{kind=link}

{kind=link}

Feeds

已发布

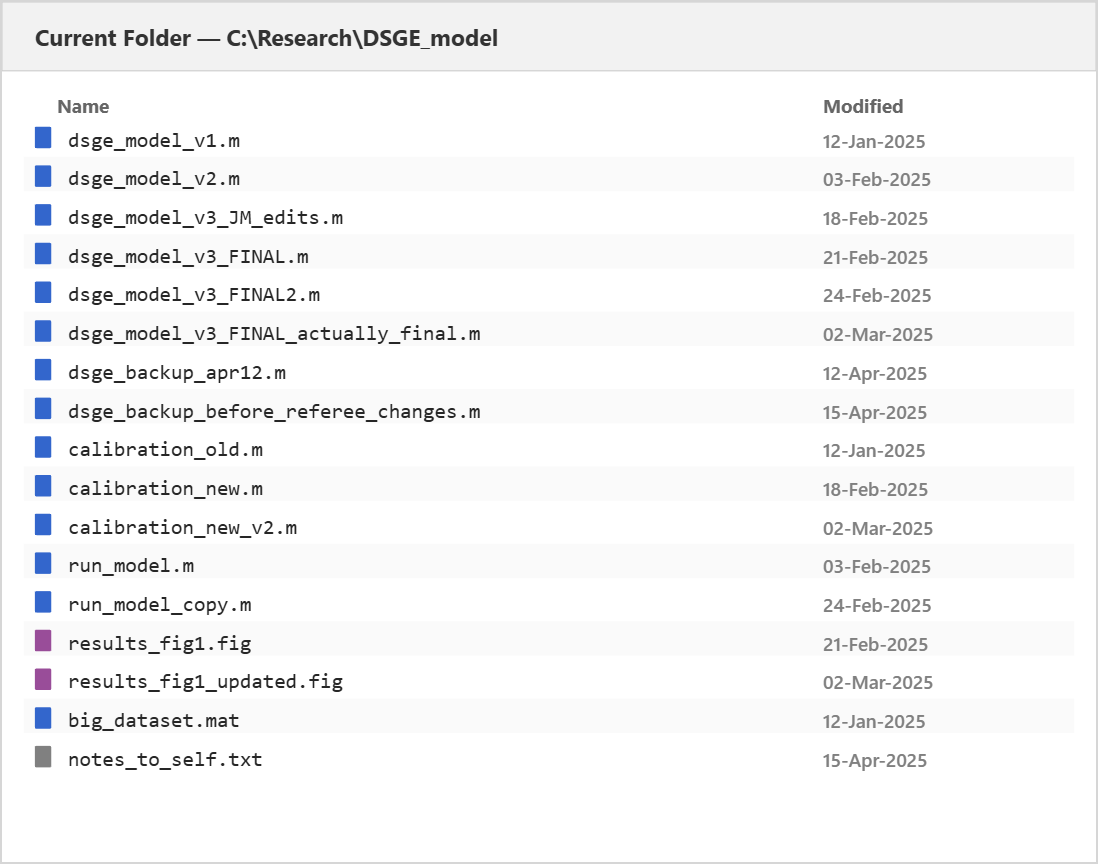

Version Control for Economic Models

A Practical Guide to Git in MATLAB The Problem You Already Have You know the folder. Somewhere on your machine there...

16 days 前

已发布

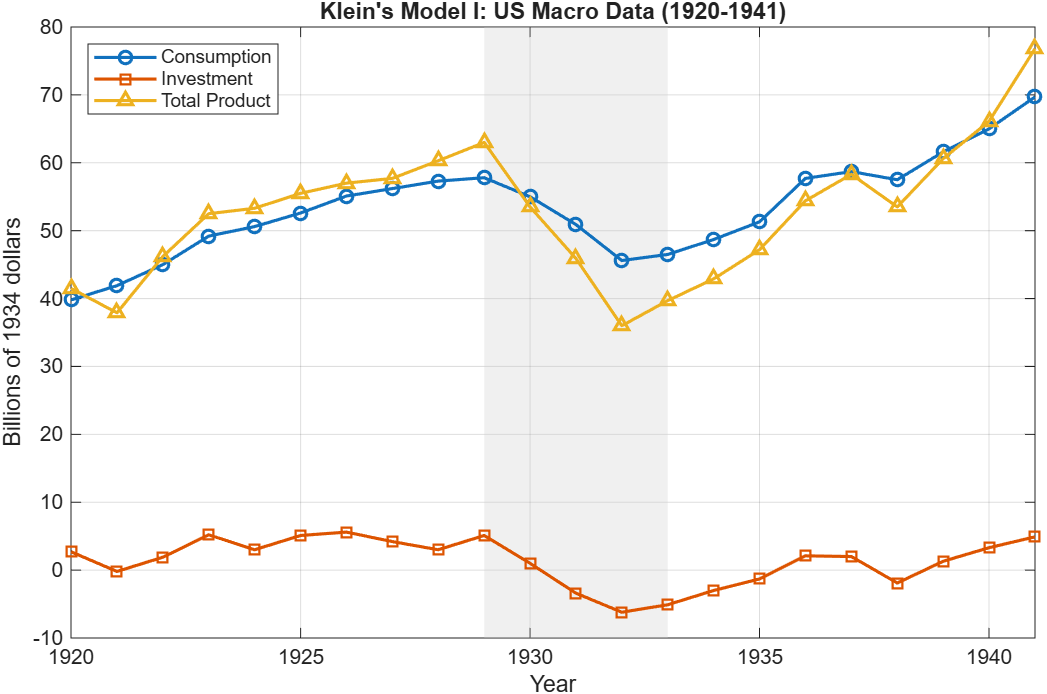

From EViews to MATLAB in One Line: Reading Workfiles Directly

Economists often keep years of work in EViews workfiles: macroeconomic series, model estimates, and curated panel data. The...

1 month 前

已发布

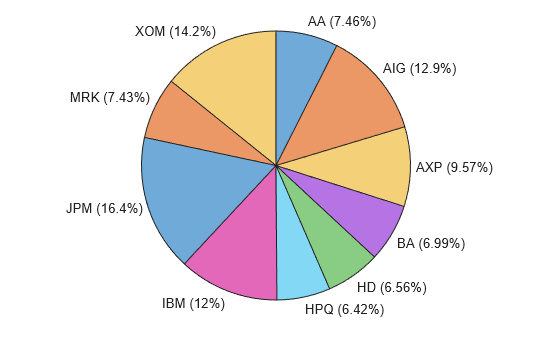

Portfolio Optimization with Target Factor Exposures

A practical MATLAB walkthrough comparing tracking error and exact exposure approaches. When you build a factor-based...

2 months 前

已发布

Prototype Time-Series Forecasts with Deep Learning—Without Writing Code

Expert Contributor: Dr. Yuchen Dong Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the...

2 months 前

已发布

Run Dynare at Scale on Databricks with Interactive MATLAB

Expert Contributor: Dr. Eduard Benet Cerdà Edu is a Senior Application Engineer at MathWorks advising customers in the...

3 months 前

已发布

What’s New in MATLAB R2026a for Economists

R2026a covers a lot of ground for economists—Bayesian state-space estimation, macro-scale forecasting, climate and physical...

3 months 前

已发布

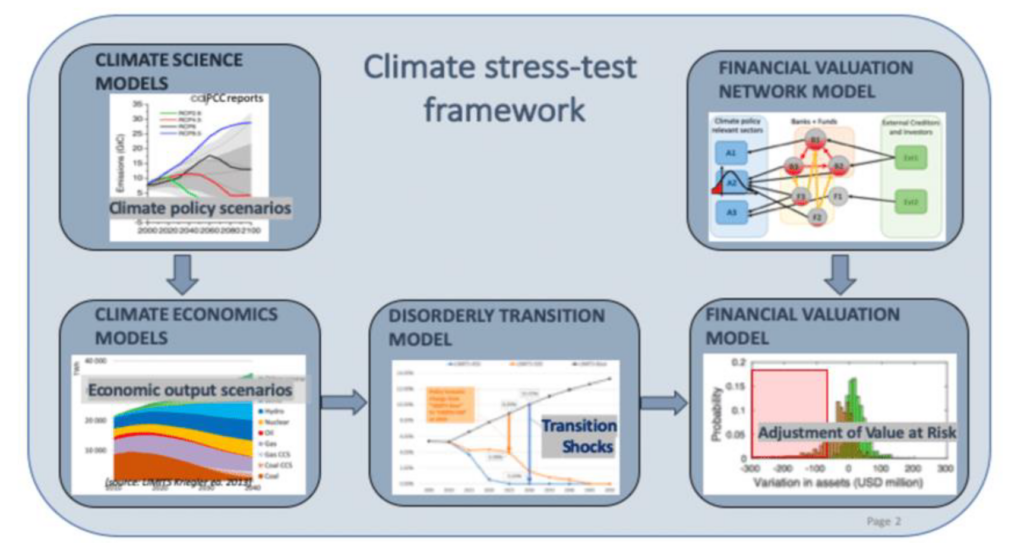

CRISK: A Market‑Based Framework for Quantifying Climate Risk in Banking

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations...

4 months 前

已发布

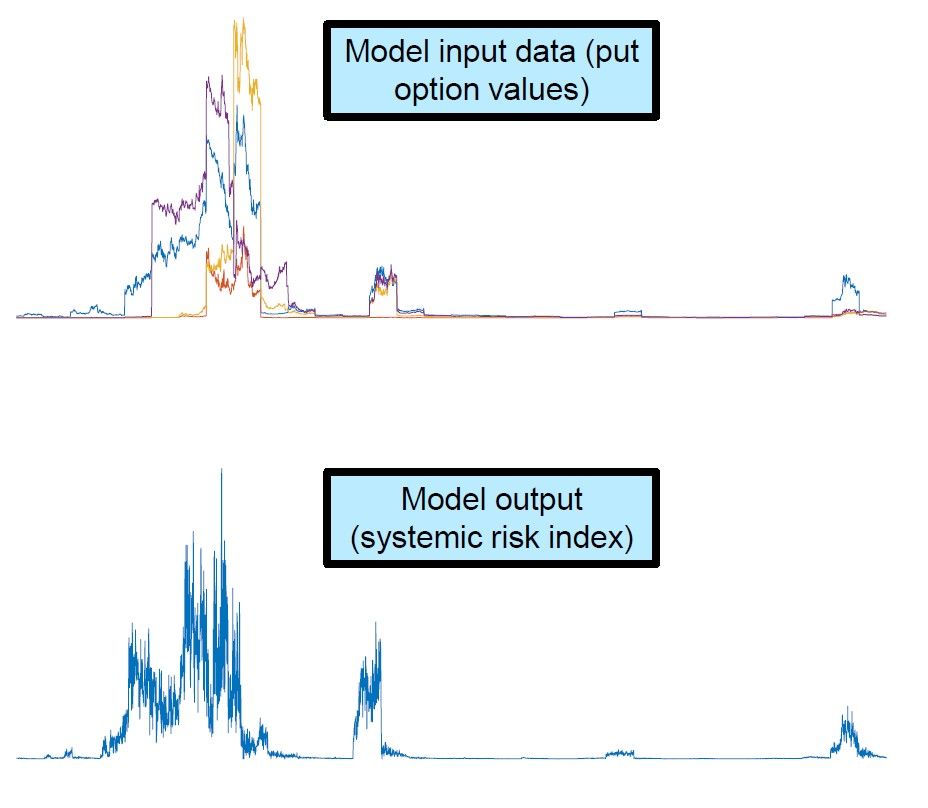

Systemic Risk Modeling with MATLAB: Tools and Techniques for Central Banks

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to...

4 months 前

已发布

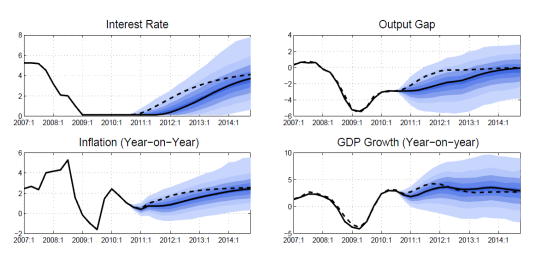

Refining Macroeconomic Forecasting with MATLAB Techniques

Nonlinear confidence bands help you quantify forecast uncertainty in DSGE models, but they can be slow to compute. At the...

4 months 前

已发布

Upgrading MATLAB: What You Gain and How to Get There

Every MATLAB release opens the door to new capabilities, better performance, and tighter integration with the platforms...

5 months 前

已发布

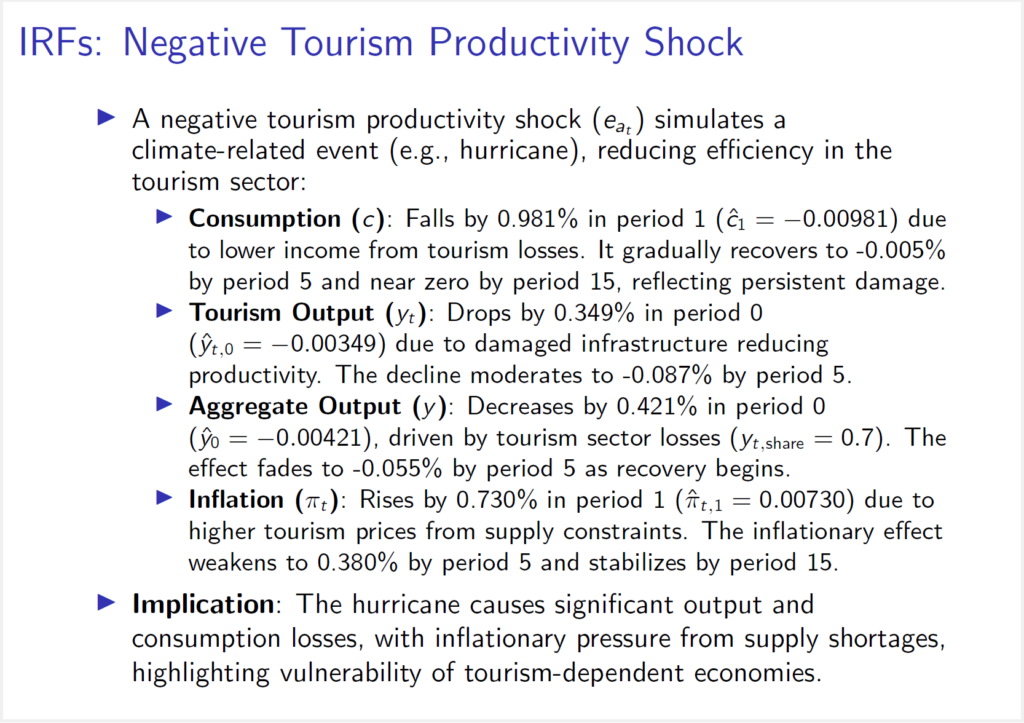

Central Bank of The Bahamas Uses MATLAB and Dynare to Model Climate and Tourism Shocks

“It [MATLAB] was used in Dynare in order to promote the accuracy and the ease of generating this model.”— Allan Wright,...

5 months 前

已发布

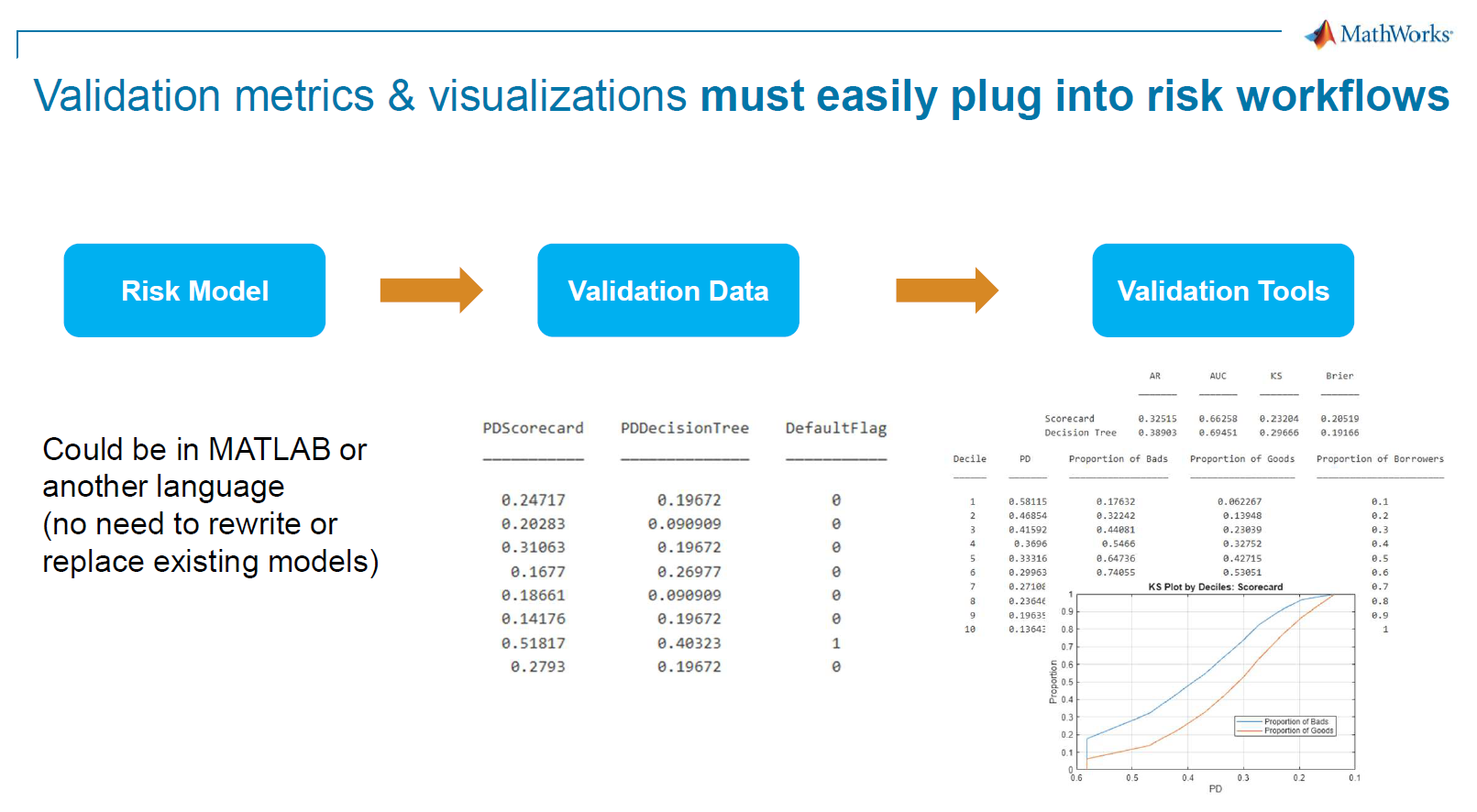

Credit and Market Risk Management: From Risk Modeling to Regulatory Compliance

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial...

7 months 前

已发布

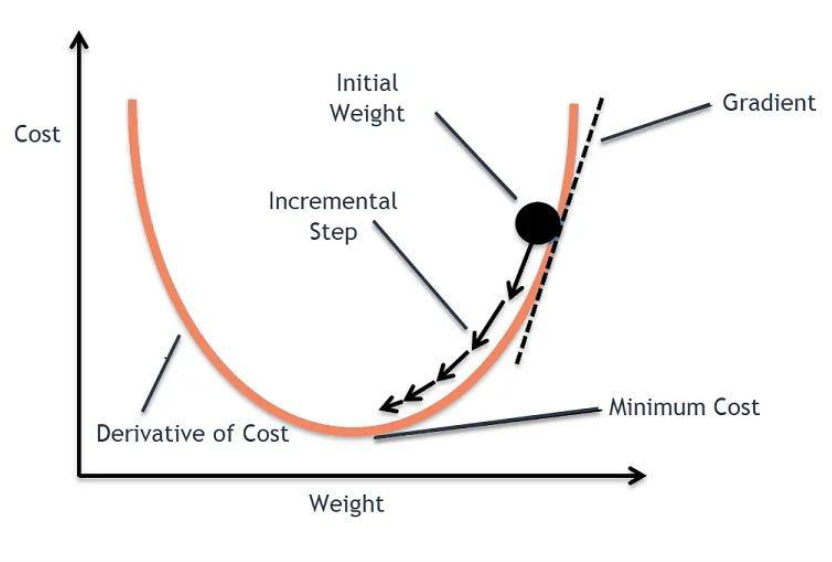

Speeding Up Dynare Models: Practical Paths to Performance Gains

Dynamic Stochastic General Equilibrium (DSGE) models are essential tools for policy analysis and forecasting, but...

7 months 前

已发布

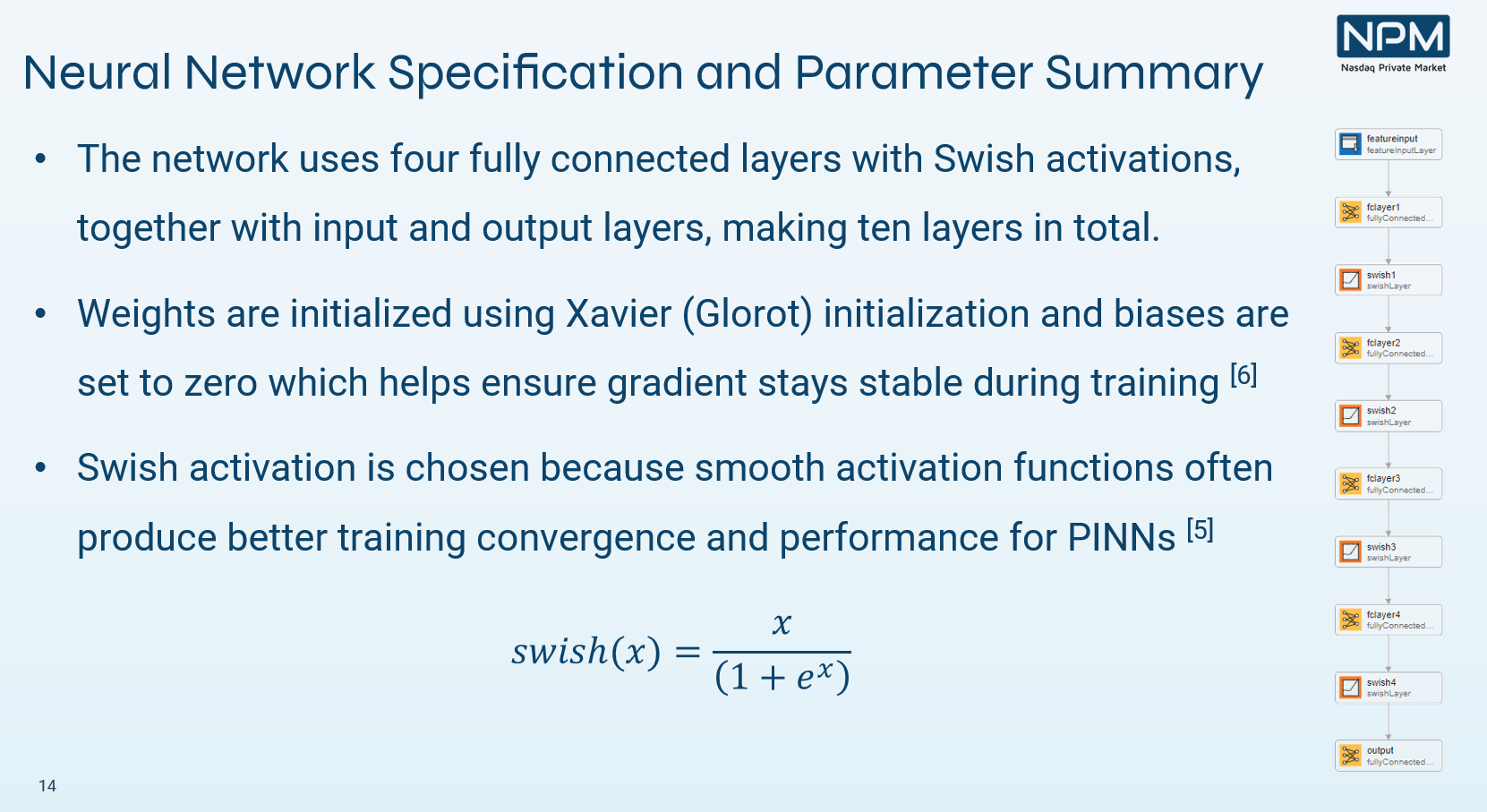

Pricing Special Purpose Vehicles with Physics‑Informed Neural Networks at Nasdaq Private Market

Summary Nasdaq Private Market (NPM) used MATLAB® to prototype and scale physics‑informed neural networks (PINNs) that price...

8 months 前

已发布

Highlights from MathWorks Finance Conference 2025

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore...

9 months 前

已发布

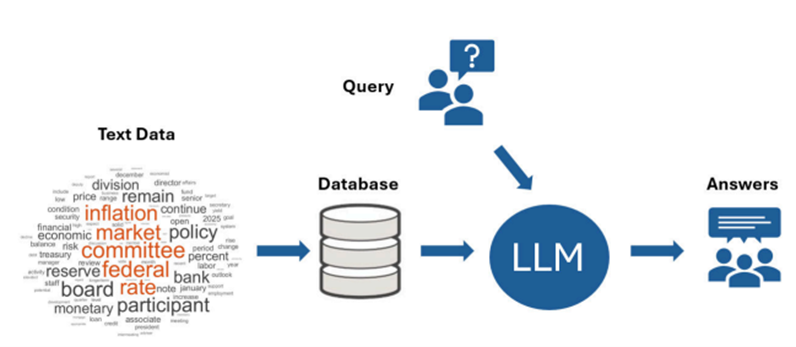

Build a RAG Pipeline in MATLAB: From Document Ingestion to LLM-Driven Insights

The following post is from Yuchen Dong, Senior Finance Application Engineer at MathWorks. The example featured in the...

9 months 前

已发布

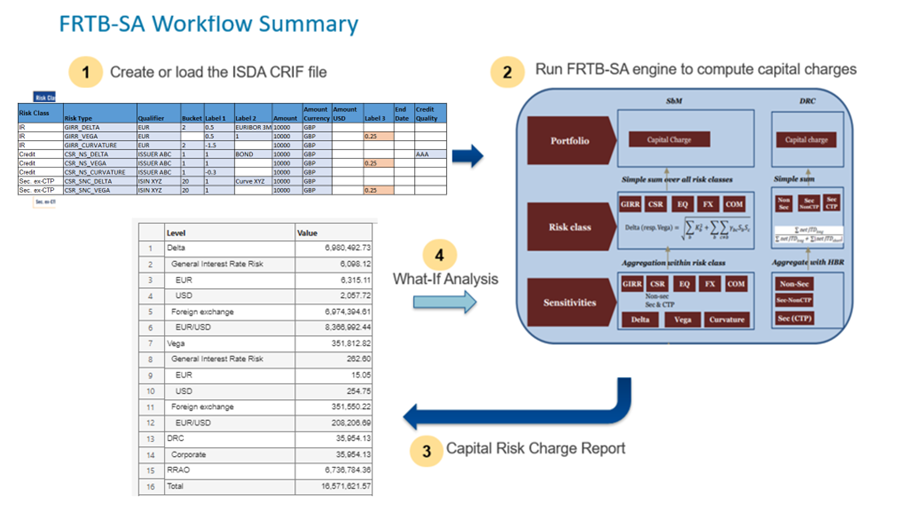

Navigating FRTB: Standardized vs Internal Models – and the Role of Scriptable Risk Engines

The Fundamental Review of the Trading Book (FRTB) is reshaping how banks measure and manage market risk. Beyond replacing...

10 months 前

已发布

The FRED Connector in Datafeed Toolbox

If you work with macro, markets, or policy analysis, chances are you touch FRED®—the Federal Reserve Economic Data service....

10 months 前

已发布

Analyzing the Financial Risks of Wildfires

We recently hosted a technical webinar focused on analyzing the financial risks of wildfires. Akshay Paul and Yuchen Dong...

10 months 前

已发布

Building a Neural Network for Time Series Forecasting – Low-Code Workflow

The following post is from Yuchen Dong, Senior Financial Application Engineer at MathWorks. Financial institutions forecast...

11 months 前

已发布

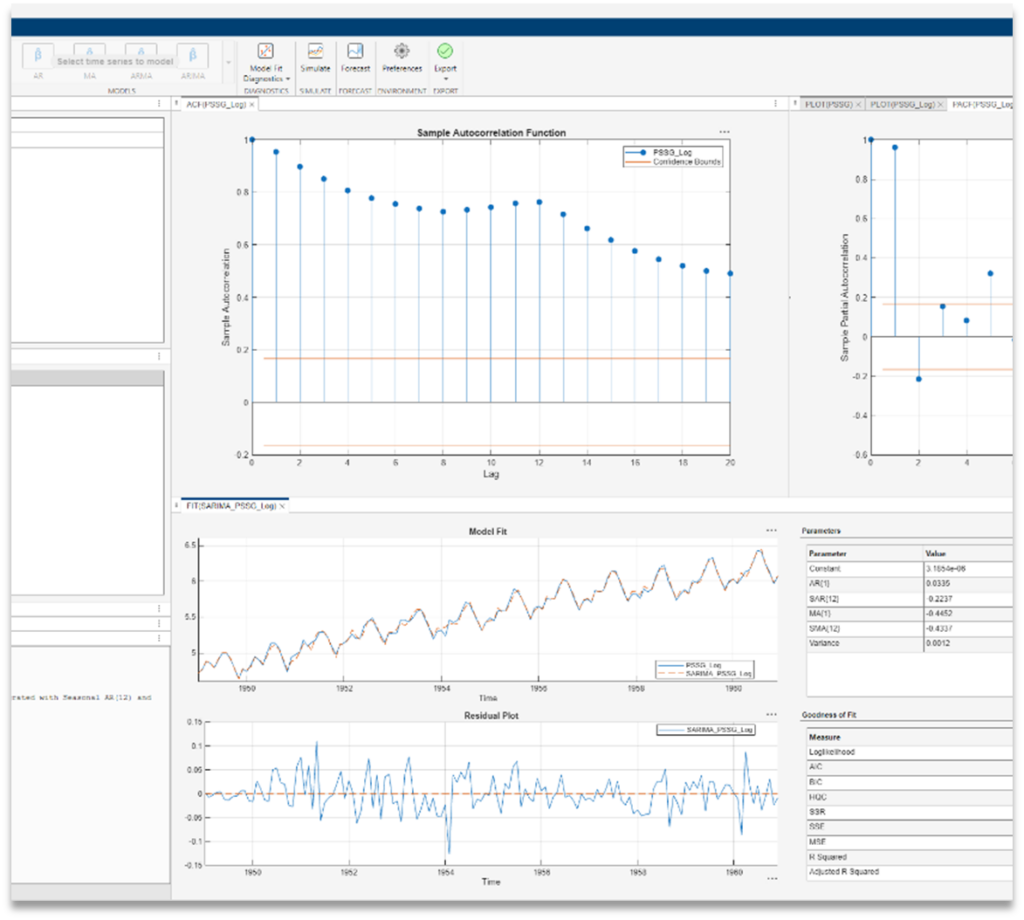

GDP Nowcasting with MATLAB

What is GDP Nowcasting? Imagine trying to drive a car while only getting speed updates every three months. That’s kind of...

1 year 前

已发布

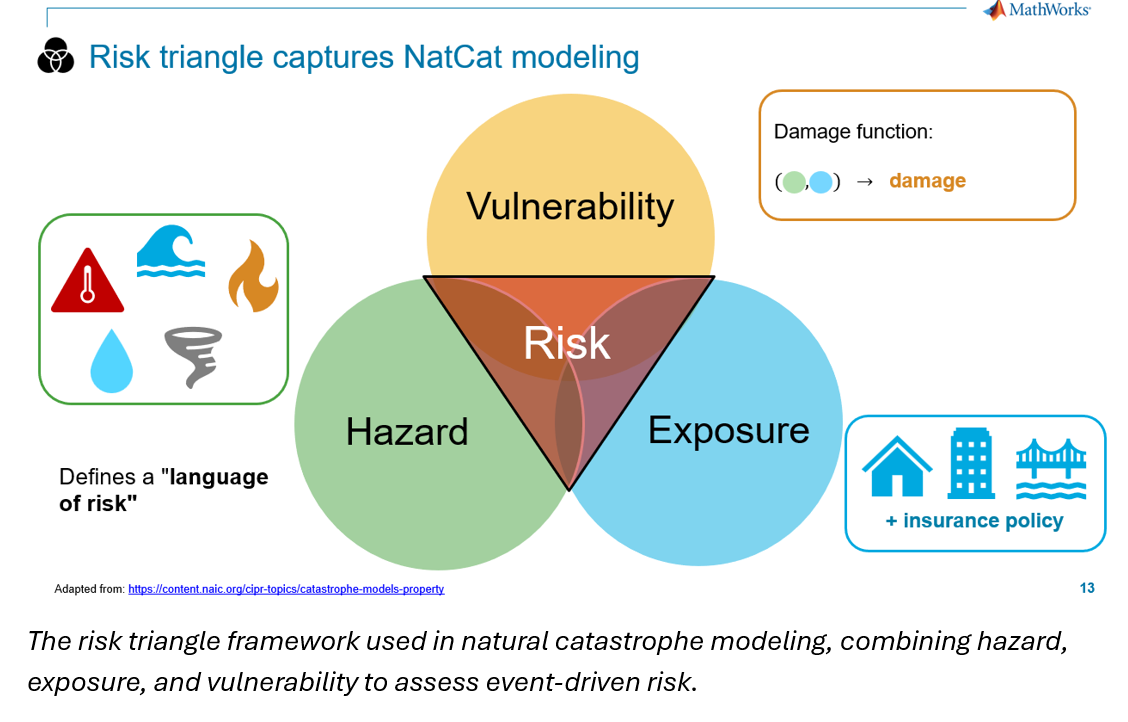

Modeling Physical Climate Risk Across Financial Portfolios

Financial institutions are reassessing long-term risk models as physical climate events like hurricanes, floods, and...

1 year 前

已发布

Accelerating Asset Management with ModelOps: From Model Building to Monitoring

Asset management quants face complex data environments, tight timelines, and the constant pressure to translate models into...

1 year 前

已发布

2nd Biennial Macroeconometric Caribbean Conference

MathWorks was recently invited to the 2nd Biennial Macroeconometric Caribbean Conference in Nassau, Bahamas, organized by...

1 year 前

已发布

The Economic Effects of Tariff Changes

The following post is from Yuchen Dong, Senior Financial Application Engineer. The code presented in this blog can be found...

1 year 前

已发布

Modeling Exchange Rate Volatility

The following post is from William Mueller, Software Developer on the Econometrics Toolbox Team. Forecasting currency...

1 year 前

已发布

Assessing Climate Impacts on Credit Risk

We recently hosted a technical webinar focused on climate transition risk, specifically assessing climate impacts on credit...

1 year 前

已发布

Simplifying Econometric Modeling with MATLAB

Econometric modeling is essential for analyzing economic data, making forecasts, and informing policy decisions, however,...

1 year 前

已发布

Celebrating 30 Years of Dynare and Its Global Impact with MATLAB

As we celebrate the 30th anniversary of Dynare, we at MathWorks would like to take a moment to reflect on its influence on...

1 year 前

已发布

Custom Portfolio Optimization: Balancing Objectives, Constraints, and Efficiency

The following blog was written by Marshall Alphonso Principal Engineer and Sara Galante, Senior Finance Application...

1 year 前