Using MATLAB to Move to the Next Generation of GRADE Model

Nadége Lespagnol, Euler Hermes

Euler Hermes (EH) is the leading B2B credit risk business of the Allianz Group, helping customers protect themselves from bad debt.

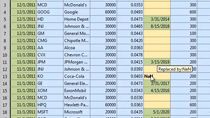

EH has a strategic objective to centralize all credit assessment model calibration data, model design, and model monitoring processes in one common modeling platform, helping to meet the regulatory requirement for reconciliation and transparency for all credit assessment models. EH’s proprietary GRADE model is a probability of default (PD) model used in both the underwriting process and in the allocation of risk capital.

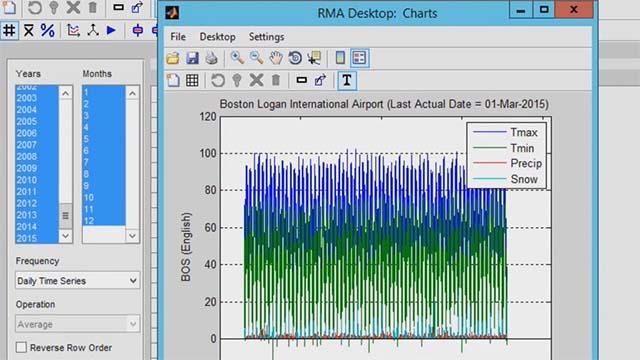

In 2020, EH launched a transformation project to migrate all credit risk models from a legacy infrastructure to MATLAB® running on AWS®. EH used components of the MATLAB Model Risk Management solution to develop and maintain the full suite of credit risk models, which are based on fuzzy logic approaches as well as tree-based algorithms.

In this presentation, learn how EH has built a new model design architecture with MATLAB and AWS that will allow many improvements in the process of building and testing future models.

Published: 6 Oct 2021

Featured Product