使用布林森模型分析业绩归因

此示例演示了如何准备数据,创建 brinsonAttribution 对象,然后分析与类别(行业)权重和收益相关的业绩归因。在此示例中,您会使用到 categoryAttribution、categoryReturns、categoryWeights、totalAttribution 和 summary 函数进行分析。此外,您还可以使用 categoryReturnsChart、categoryWeightsChart 和 attributionsChart 为结果生成绘图。

准备数据

将股票价格数据加载到表格中。

T = readtable('dowPortfolio.xlsx');

MonthIdx = [1;20;39;62;81;103;125;145;168;188;210;231;251];

MonthlyPrices = T(MonthIdx,3:end);使用 tick2ret 计算月收益。

MonthlyReturns = tick2ret(MonthlyPrices.Variables)'; [NumAssets,NumPeriods] = size(MonthlyReturns);

使用 categorical 定义资产类别(行业)。

Category = categorical(["Materials";"Financials";"Financials"; ... "Industrials";"Financials";"Industrials";"Materials"; ... "Communication Services";"Industrials";"Consumer Discretionary"; ... "Consumer Discretionary";"Industrials";"Information Technology"; ... "Information Technology";"Information Technology";"Health Care"; ... "Financials";"Consumer Staples";"Consumer Discretionary"; ... "Industrials";"Consumer Staples";"Health Care"; ... "Information Technology";"Health Care";"Consumer Staples"; ... "Communication Services";"Industrials";"Communication Services"; ... "Consumer Staples";"Energy"]); Category = repmat(Category,1,NumPeriods);

定义基准与投资组合权重

按季度为每只股票资产定义基准权重和投资组合权重。

BenchmarkWeight = 1./length(MonthlyReturns).*ones(NumAssets, NumPeriods); PortfolioWeightQ1 = [0;0;0.022;0.033;0;0.044;0.022;0.011;0.065;0.033; ... 0.055;0.072;0;0.04;0;0.05;0.08;0.042;0.03;0.043;0.055;0.036;0.111; ... 0.036;0;0.03;0;0.05;0;0.04]*ones(1,3); PortfolioWeightQ2 = [0;0;0.022;0.033;0;0.044;0.022;0.011;0.049;0.033; ... 0.055;0.074;0;0.04;0;0.05;0.08;0.042;0.03;0.02;0.055;0.036;0.148; ... 0.036;0;0.03;0;0.05;0;0.04]*ones(1,3); PortfolioWeightQ3 = [0;0;0.022;0.033;0;0.042;0.022;0.01;0.049;0.033; ... 0.05;0.07;0;0.04;0;0.05;0.08;0.042;0.03;0.02;0.055;0.036;0.16; ... 0.036;0;0.03;0;0.05;0;0.04]*ones(1,3); PortfolioWeightQ4 = [0;0;0.022;0.033;0;0.042;0.02;0.01;0.039;0.033; ... 0.05;0.07;0;0.04;0;0.05;0.08;0.042;0.03;0.02;0.055;0.036;0.198; ... 0.036;0;0.03;0;0.03;0;0.034]*ones(1,3); PortfolioWeight = [PortfolioWeightQ1 PortfolioWeightQ2 ... PortfolioWeightQ3 PortfolioWeightQ4]; Period = (1:NumPeriods).*ones(NumAssets,1); Name = repmat(string(MonthlyPrices.Properties.VariableNames(:)),1,NumPeriods);

创建 AssetTable 输入。

使用 table 创建一个 AssetTable 输入以在创建 brinsonAttribution 对象时使用。

AssetTable = table(Period(:), Name(:), ... MonthlyReturns(:), Category(:), ... PortfolioWeight(:), BenchmarkWeight(:), ... VariableNames=["Period", "Name","Return","Category",... "PortfolioWeight","BenchmarkWeight"])

AssetTable=360×6 table

Period Name Return Category PortfolioWeight BenchmarkWeight

______ ______ ___________ ______________________ _______________ _______________

1 "AA" 0.053621 Materials 0 0.033333

1 "AIG" -0.05964 Financials 0 0.033333

1 "AXP" -0.00019406 Financials 0.022 0.033333

1 "BA" -0.030162 Industrials 0.033 0.033333

1 "C" -0.055015 Financials 0 0.033333

1 "CAT" 0.17956 Industrials 0.044 0.033333

1 "DD" -0.090708 Materials 0.022 0.033333

1 "DIS" 0.037221 Communication Services 0.011 0.033333

1 "GE" -0.07381 Industrials 0.065 0.033333

1 "GM" 0.27273 Consumer Discretionary 0.033 0.033333

1 "HD" -0.016838 Consumer Discretionary 0.055 0.033333

1 "HON" 0.025457 Industrials 0.072 0.033333

1 "HPQ" 0.083598 Information Technology 0 0.033333

1 "IBM" -0.009235 Information Technology 0.04 0.033333

1 "INTC" -0.1685 Information Technology 0 0.033333

1 "JNJ" -0.066351 Health Care 0.05 0.033333

⋮

创建 brinsonAttribution 对象

使用 brinsonAttribution 创建一个 brinsonAttribution 对象。

BrinsonPAobj = brinsonAttribution(AssetTable)

BrinsonPAobj =

brinsonAttribution with properties:

NumAssets: 30

NumPortfolioAssets: 22

NumBenchmarkAssets: 30

NumPeriods: 12

NumCategories: 9

AssetName: [30×1 string]

AssetReturn: [30×12 double]

AssetCategory: [30×12 categorical]

PortfolioAssetWeight: [30×12 double]

BenchmarkAssetWeight: [30×12 double]

PortfolioCategoryReturn: [9×12 double]

BenchmarkCategoryReturn: [9×12 double]

PortfolioCategoryWeight: [9×12 double]

BenchmarkCategoryWeight: [9×12 double]

PortfolioReturn: 0.2234

BenchmarkReturn: 0.2046

ActiveReturn: 0.0188

计算类别权重

使用 brinsonAttribution 对象和 categoryWeights 计算投资组合和基准的平均及周期性类别权重,以及相应的主动权重。

[AverageCategoryWeights,PeriodicCategoryWeights] = categoryWeights(BrinsonPAobj)

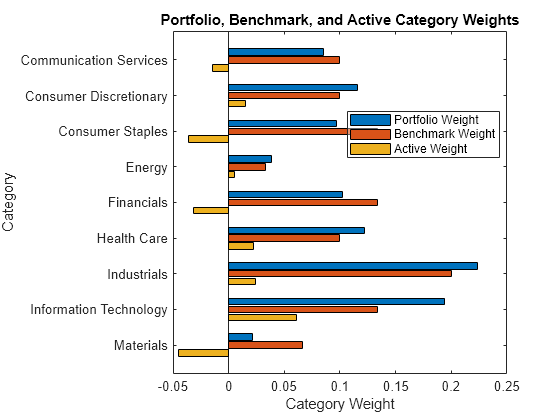

AverageCategoryWeights=9×4 table

Category AveragePortfolioWeight AverageBenchmarkWeight AverageActiveWeight

______________________ ______________________ ______________________ ___________________

Communication Services 0.0855 0.1 -0.0145

Consumer Discretionary 0.1155 0.1 0.0155

Consumer Staples 0.097 0.13333 -0.036333

Energy 0.0385 0.033333 0.0051667

Financials 0.102 0.13333 -0.031333

Health Care 0.122 0.1 0.022

Industrials 0.22375 0.2 0.02375

Information Technology 0.19425 0.13333 0.060917

Materials 0.0215 0.066667 -0.045167

PeriodicCategoryWeights=108×5 table

Period Category PortfolioWeight BenchmarkWeight ActiveWeight

______ ______________________ _______________ _______________ ____________

1 Communication Services 0.091 0.1 -0.009

1 Consumer Discretionary 0.118 0.1 0.018

1 Consumer Staples 0.097 0.13333 -0.036333

1 Energy 0.04 0.033333 0.0066667

1 Financials 0.102 0.13333 -0.031333

1 Health Care 0.122 0.1 0.022

1 Industrials 0.257 0.2 0.057

1 Information Technology 0.151 0.13333 0.017667

1 Materials 0.022 0.066667 -0.044667

2 Communication Services 0.091 0.1 -0.009

2 Consumer Discretionary 0.118 0.1 0.018

2 Consumer Staples 0.097 0.13333 -0.036333

2 Energy 0.04 0.033333 0.0066667

2 Financials 0.102 0.13333 -0.031333

2 Health Care 0.122 0.1 0.022

2 Industrials 0.257 0.2 0.057

⋮

计算类别收益

使用 brinsonAttribution 对象和 categoryReturns 计算投资组合和基准的聚合及周期性类别(行业)收益。

[AggregateCategoryReturns,PeriodicCategoryReturns] = categoryReturns(BrinsonPAobj)

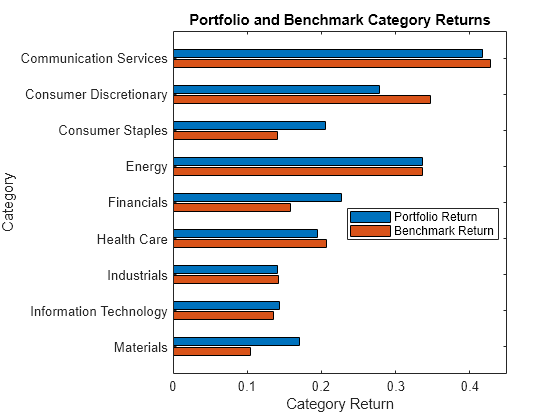

AggregateCategoryReturns=9×3 table

Category AggregatePortfolioReturn AggregateBenchmarkReturn

______________________ ________________________ ________________________

Communication Services 0.41756 0.42797

Consumer Discretionary 0.27772 0.34718

Consumer Staples 0.20572 0.14112

Energy 0.33598 0.33598

Financials 0.22678 0.15838

Health Care 0.19451 0.20679

Industrials 0.14132 0.14253

Information Technology 0.14339 0.13485

Materials 0.17109 0.10402

PeriodicCategoryReturns=108×4 table

Period Category PortfolioReturn BenchmarkReturn

______ ______________________ _______________ _______________

1 Communication Services 0.056262 0.052385

1 Consumer Discretionary 0.079767 0.10017

1 Consumer Staples -0.01485 -0.0033588

1 Energy 0.073093 0.073093

1 Financials -0.0021179 -0.029374

1 Health Care 0.012124 0.022297

1 Industrials 0.0018686 0.0088589

1 Information Technology 0.033481 -0.011315

1 Materials -0.090708 -0.018543

2 Communication Services 0.069253 0.078033

2 Consumer Discretionary -0.023091 -0.036416

2 Consumer Staples 0.0027749 0.00096619

2 Energy -0.0487 -0.0487

2 Financials 0.033379 0.02054

2 Health Care 0.014975 0.015929

2 Industrials 0.047732 0.041906

⋮

计算类别归因

使用 brinsonAttribution 对象和 categoryAttribution 计算投资组合在每个类别(行业)中的业绩归因。

[AggregateCategoryAttribution,PeriodicCategoryAttribution] = categoryAttribution(BrinsonPAobj)

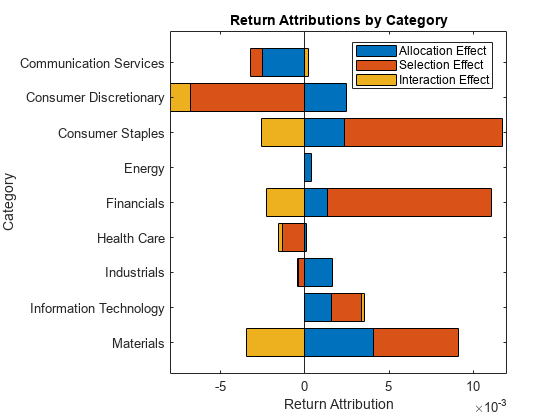

AggregateCategoryAttribution=9×5 table

Category Allocation Selection Interaction ActiveReturn

______________________ __________ ___________ ___________ ____________

Communication Services -0.0025318 -0.00071062 0.0002061 -0.0030363

Consumer Discretionary 0.0024505 -0.00678 -0.0011609 -0.0054903

Consumer Staples 0.0023692 0.0093618 -0.0025511 0.00918

Energy 0.00038824 1.3872e-19 2.7745e-20 0.00038824

Financials 0.0013464 0.0097268 -0.0022858 0.0087874

Health Care 0.00011567 -0.0013031 -0.00028667 -0.0014741

Industrials 0.0016701 -0.00035051 -5.7623e-05 0.001262

Information Technology 0.0015686 0.0017812 0.00016898 0.0035187

Materials 0.0040725 0.0050687 -0.0034678 0.0056734

PeriodicCategoryAttribution=108×7 table

Period LinkingCoefficient Category Allocation Selection Interaction ActiveReturn

______ __________________ ______________________ ___________ ___________ ___________ ____________

1 1.1901 Communication Services -0.00034021 0.00038766 -3.489e-05 1.2564e-05

1 1.1901 Consumer Discretionary 0.0015405 -0.0020403 -0.00036725 -0.00086699

1 1.1901 Consumer Staples 0.00065192 -0.0015322 0.00041752 -0.00046274

1 1.1901 Energy 0.00039006 0 0 0.00039006

1 1.1901 Financials 0.0013774 0.0036342 -0.00085403 0.0041575

1 1.1901 Health Care 0.00016968 -0.0010173 -0.0002238 -0.0010714

1 1.1901 Industrials -0.00032634 -0.0013981 -0.00039845 -0.0021229

1 1.1901 Information Technology -0.00045756 0.0059728 0.0007914 0.0063066

1 1.1901 Materials 0.0014797 -0.004811 0.0032234 -0.00010793

2 1.1935 Communication Services -0.00058016 -0.000878 7.902e-05 -0.0013791

2 1.1935 Consumer Discretionary -0.00089975 0.0013325 0.00023985 0.00067261

2 1.1935 Consumer Staples 0.00045794 0.00024116 -6.5715e-05 0.00063338

2 1.1935 Energy -0.00041514 0 0 -0.00041514

2 1.1935 Financials -0.00021838 0.0017119 -0.0004023 0.0010912

2 1.1935 Health Care 5.19e-05 -9.5418e-05 -2.0992e-05 -6.451e-05

2 1.1935 Industrials 0.0016152 0.0011651 0.00033205 0.0031123

⋮

计算总归因

使用 brinsonAttribution 对象和 totalAttribution 计算投资组合在所有类别(行业)中汇总的总业绩归因。

[AggregateTotalAttribution,PeriodicTotalAttribution] = totalAttribution(BrinsonPAobj)

AggregateTotalAttribution=1×4 table

Allocation Selection Interaction ActiveReturn

__________ _________ ___________ ____________

0.011449 0.016794 -0.0094348 0.018809

PeriodicTotalAttribution=12×6 table

Period LinkingCoefficient Allocation Selection Interaction ActiveReturn

______ __________________ ___________ ___________ ___________ ____________

1 1.1901 0.0044852 -0.00080413 0.0025538 0.0062349

2 1.1935 0.00087285 0.0032617 -0.0025973 0.0015372

3 1.1904 -6.9025e-05 0.0052394 0.00069386 0.0058643

4 1.208 -0.004707 -0.0095748 -0.0046622 -0.018944

5 1.1995 -0.00030704 -0.006091 -0.00061525 -0.0070132

6 1.1935 0.0012025 -0.00026724 0.00058932 0.0015246

7 1.1813 0.0032236 0.017541 -0.0021062 0.018658

8 1.196 0.004629 -0.004929 -0.0018038 -0.0021038

9 1.1927 0.0013046 0.00036681 0.00099195 0.0026634

10 1.1923 0.0032172 0.0023077 -0.0023663 0.0031586

11 1.194 -0.001881 0.00044958 0.0022018 0.00077039

12 1.1918 -0.0022819 0.0069324 -0.0007375 0.003913

生成业绩归因汇总

使用 brinsonAttribution 对象和 summary 生成一个表格,该表格汇总使用布林森模型进行的业绩归因的最终结果(涵盖所有时间段和类别)。

SummaryTable = summary(BrinsonPAobj)

SummaryTable=11×1 table

Brinson Attribution Summary

___________________________

Total Number of Assets 30

Number of Assets in Portfolio 22

Number of Assets in Benchmark 30

Number of Periods 12

Number of Categories 9

Portfolio Return 0.22345

Benchmark Return 0.20464

Active Return 0.018809

Allocation Effect 0.011449

Selection Effect 0.016794

Interaction Effect -0.0094348

生成收益、权重和业绩归因的水平条形图

使用 brinsonAttribution 对象以及 categoryReturnsChart、categoryWeightsChart 和 attributionsChart 生成水平条形图。

categoryReturnsChart(BrinsonPAobj)

categoryWeightsChart(BrinsonPAobj)

attributionsChart(BrinsonPAobj, Style="stacked")

另请参阅

brinsonAttribution | categoryAttribution | categoryReturns | categoryWeights | totalAttribution | summary