Alpha Generation Using Refinitiv News Sentiment and MATLAB

With the explosion of market data volumes and venues, quantitative trading firms face increasing data management complexities in their quest for alpha. The issues that they have to address include data gathering and preparation, model development, back-testing and calibration, integration with existing systems as well as reporting and visualization.

Join us for a webinar focused on addressing these challenges with Thomson Reuters and MathWorks. Together they help firms improve trading efficiency with integrated data management and modeling capabilities to handle the massive increases in trading volumes, venues, data sources, and depth of data with scalable and manageable tools.

This webinar features a joint use-case of MATLAB fed by Thomson Reuters News Sentiment Data. You will learn how to:

- Access and rapidly analyze daily, intraday and real-time data

- Develop models and prototype trading applications quickly and accurately

- Back-test and calibrate your trading models and strategies

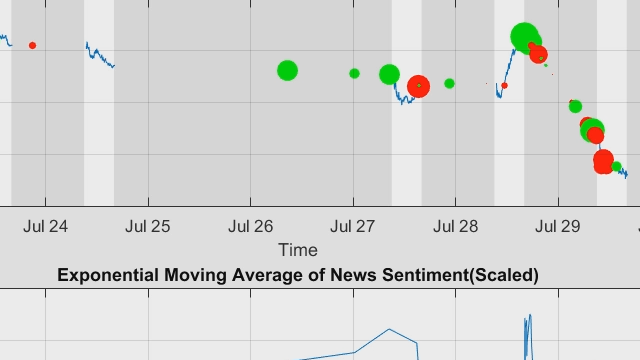

- Build promising alpha signals using News Sentiment and textual data

- Speed up your algorithms with GPUs and parallel computing

Presenters:

Stuart Kozola, Product Manager, Finance, MathWorks

Aleksander Sobczyk, Quantitative Research, Thomson Reuters

Recorded: 14 Nov 2012

Featured Product