ecmnmle

Mean and covariance of incomplete multivariate normal data

Syntax

Description

ecmnmle( with no output arguments,

this mode displays the convergence of the ECM algorithm in a plot by estimating

objective function values for each iteration of the ECM algorithm until termination. Data)

[

estimates the mean and covariance of a data set (Mean,Covariance] = ecmnmle(Data)Data). If the

data set has missing values, this routine implements the ECM algorithm of Meng and

Rubin [2] with enhancements by Sexton and Swensen [3]. ECM stands for a conditional

maximization form of the EM algorithm of Dempster, Laird, and Rubin [4].

[

adds an optional arguments for Mean,Covariance] = ecmnmle(___,InitMethod,MaxIterations,Tolerance,Mean0,Covar0)InitMethod,

MaxIterations,

Tolerance,Mean0, and

Covar0.

Examples

This example shows how to compute the mean and covariance of incomplete multivariate normal data for five years of daily total return data for 12 computer technology stocks, with six hardware and six software companies

load ecmtechdemo.matThe time period for this data extends from April 19, 2000 to April 18, 2005. The sixth stock in Assets is Google (GOOG), which started trading on August 19, 2004. So, all returns before August 20, 2004 are missing and represented as NaNs. Also, Amazon (AMZN) had a few days with missing values scattered throughout the past five years.

ecmnmle(Data)

ans = 12×1

0.0008

0.0008

-0.0005

0.0002

0.0011

0.0038

-0.0003

-0.0000

-0.0003

-0.0000

-0.0003

0.0004

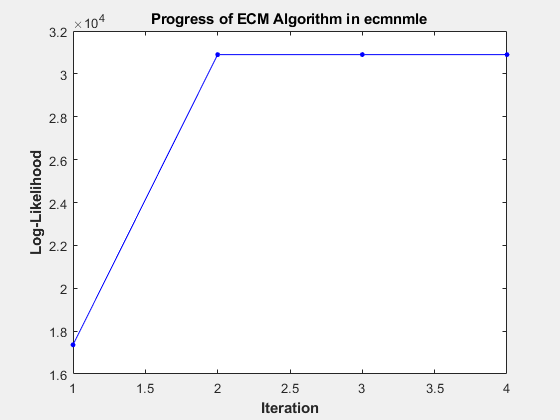

This plot shows that, even with almost 87% of the Google data being NaN values, the algorithm converges after only four iterations.

[Mean,Covariance] = ecmnmle(Data)

Mean = 12×1

0.0008

0.0008

-0.0005

0.0002

0.0011

0.0038

-0.0003

-0.0000

-0.0003

-0.0000

-0.0003

0.0004

Covariance = 12×12

0.0012 0.0005 0.0006 0.0005 0.0005 0.0003 0.0005 0.0003 0.0006 0.0003 0.0005 0.0006

0.0005 0.0024 0.0007 0.0006 0.0010 0.0004 0.0005 0.0003 0.0006 0.0004 0.0006 0.0012

0.0006 0.0007 0.0013 0.0007 0.0007 0.0003 0.0006 0.0004 0.0008 0.0005 0.0008 0.0008

0.0005 0.0006 0.0007 0.0009 0.0006 0.0002 0.0005 0.0003 0.0007 0.0004 0.0005 0.0007

0.0005 0.0010 0.0007 0.0006 0.0016 0.0006 0.0005 0.0003 0.0006 0.0004 0.0007 0.0011

0.0003 0.0004 0.0003 0.0002 0.0006 0.0022 0.0001 0.0002 0.0002 0.0001 0.0003 0.0016

0.0005 0.0005 0.0006 0.0005 0.0005 0.0001 0.0009 0.0003 0.0005 0.0004 0.0005 0.0006

0.0003 0.0003 0.0004 0.0003 0.0003 0.0002 0.0003 0.0005 0.0004 0.0003 0.0004 0.0004

0.0006 0.0006 0.0008 0.0007 0.0006 0.0002 0.0005 0.0004 0.0011 0.0005 0.0007 0.0007

0.0003 0.0004 0.0005 0.0004 0.0004 0.0001 0.0004 0.0003 0.0005 0.0006 0.0004 0.0005

0.0005 0.0006 0.0008 0.0005 0.0007 0.0003 0.0005 0.0004 0.0007 0.0004 0.0013 0.0007

0.0006 0.0012 0.0008 0.0007 0.0011 0.0016 0.0006 0.0004 0.0007 0.0005 0.0007 0.0020

Input Arguments

Output Arguments

Algorithms

References

[1] Little, Roderick J. A. and Donald B. Rubin. Statistical Analysis with Missing Data. 2nd Edition. John Wiley & Sons, Inc., 2002.

[2] Meng, Xiao-Li and Donald B. Rubin. “Maximum Likelihood Estimation via the ECM Algorithm.” Biometrika. Vol. 80, No. 2, 1993, pp. 267–278.

[3] Sexton, Joe and Anders Rygh Swensen. “ECM Algorithms that Converge at the Rate of EM.” Biometrika. Vol. 87, No. 3, 2000, pp. 651–662.

[4] Dempster, A. P., N. M. Laird, and Donald B. Rubin. “Maximum Likelihood from Incomplete Data via the EM Algorithm.” Journal of the Royal Statistical Society. Series B, Vol. 39, No. 1, 1977, pp. 1–37.

Version History

Introduced before R2006a