risk.validation.areaUnderCurveTest

Syntax

Description

hAUCTest = risk.validation.areaUnderCurveTest(BaselineScore,BaselineBinaryResponse,TargetScore,TargetBinaryResponse)1 if the test rejects the

null hypothesis at the 95% confidence level, or 0

otherwise.

hAUCTest = risk.validation.areaUnderCurveTest(BaselineScore,BaselineBinaryResponse,TargetScore,TargetBinaryResponse,Name=Value)

Examples

Perform an AUC test on customer probability of default (PD) data to determine if the AUC for a baseline portfolio is smaller than the AUC for a target portfolio. The PDRatingGradeData file contains a table with variables PD, RatingGrade, ObservationYear, and Default. These variables, respectively, contain data for customer probability of default (PD), rating grade, observation year, and whether the customer defaulted.

Load the data.

data = readtable("PDRatingGradeData.csv")data=500×4 table

PD RatingGrade ObservationYear Default

________ ___________ _______________ _______

0.40736 9 2020 0

0.4529 10 2020 0

0.063493 2 2020 0

0.45669 10 2020 1

0.31618 7 2020 0

0.04877 1 2020 0

0.13925 3 2020 0

0.27344 6 2020 0

0.47875 10 2020 0

0.48244 10 2020 0

0.078807 2 2020 0

0.4853 10 2020 0

0.47858 10 2020 0

0.24269 5 2020 0

0.40014 9 2020 0

0.070943 2 2020 0

⋮

Create two logical vectors indicating the observations that belong to the baseline portfolio and the observations that belong to the target portfolio.

baselineElem = data.ObservationYear==2023; targetElem = data.ObservationYear==2024;

Create vectors from the rating grade and binary response data for the baseline and target portfolios.

BaselineScore = data.RatingGrade(baselineElem); TargetScore = data.RatingGrade(targetElem); BaselineBinaryResponse = data.Default(baselineElem); TargetBinaryResponse = data.Default(targetElem);

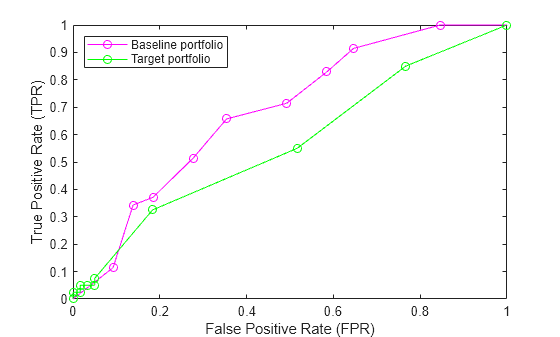

Calculate the x- and y-coordinates of the receiver operating characteristic (ROC) curve for each portfolio by using the perfcurve function. Plot the ROC curves together.

[XB,YB] = perfcurve(BaselineBinaryResponse,BaselineScore,1); [XT,YT] = perfcurve(TargetBinaryResponse,TargetScore,1); plot(XB,YB,"o-m") hold on plot(XT,YT,"o-g") xlabel("False Positive Rate (FPR)") ylabel("True Positive Rate (TPR)") legend("Baseline portfolio","Target portfolio",Location="northwest")

The plot shows that the curve for the target portfolio is mostly below the curve for the baseline portfolio.

Use the areaUnderCurveTest function with the fully qualified namespace risk.validation to perform an area under curve test on the baseline and target portfolio data.

risk.validation.areaUnderCurveTest(BaselineScore,BaselineBinaryResponse, ...

TargetScore,TargetBinaryResponse)ans = logical

1

The output shows that enough evidence exists to reject the null hypothesis that the AUC for the baseline portfolio is smaller than the AUC for the target portfolio. This result is consistent with the ROC curve for the target portfolio being under the ROC curve for the baseline portfolio.

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] European Central Bank, “Instructions for reporting the validation results of internal models.” February, 2019. https://www.bankingsupervision.europa.eu/activities/internal_models/shared/pdf/instructions_validation_reporting_credit_risk.en.pdf.

Version History

Introduced in R2026a