtmc(PEst); mdl = arima(1,0,0); Mdl = msVAR(mcEst,[mdl; mdl]);

Create Model Containing Initial Values

Create a fully specified Markov-switching dynamic regression model that has the same structure as Mdl, but set all estimable parameters to initial values.

P0 = 0.5*ones(2); mc0 = dtmc(P0); mdl01 = arima('Constant',1,'AR',0.5,'Variance',2); mdl02 = arima('Constant',-1,'AR',0.5,'Variance',1); Mdl0 = msVAR(mc0,[mdl01,mdl02]);

Estimate Models

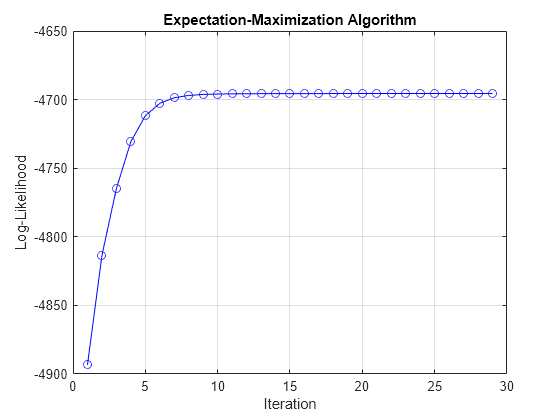

Fit the model to each simulated path. For each path, plot the loglikelihood at each iteration of the EM algorithm.

c1 = zeros(N,1); c2 = zeros(N,1); v1 = zeros(N,1); v2 = zeros(N,1); ar1 = zeros(N,1); ar2 = zeros(N,1); PStack = zeros(2,2,N); figure hold on for i = 1:N EstModel = estimate(Mdl,Mdl0,Data(:,i),'IterationPlot',true); c1(i) = EstModel.Submodels(1).Constant; c2(i) = EstModel.Submodels(2).Constant; v1(i) = EstModel.Submodels(1).Covariance; v2(i) = EstModel.Submodels(2).Covariance; ar1(i) = EstModel.Submodels(1).AR{1}; ar2(i) = EstModel.Submodels(2).AR{1}; PStack(:,:,i) = EstModel.Switch.P; end hold off

Assess Accuracy

Compute the Monte Carlo mean of each estimated parameter.

c1Mean = mean(c1); c2Mean = mean(c2); v1Mean = mean(v1); v2Mean = mean(v2); ar1Mean = mean(ar1); ar2Mean = mean(ar2); PMean = mean(PStack,3);

Compare population parameters to the corresponding Monte Carlo estimates.

DGPvsEstimate = [...

C1 c1Mean

C2 c2Mean

V1 v1Mean

V2 v2Mean

AR1 ar1Mean

AR2 ar2Mean]DGPvsEstimate = 6×2

5.0000 5.0260

-2.0000 -1.9615

4.0000 3.9710

2.0000 1.9903

0.4000 0.4061

0.2000 0.2017

P

P = 2×2

0.7000 0.3000

0.1000 0.9000

PEstimate = PMean

PEstimate = 2×2

0.7065 0.2935

0.1023 0.8977

Consider the data in Estimate Markov-Switching Dynamic Regression Model, but assume that the period of interest is 1960:Q1–2004:Q2. Also, consider adding an autoregressive term to each submodel.

Create a partially specified Markov-switching dynamic regression model for estimation. Specify AR(1) submodels.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(1,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Because the submodels are AR(1), each requires one presample observation to initialize its dynamic component for estimation.

Create the model containing initial parameter values for the estimation procedure.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1,'AR',0.001); mdl02 = arima('Constant',-1,'Variance',1,'AR',0.001); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Load the data. Transform the entire set to an annualized rate series.

load Data_GDP

qrate = diff(Data)./Data(1:(end - 1));

arate = 100*((1 + qrate).^4 - 1);Identify the presample and estimation sample periods using the dates associated with the annualized rate series. Because the transformation applies the first difference, you must drop the first observation date from the original sample.

dates = datetime(dates(2:end),'ConvertFrom','datenum',... 'Format','yyyy:QQQ','Locale','en_US'); estPrd = datetime(["1960:Q2" "2004:Q2"],'InputFormat','yyyy:QQQ',... 'Format','yyyy:QQQ','Locale','en_US'); idxEst = isbetween(dates,estPrd(1),estPrd(2)); idxPre = dates < estPrd(1); % The presample is the previous quarter.

Fit the model to the estimation sample data. Specify the presample observation and plot the loglikelihood at each iteration when the estimation procedure terminates.

EstMdl = estimate(Mdl,Mdl0,arate(idxEst),'Y0',arate(idxPre),... 'IterationPlot',true);

Consider the model and data in Estimate Markov-Switching Dynamic Regression Model.

Create the partially specified model for estimation.

P = NaN(2); mc = dtmc(P,'StateNames',["Expansion" "Recession"]); mdl = arima(0,0,0); Mdl = msVAR(mc,[mdl; mdl]);

Create the fully specified model containing initial parameter values for the estimation procedure.

P0 = 0.5*ones(2); mc0 = dtmc(P0,'StateNames',Mdl.StateNames); mdl01 = arima('Constant',1,'Variance',1); mdl02 = arima('Constant',-1,'Variance',1); Mdl0 = msVAR(mc0,[mdl01; mdl02]);

Load and preprocess the data.

load Data_GDP

qrate = diff(Data(2:230))./Data(2:229);

arate = 100*((1 + qrate).^4 - 1); Fit the model to the data. Return the expected smoothed state probabilities and loglikelihood when the algorithm terminates.

[EstMdl,SS,logL] = estimate(Mdl,Mdl0,arate);

SS is a 228-by-2 matrix of expected smoothed state probabilities; rows correspond to periods in the estimation sample, and columns correspond to the regimes. logL is the final loglikelihood.

Display the expected smoothed state probabilities for the last period in the estimation sample, and display the final loglikelihood.

SS(end,:)

ans = 1×2

0.8985 0.1015

logL

logL = -639.4962

Fit simulated data to a Markov-switching dynamic regression model with VARX submodels. Specify equality constraints for estimation. This example uses arbitrary parameter values.

Create Model for DGP

Create a fully specified, three-state discrete-time Markov chain model for the switching mechanism.

P = [0.8 0.1 0.1; 0.2 0.6 0.2; 0 0.1 0.9]; mc = dtmc(P);

For each state, create a fully specified VARX(1) model for the response process. Specify the same model constant and lag 1 AR coefficient matrix for all submodels. For each model, specify a different 2-by-1 regression coefficient for the one exogenous variable.

% Constants C = [1;-1]; % Autoregression coefficients AR = {[0.6 0.1; 0.4 0.2]}; % Regression coefficients Beta1 = [0.2;-0.4]; Beta2 = [0.6;-1.0]; Beta3 = [0.9;-1.3]; % VAR Submodels dgp = varm('Constant',C,'AR',AR,'Covariance',5*eye(2)); dgp1 = dgp; dgp1.Beta = Beta1; dgp2 = dgp; dgp2.Beta = Beta2; dgp3 = dgp; dgp3.Beta = Beta3;

Create a fully specified Markov-switching dynamic regression model for the DGP.

DGP = msVAR(mc,[dgp1; dgp2; dgp3]);

Simulate Data from DGP

Simulate data for the exogenous series by generating 1000 observations from the Gaussian distribution with mean 0 and variance 100.

rng(1); % For reproducibility

X = 10*randn(1000,1);Generate a random response path of length 1000 from the DGP. Specify the simulated exogenous data for the submodel regression components.

Data = simulate(DGP,1000,'X',X);Data is a 1000-by-1 vector of simulated responses.

Create Model for Estimation

Create a partially specified Markov-switching dynamic regression model that has the same structure as the data-generating process, but specify an unknown transition matrix and unknown regression coefficients. Specify the true values of the constants and AR coefficient matrices.

PEst = NaN(3); mcEst = dtmc(PEst); mdl = varm(2,1); mdl.Constant = C; mdl.AR = AR; mdl.Beta = NaN(2,1); Mdl = msVAR(mcEst,[mdl; mdl; mdl]);

Because the values of the constants and AR coefficient matrices are specified in Mdl, estimate treats them as equality constraints for estimation.

Create Model Containing Initial Values

Create a fully specified Markov-switching dynamic regression model that has the same structure as Mdl, but set all estimable parameters to initial values and set parameters with equality constraints to their values specified in Mdl.

P0 = (1/3)*ones(3); mc0 = dtmc(P0); mdl0 = varm('Constant',C,'AR',AR,'Covariance',eye(2)); mdl01 = mdl0; mdl01.Beta = [0.1;-0.1]; mdl02 = mdl0; mdl02.Beta = [0.5;-0.5]; mdl03 = mdl0; mdl03.Beta = [1;-1]; Mdl0 = msVAR(mc0,[mdl01; mdl02; mdl03]);

Estimate Model

Fit the model to the simulated data. Specify the exogenous data for the regression component. Plot the loglikelihood at each iteration of the EM algorithm.

figure EstMdl = estimate(Mdl,Mdl0,Data,'X',X,'IterationPlot',true);

Assess Accuracy

Compare the estimated regression coefficient vectors and transition matrix to their true values.

Beta1

Beta1 = 2×1

0.2000

-0.4000

Beta1Estimate = EstMdl.Submodels(1).Beta

Beta1Estimate = 2×1

0.1596

-0.4040

Beta2

Beta2 = 2×1

0.6000

-1.0000

Beta2Estimate = EstMdl.Submodels(2).Beta

Beta2Estimate = 2×1

0.5888

-0.9771

Beta3

Beta3 = 2×1

0.9000

-1.3000

Beta3Estimate = EstMdl.Submodels(3).Beta

Beta3Estimate = 2×1

0.8987

-1.2991

P

P = 3×3

0.8000 0.1000 0.1000

0.2000 0.6000 0.2000

0 0.1000 0.9000

PEstimate = EstMdl.Switch.P

PEstimate = 3×3

0.7787 0.0856 0.1357

0.1366 0.6906 0.1727

0.0086 0.0787 0.9127

Input Arguments

Name-Value Arguments

Output Arguments

Tips

In [4], Hamilton cautions: "Although a researcher might be tempted to use the most general specification possible, with all the parameters changing across a large number of regimes...in practice this is usually asking more than the data can deliver." Hamilton recommends model parsimony and selective estimation, to "limit the focus to a few of the most important parameters that are likely to change."

Data-generating processes with low variances can lead to difficulties in state inference and subsequent parameter estimation. In such cases, consider scaling the data. The variance scales quadratically.

Algorithms

estimateimplements a version of the EM algorithm described in [2], [3], and [4]. Given an initial estimate of model parametersMdl0,estimateiterates the following process until convergence:Expectation step —

estimateappliessmoothto the data to obtain inferences of latent state probabilities at each time step and an estimate of the overall data loglikelihood.Maximization step —

estimateuses the expected smoothed probabilities from the expectation step to weight the data before updating parameter estimates in each submodel.

Likelihood surfaces for the mixture densities of switching models can contain local maxima and singularities [2]. If so, the largest local maximum with a nonzero model variance is considered the maximum likelihood estimate (MLE). If

Mdl0is in the neighborhood of the MLE,estimatetypically converges to it, but this convergence is not guaranteed.estimatehandles two types of constraints:Constraints on submodel parameters, which the

estimateobject function of thevarmobject enforces at each maximization stepConstraints on transition probabilities, which

estimateenforces by projecting a maximal estimate of the transition matrix onto the constrained parameter space after each iteration

Constraints on submodel innovations variances and covariances are unsupported.

estimatecomputes innovations covariances after estimation, regardless of their values.

References

[2] Hamilton, J. D. "Analysis of Time Series Subject to Changes in Regime." Journal of Econometrics. Vol. 45, 1990, pp. 39–70.

[3] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[4] Hamilton, J. D. "Macroeconomic Regimes and Regime Shifts." In Handbook of Macroeconomics. (H. Uhlig and J. Taylor, eds.). Amsterdam: Elsevier, 2016.

[5] Kole, E. "Regime Switching Models: An Example for a Stock Market Index." Rotterdam, NL: Econometric Institute, Erasmus School of Economics, 2010.

Version History

Introduced in R2019b