chargeChart

Syntax

Description

chargeChart( creates a chart of

portfolio market risk capital charge values. Each charge value can be broken down into

contributions from the default risk capital charge (DRC), residual risk add-on capital

charge (RRAO), and sensitivity-based market risk capital charge (SBM). For more

information on market risk capital charge, see Charge.frtbsaObj)

chargeChart(

creates a chart of portfolio market risk capital charge values using optional name-value

arguments.frtbsaObj,Name=Value)

Examples

Use an frtbsa object and the chargeChart function to plot the total capital market risk charge for each portfolio. FRTB-SA (Standardized Approach for Fundamental Review of Trading Book) is a Basel Committee on Banking Supervision framework for calculating market capital risk requirements. This framework is based on a set of standardized risk factors.

Create frtbsa Object

Use bank format to display numeric data using two decimal places.

format bankDefine the ISDA® FRTB-SA CRIF file.

FRTBSACRIF = "FRTBSA_CRIF.csv";Define the DRC reference date.

DrcRefCOBDate = datetime(2023,9,21);

Use frtbsa to create the FRTB-SA object.

myFRTBSA = frtbsa(FRTBSACRIF,DRCValuationDate=DrcRefCOBDate)

myFRTBSA =

frtbsa with properties:

CRIF: [159×18 table]

NumPortfolios: 2.00

PortfolioIDs: [2×1 string]

Portfolios: [2×1 frtbsa.Portfolio]

Regulation: "Basel"

DomesticCurrency: "USD"

DRCValuationDate: 21-Sep-2023

NumDaysYear: 365.00

Generate Charge Charts

To plot the total portfolio market risk capital charge values, use chargeChart with the Style name-value argument set to "final".

chargeChart(myFRTBSA,Style="final")

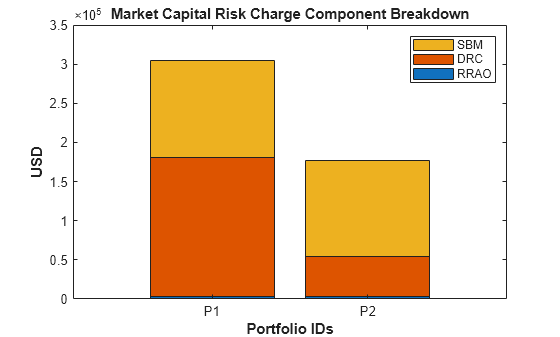

To plot the breakdown of the market risk capital charge components, use chargeChart with the Style name-value argument set to "component".

chargeChart(myFRTBSA,Style="component")

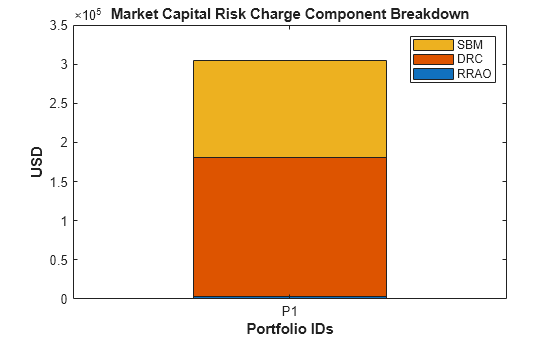

To plot the breakdown of the market risk capital charge components for a subset of portfolios using the IDs name-value argument, use chargeChart with the Style name-value argument set to "component".

chargeChart(myFRTBSA,Style="component",IDs = "P1")

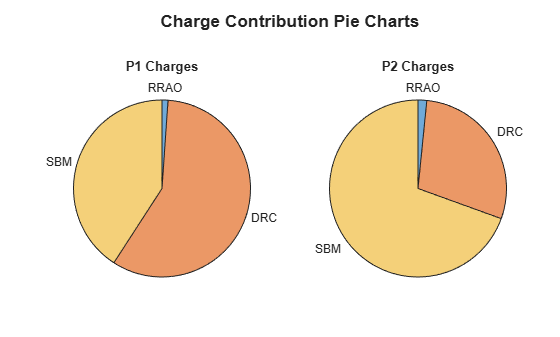

Specify "pie" for Style to create a breakdown of pie charts by its components: DRC, RRAO, and SBM.

ax = gca;

chargeChart(myFRTBSA,Style="pie",Parent=ax)

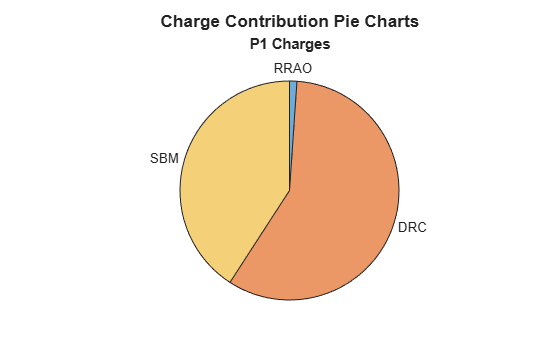

Plot a subset of portfolios using the IDs name-value argument.

figure chargeChart(myFRTBSA,Style="pie",IDs="P1")

Input Arguments

Name-Value Arguments

Output Arguments

References

[1] Bank for International Settlements. "MAR21 — Standardised Approach: Sensitivities-Based Method." March 2020. https://www.bis.org/basel_framework/chapter/MAR/21.htm.

[2] Bank for International Settlements. "MAR22 — Standardised Approach: Default Risk Capital Requirement." March 2020. https://www.bis.org/basel_framework/chapter/MAR/22.htm.

[3] Bank for International Settlements. "MAR23 — Standardised Approach: Residual Risk Add-On." March 2020. https://www.bis.org/basel_framework/chapter/MAR/23.htm.

[4] Bank for International Settlements. "CRE42 — Securitisation: External-Ratings-Based Approach (SEC-ERBA)." January 2023. https://www.bis.org/basel_framework/chapter/CRE/42.htm.

[5] Bank for International Settlements. "Basel Committee on Banking Supervision: Minimum Capital Requirements for Market Risk." January 2019. https://www.bis.org/bcbs/publ/d457.pdf.