使用时间表处理金融数据

使用时间表根据模拟的每日股票数据可视化和计算每周统计数据。

第 1 步:加载数据。

此示例的数据位于 MAT 文件 SimulatedStock.mat 中,加载以下内容:

与收盘价相对应的日期,

TMW_DATES开盘价,

TMW_OPEN股价每日高点,

TMW_HIGH股价每日低点,

TMW_LOW收盘价,

TMW_CLOSE, TMW_CLOSE_MISSING每日交易量,

TMW_VOLUME表中的数据,

TMW_TB

load SimulatedStock.mat TMW_*

第 2 步:创建时间表。

在时间表中,您可以使用金融时间序列而不是向量。当使用 timetable 时,您可以轻松跟踪日期。您可以根据日期操作数据序列,因为 timetable 对象能够跟踪时间序列的管理。

使用 MATLAB® timetable 函数创建 timetable 对象。或者,您也可以使用 MATLAB 转换函数 table2timetable 将表转换为时间表。在此示例中,时间表 TMW_TT 是从表转换构建的,仅用于说明目的。创建 timetable 对象后,您可以使用 timetable 对象的 Description 字段存储关于时间表的元信息。

% Create a timetable from vector input TMW = timetable(TMW_OPEN,TMW_HIGH,TMW_LOW,TMW_CLOSE_MISSING,TMW_VOLUME, ... 'VariableNames',{'Open','High','Low','Close','Volume'},'RowTimes',TMW_DATES); % Convert from a table to a timetable TMW_TT = table2timetable(TMW_TB,'RowTimes',TMW_DATES); TMW.Properties.Description = 'Simulated stock data.'; TMW.Properties

ans =

TimetableProperties with properties:

Description: 'Simulated stock data.'

UserData: []

DimensionNames: {'Time' 'Variables'}

VariableNames: {'Open' 'High' 'Low' 'Close' 'Volume'}

VariableTypes: ["double" "double" "double" "double" "double"]

VariableDescriptions: {}

VariableUnits: {}

VariableContinuity: []

RowTimes: [1000×1 datetime]

StartTime: 04-Sep-2012

SampleRate: NaN

TimeStep: NaN

Events: []

CustomProperties: No custom properties are set.

Use addprop and rmprop to modify CustomProperties.

第 3 步:计算基本的数据统计,并填充缺失数据。

使用 MATLAB summary 函数查看 timetable 数据的基本统计信息。通过查看每个变量的摘要,您可以确定缺失值。然后,您可以使用 MATLAB fillmissing 函数通过指定填充方法来填充时间表中的缺失数据。

summaryTMW = summary(TMW); summaryTMW.Close

ans = struct with fields:

Size: [1000 1]

Type: 'double'

Description: ''

Units: ''

Continuity: []

NumMissing: 3

Min: 83.4200

Median: 116.7500

Max: 162.1100

Mean: 117.9487

Std: 18.2554

TMW = fillmissing(TMW,'linear');

summaryTMW = summary(TMW);

summaryTMW.Closeans = struct with fields:

Size: [1000 1]

Type: 'double'

Description: ''

Units: ''

Continuity: []

NumMissing: 0

Min: 83.4200

Median: 116.7050

Max: 162.1100

Mean: 117.8929

Std: 18.2566

summaryTMW.Time

ans = struct with fields:

Size: [1000 1]

Type: 'datetime'

TimeZone: ''

SampleRate: NaN

StartTime: 04-Sep-2012

NumMissing: 0

Min: 04-Sep-2012

Median: 31-Aug-2014

Max: 24-Aug-2016

Mean: 31-Aug-2014

Std: 10058:44:06

TimeStep: NaN

第 4 步:可视化数据。

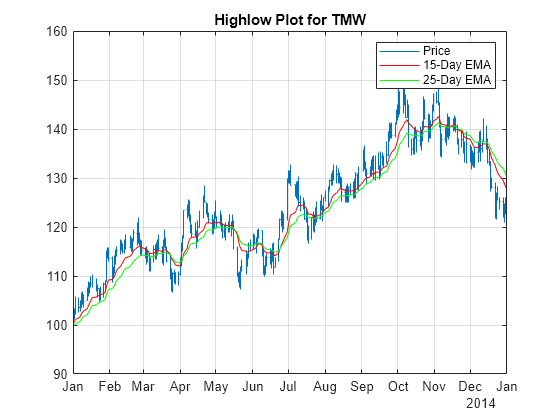

要可视化时间表数据,请使用金融图表函数,例如 highlow 或 movavg。在此示例中,移动平均线信息与 highlow 绘制在同一张图上,以提供完整的可视化信息。要获得 2014 年的股票表现,请使用 MATLAB timerange 函数选择 timetable 的行。要可视化技术指标,例如平滑异同移动平均线 (MACD),请将 timetable 对象传递给 macd 函数进行分析。

index = timerange(datetime('01-Jan-2014','Locale','en_US'),datetime('31-Dec-2014','Locale','en_US'),'closed'); highlow(TMW(index,:)); hold on ema15 = movavg(TMW(:,'Close'),'exponential',15); ema25 = movavg(TMW(:,'Close'),'exponential',25); ema15 = ema15(index,:); ema25 = ema25(index,:); plot(ema15.Time,ema15.Close,'r'); plot(ema25.Time,ema25.Close,'g'); hold off legend('Price','15-Day EMA','25-Day EMA') title('Highlow Plot for TMW')

[macdLine, signalLine] = macd(TMW(:,'Close')); plot(macdLine.Time,macdLine.Close); hold on plot(signalLine.Time,signalLine.Close); hold off title('MACD for TMW') legend('MACD Line', 'Signal Line')

第 5 步:创建每周收益和波动率序列。

要根据每日股票价格计算每周收益,须将数据采样周期从每天变为每周。使用时间表时,请使用 MATLAB 函数 retime 或 synchronize 结合各种聚合方法计算每周的统计信息。要基于一个时间向量来调整时间表数据,请使用 retime涉及多个时间表时,需使用 synchronize。

weeklyOpen = retime(TMW(:,'Open'),'weekly','firstvalue'); weeklyHigh = retime(TMW(:,'High'),'weekly','max'); weeklyLow = retime(TMW(:,'Low'),'weekly','min'); weeklyClose = retime(TMW(:,'Close'),'weekly','lastvalue'); weeklyTMW = [weeklyOpen,weeklyHigh,weeklyLow,weeklyClose]; weeklyTMW = synchronize(weeklyTMW,TMW(:,'Volume'),'weekly','sum'); head(weeklyTMW)

Time Open High Low Close Volume

___________ ______ ______ ______ ______ __________

02-Sep-2012 100 102.38 98.45 99.51 2.7279e+07

09-Sep-2012 99.72 101.55 96.52 97.52 2.8518e+07

16-Sep-2012 97.35 97.52 92.6 93.73 2.9151e+07

23-Sep-2012 93.55 98.03 92.25 97.35 3.179e+07

30-Sep-2012 97.3 103.15 96.68 99.66 3.3761e+07

07-Oct-2012 99.76 106.61 98.7 104.23 3.1299e+07

14-Oct-2012 104.54 109.75 100.55 103.77 3.1534e+07

21-Oct-2012 103.84 104.32 96.95 97.41 3.1706e+07

要对 timetable 中的条目执行计算,请使用 MATLAB rowfun 函数,对以每周为采样周期的时间表中的每一行应用函数。

returnFunc = @(open,high,low,close,volume) log(close) - log(open); weeklyReturn = rowfun(returnFunc,weeklyTMW,'OutputVariableNames',{'Return'}); weeklyStd = retime(TMW(:,'Close'),'weekly',@std); weeklyStd.Properties.VariableNames{'Close'} = 'Volatility'; weeklyTMW = [weeklyReturn,weeklyStd,weeklyTMW]

weeklyTMW=208×7 timetable

Time Return Volatility Open High Low Close Volume

___________ ___________ __________ ______ ______ ______ ______ __________

02-Sep-2012 -0.004912 0.59386 100 102.38 98.45 99.51 2.7279e+07

09-Sep-2012 -0.022309 0.63563 99.72 101.55 96.52 97.52 2.8518e+07

16-Sep-2012 -0.037894 0.93927 97.35 97.52 92.6 93.73 2.9151e+07

23-Sep-2012 0.039817 2.0156 93.55 98.03 92.25 97.35 3.179e+07

30-Sep-2012 0.023965 1.1014 97.3 103.15 96.68 99.66 3.3761e+07

07-Oct-2012 0.043833 1.3114 99.76 106.61 98.7 104.23 3.1299e+07

14-Oct-2012 -0.0073929 1.8097 104.54 109.75 100.55 103.77 3.1534e+07

21-Oct-2012 -0.063922 2.1603 103.84 104.32 96.95 97.41 3.1706e+07

28-Oct-2012 -0.028309 0.9815 97.45 99.1 92.58 94.73 1.9866e+07

04-Nov-2012 -0.00010566 1.224 94.65 96.1 90.82 94.64 3.5043e+07

11-Nov-2012 0.077244 2.4854 94.39 103.98 93.84 101.97 3.0624e+07

18-Nov-2012 0.022823 0.55896 102.23 105.27 101.24 104.59 2.5803e+07

25-Nov-2012 -0.012789 1.337 104.66 106.02 100.85 103.33 3.1402e+07

02-Dec-2012 -0.043801 0.2783 103.37 103.37 97.69 98.94 3.2136e+07

09-Dec-2012 -0.063475 1.9826 99.02 99.09 91.34 92.93 3.4447e+07

16-Dec-2012 0.0025787 1.2789 92.95 94.2 88.58 93.19 3.3247e+07

⋮

另请参阅

timetable | retime | synchronize | timerange | withtol | vartype | issorted | sortrows | unique | diff | isregular | rmmissing | fillmissing