Sanlam Multi-Manager International Develops Dashboard for Quantitative Risk Analysis

“MATLAB enabled us to concentrate on our core competencies as investment professionals and deploy a quantitative risk management and portfolio optimization dashboard that has added value from day one across our team.”

Challenge

Solution

Results

- Calculation time reduced from minutes to seconds

- Quantitative analysis tools widely deployed

- Development time shortened by months

Sanlam Multi-Manager International (SMMI) is focused on optimizing returns for its clients by identifying, selecting, and combining the best asset managers. These managers, in turn, select the underlying investment assets. Decisions on portfolio construction, manager selection, and tactical asset allocation are based on quantitative analysis and qualitative evaluations.

SMMI used MATLAB® to implement an integrated workflow for modeling risk inputs, generating optimized portfolios, calculating risk metrics, and supporting qualitative insights with quantitative metrics.

“With MATLAB we integrated three previously siloed activities,” says Mathew John, investment analyst at SMMI. Jason Liddle, risk manager at SMMI, adds, “This led to a greater understanding within the investment team about the risk exposures of our portfolios. That shared understanding contributed to a significant improvement in performance in challenging market conditions.”

Challenge

The analysts wanted to replace their spreadsheet-based solution with an application that accelerated analysis, simplified data management, and integrated risk input modeling, portfolio optimization, and data visualization.

Solution

SMMI analysts used MATLAB to build and deploy an investment risk dashboard and the underlying risk modeling and optimization components.

Working in MATLAB, the team modeled risk inputs, including volatility, correlation, and covariance, and stored them in an SQL database easily accessible under referenced job names.

Using MATLAB, Financial Toolbox™, and Optimization Toolbox™ they developed algorithms that generate optimized portfolios on the efficient frontier using the Black-Litterman framework. Black-Litterman prior and posterior returns are calculated based on the stored risk inputs and market views of the investment strategist.

To calculate risk metrics, the team used a Component Object Model (COM) interface to access a Sungard APT risk engine from their MATLAB application.

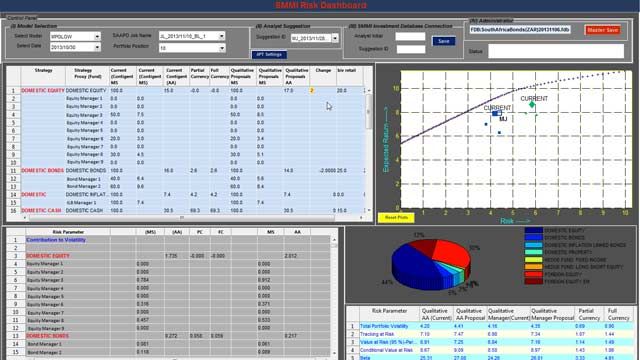

Working with OPTI-NUM Solutions, the MathWorks distributor in South Africa, the SMMI analysts used MATLAB to create a graphical interface that enables them to visualize proposed portfolio weightings and compare them against the efficient frontier and against current and past portfolios.

The team created a standalone Windows executable using MATLAB Compiler™. This version of the application, which can be used without installing MATLAB, is employed by analysts throughout SMMI, including the Chief Investment Officer.

Results

Calculation time reduced from minutes to seconds. “It took up to five minutes to open the large, complex spreadsheets we used before, and another 20 seconds to recalculate after we made changes,” says Liddle. “With MATLAB we get the results almost instantaneously. Plus, we can save the results of our analysis to a database, which is much easier to access and manage than sets of spreadsheets.”

Quantitative analysis tools widely deployed. “After we deployed the quantitative risk dashboard created with MATLAB and MATLAB Compiler, our analysts were much better prepared to have productive, qualitative debates,” notes John. “MATLAB Compiler enabled us to scale the solution we had developed and make it available to our entire investment team.”

Development time shortened by months. “If we had chosen C++ or VBA instead of MATLAB, it probably would have taken us four times longer,” says Liddle. “MATLAB makes it easy to test new ideas using built-in portfolio optimization functions and quickly turn an initial prototype into a production application.”