risk.validation.plotSpearmanRanks

Syntax

Description

risk.validation.plotSpearmanRanks(

plots the ranks of the observations in Sample1,Sample2)Sample1 against the ranks of the

observations in Sample2. The plot also displays the Spearman rank

correlation coefficient in the lower right corner.

risk.validation.plotSpearmanRanks(

plots into the axes specified by ax,Sample1,Sample2)ax instead of into the current axes

(gca).

risk.validation.plotSpearmanRanks(

plots into the axes specified by Sample1,Sample2,Parent=ax)ax instead of into the current axes

(gca).

h = risk.validation.plotSpearmanRanks(___)

Examples

Load the CreditValidationData data.

load CreditValidationData.matThe table LGDModelsValidationData contains variables RegressionLGD, TobitLGD, and ObservedLGD. RegressionLGD and TobitLGD contain data for predicted loss given default (LGD), and ObservedLGD contains data for observed LGD.

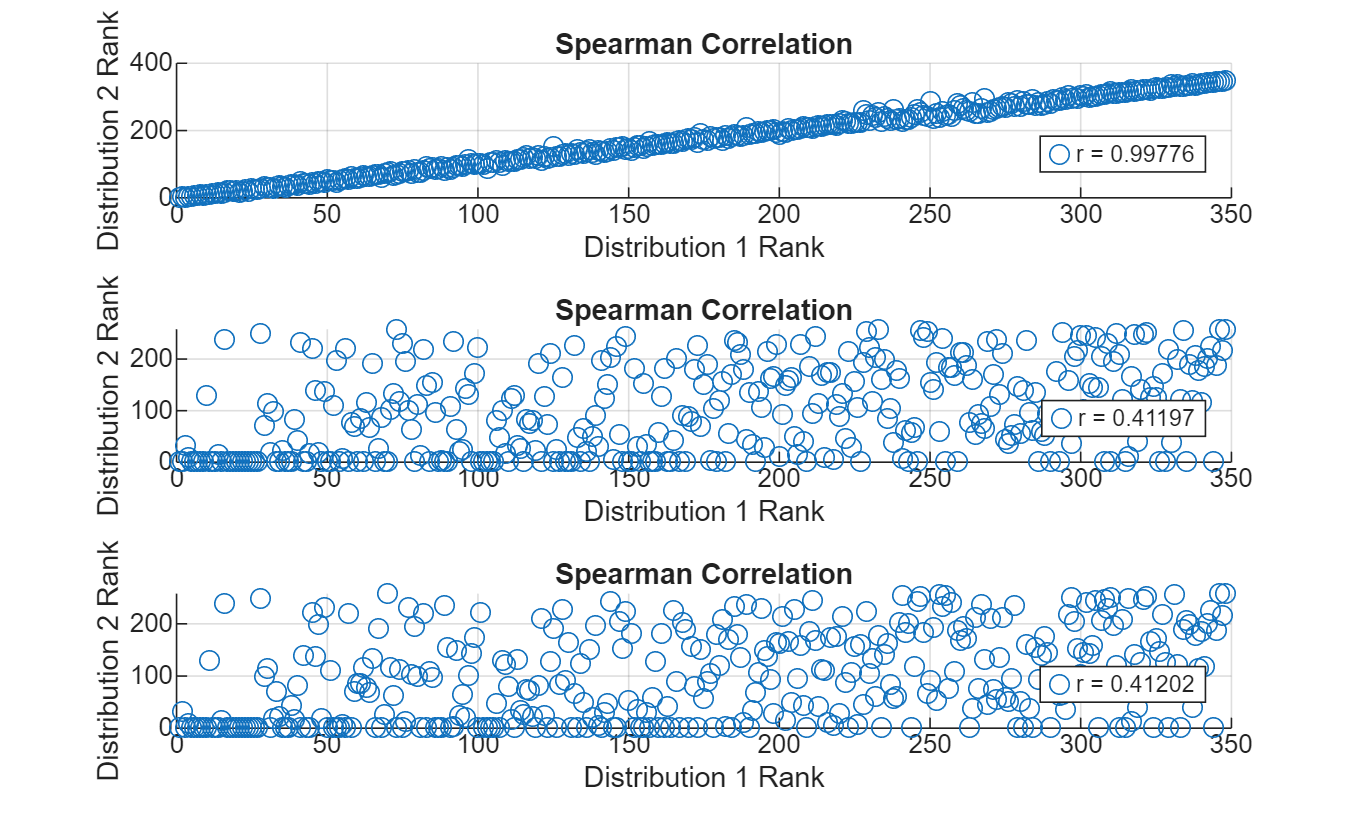

Plot the ranks of the regression model's LGD predictions against the Tobit model's predictions. Then plot the ranks of the observed LGDs against each model's predictions.

Regression = LGDModelsValidationData.RegressionLGD;

Tobit = LGDModelsValidationData.TobitLGD;

Observed = LGDModelsValidationData.ObservedLGD;

tiledlayout("vertical")

nexttile

risk.validation.plotSpearmanRanks(Regression,Tobit)

nexttile

risk.validation.plotSpearmanRanks(Regression,Observed)

nexttile

risk.validation.plotSpearmanRanks(Tobit,Observed)

The plots show that the regression model predictions are highly correlated with the Tobit model predictions. This is consistent with their Spearman correlation of 0.998. However, each model's predictions are only moderately correlated with the observed predictions.

Input Arguments

Output Arguments

References

[1] Basel Committee on Banking Supervision, "Calculation of RWA for market risk." January, 2022. https://www.bis.org/basel_framework/chapter/MAR/32.htm?inforce=20220101&published=20191215.

Version History

Introduced in R2026a