summary

Generate summary table of backtest results

Description

summaryTable = summary(backtester)runBacktest function.

Examples

The MATLAB® backtesting engine runs backtests of portfolio investment strategies over time series of asset price data. You can use summary to compare multiple strategies over the same market scenario. This example shows how to examine the results of a backtest with two strategies.

Load Data

Load one year of stock price data. For readability, this example uses a subset of the DJIA stocks.

% Read table of daily adjusted close prices for 2006 DJIA stocks T = readtable('dowPortfolio.xlsx'); % Prune the table to include only the dates and selected stocks timeColumn = "Dates"; assetSymbols = ["BA", "CAT", "DIS", "GE", "IBM", "MCD", "MSFT"]; T = T(:,[timeColumn assetSymbols]); % Convert to timetable pricesTT = table2timetable(T,'RowTimes','Dates'); % View the final asset price timetable head(pricesTT)

Dates BA CAT DIS GE IBM MCD MSFT

___________ _____ _____ _____ _____ _____ _____ _____

03-Jan-2006 68.63 55.86 24.18 33.6 80.13 32.72 26.19

04-Jan-2006 69.34 57.29 23.77 33.56 80.03 33.01 26.32

05-Jan-2006 68.53 57.29 24.19 33.47 80.56 33.05 26.34

06-Jan-2006 67.57 58.43 24.52 33.7 82.96 33.25 26.26

09-Jan-2006 67.01 59.49 24.78 33.61 81.76 33.88 26.21

10-Jan-2006 67.33 59.25 25.09 33.43 82.1 33.91 26.35

11-Jan-2006 68.3 59.28 25.33 33.66 82.19 34.5 26.63

12-Jan-2006 67.9 60.13 25.41 33.25 81.61 33.96 26.48

The inverse variance strategy requires some price history to initialize, so you can allocate a portion of the data to use for setting initial weights. By doing this, you can "warm start" the backtest.

warmupRange = 1:20; testRange = 21:height(pricesTT);

Create Strategies

Define an investment strategy by using the backtestStrategy function. This example builds two strategies:

Equal weighted

Inverse variance

This example does not provide details on how to build the strategies. For more information on creating strategies, see backtestStrategy. The strategy rebalance functions are implemented in the Rebalance Functions section.

% Create the strategies ewInitialWeights = equalWeightFcn([],pricesTT(warmupRange,:)); ewStrategy = backtestStrategy("EqualWeighted",@equalWeightFcn, ... 'RebalanceFrequency',20, ... 'TransactionCosts',[0.0025 0.005], ... 'LookbackWindow',0, ... 'InitialWeights',ewInitialWeights)

ewStrategy =

backtestStrategy with properties:

Name: "EqualWeighted"

RebalanceFcn: @equalWeightFcn

RebalanceFrequency: 20

TransactionCosts: [0.0025 0.0050]

LookbackWindow: 0

InitialWeights: [0.1429 0.1429 0.1429 0.1429 0.1429 0.1429 0.1429]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0×0 struct]

EngineDataList: [0×0 string]

ivInitialWeights = inverseVarianceFcn([],pricesTT(warmupRange,:)); ivStrategy = backtestStrategy("InverseVariance",@inverseVarianceFcn, ... 'RebalanceFrequency',20, ... 'TransactionCosts',[0.0025 0.005], ... 'InitialWeights',ivInitialWeights)

ivStrategy =

backtestStrategy with properties:

Name: "InverseVariance"

RebalanceFcn: @inverseVarianceFcn

RebalanceFrequency: 20

TransactionCosts: [0.0025 0.0050]

LookbackWindow: [0 Inf]

InitialWeights: [0.1401 0.0682 0.0795 0.2187 0.1900 0.1875 0.1160]

ManagementFee: 0

ManagementFeeSchedule: 1y

PerformanceFee: 0

PerformanceFeeSchedule: 1y

PerformanceHurdle: 0

UserData: [0×0 struct]

EngineDataList: [0×0 string]

% Aggregate the strategies into an array

strategies = [ewStrategy ivStrategy];Run Backtest

Create a backtesting engine and run a backtest over a year of stock data. For more information on creating backtesting engines, see backtestEngine. The software initializes several properties of the backtestEngine object to empty. These read-only properties are populated by the engine after you run the backtest.

% Create the backtesting engine using the default settings

backtester = backtestEngine(strategies)backtester =

backtestEngine with properties:

Strategies: [1×2 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: []

Returns: []

Positions: []

Turnover: []

BuyCost: []

SellCost: []

TransactionCosts: []

Fees: []

Run the backtest using runBacktest.

% Run the backtest

backtester = runBacktest(backtester,pricesTT(testRange,:));Examine Summary Results

The summary function uses the results of the backtest and returns a table of high-level results from the backtest.

s1 = summary(backtester)

s1=9×2 table

EqualWeighted InverseVariance

_____________ _______________

TotalReturn 0.17567 0.17155

SharpeRatio 0.097946 0.10213

Volatility 0.0074876 0.0069961

AverageTurnover 0.0007014 0.0024246

MaxTurnover 0.021107 0.097472

AverageReturn 0.00073178 0.00071296

MaxDrawdown 0.097647 0.096299

AverageBuyCost 0.018532 0.061913

AverageSellCost 0.037064 0.12383

Each row of the table output is a measurement of the performance of a strategy. Each strategy occupies a column. The summary function reports on the following metrics:

TotalReturn— The nonannulaized total return of the strategy, inclusive of fees, over the full backtest period.SharpeRatio— The nonannualized Sharpe ratio of each strategy over the backtest. For more information, seesharpe.Volatility— The nonannualized standard deviation of per-time-step strategy returns.AverageTurnover— The average per-time-step portfolio turnover, expressed as a decimal percentage.MaxTurnover— The maximum portfolio turnover in a single rebalance, expressed as a decimal percentage.AverageReturn—The arithmetic mean of the per-time step portfolio returns.MaxDrawdown— The maximum drawdown of the portfolio, expressed as a decimal percentage. For more information, seemaxdrawdown.AverageBuyCost— The average per-time-step transaction costs the portfolio incurred for asset purchases.AverageSellCost— The average per-time-step transaction costs the portfolio incurred for asset sales.

Sometimes it is useful to transpose the summary table when plotting the metrics of different strategies.

s2 = rows2vars(s1);

s2.Properties.VariableNames{1} = 'StrategyName's2=2×10 table

StrategyName TotalReturn SharpeRatio Volatility AverageTurnover MaxTurnover AverageReturn MaxDrawdown AverageBuyCost AverageSellCost

___________________ ___________ ___________ __________ _______________ ___________ _____________ ___________ ______________ _______________

{'EqualWeighted' } 0.17567 0.097946 0.0074876 0.0007014 0.021107 0.00073178 0.097647 0.018532 0.037064

{'InverseVariance'} 0.17155 0.10213 0.0069961 0.0024246 0.097472 0.00071296 0.096299 0.061913 0.12383

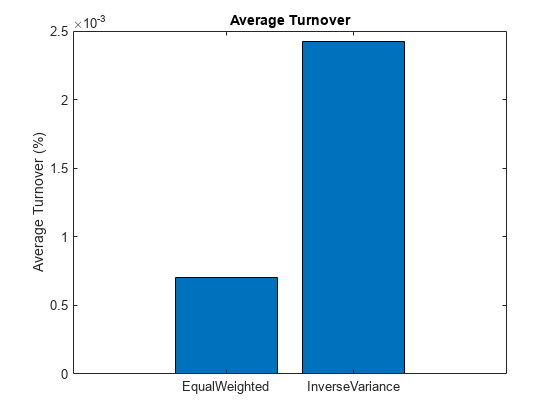

bar(s2.AverageTurnover) title('Average Turnover') ylabel('Average Turnover (%)') set(gca,'xticklabel',s2.StrategyName)

Examine Detailed Results

After you run the backtest, the backtestEngine object updates the read-only fields with the detailed results of the backtest. The Returns, Positions, Turnover, BuyCost, SellCost, and Fees properties each contain a timetable of results. Since this example uses daily price data in the backtest, these timetables hold daily results.

backtester

backtester =

backtestEngine with properties:

Strategies: [1×2 backtestStrategy]

RiskFreeRate: 0

CashBorrowRate: 0

RatesConvention: "Annualized"

Basis: 0

InitialPortfolioValue: 10000

DateAdjustment: "Previous"

PayExpensesFromCash: 0

NumAssets: 7

Returns: [230×2 timetable]

Positions: [1×1 struct]

Turnover: [230×2 timetable]

BuyCost: [230×2 timetable]

SellCost: [230×2 timetable]

TransactionCosts: [1×1 struct]

Fees: [1×1 struct]

Returns

The Returns property holds a timetable of strategy (simple) returns for each time step. These returns are inclusive of all transaction fees.

head(backtester.Returns)

Time EqualWeighted InverseVariance

___________ _____________ _______________

02-Feb-2006 -0.007553 -0.0070957

03-Feb-2006 -0.0037771 -0.003327

06-Feb-2006 -0.0010094 -0.0014312

07-Feb-2006 0.0053284 0.0020578

08-Feb-2006 0.0099755 0.0095781

09-Feb-2006 -0.0026871 -0.0014999

10-Feb-2006 0.0048374 0.0059589

13-Feb-2006 -0.0056868 -0.0051232

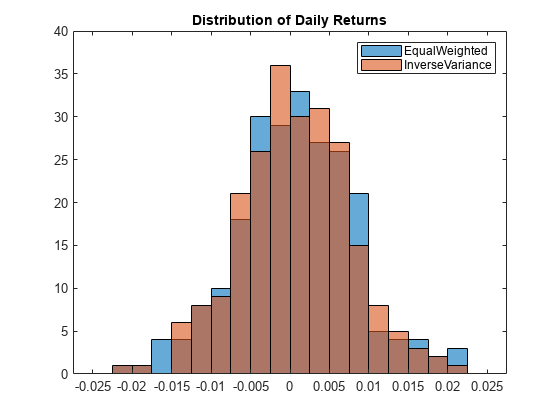

binedges = -0.025:0.0025:0.025; h1 = histogram(backtester.Returns.EqualWeighted,'BinEdges',binedges); hold on histogram(backtester.Returns.InverseVariance,'BinEdges',binedges); hold off title('Distribution of Daily Returns') legend([strategies.Name]);

Positions

The Positions property holds a structure of timetables, one per strategy.

backtester.Positions

ans = struct with fields:

EqualWeighted: [231×8 timetable]

InverseVariance: [231×8 timetable]

The Positions timetable of each strategy holds the per-time-step positions for each asset as well as the Cash asset (which earns the risk-free rate). The Positions timetables contain one more row than the other results timetables because the Positions timetables include initial positions of the strategy as their first row. You can consider the initial positions as the Time = 0 portfolio positions. In this example, the Positions timetables start with February 1, while the others start on February 2.

head(backtester.Positions.InverseVariance)

Time Cash BA CAT DIS GE IBM MCD MSFT

___________ ___________ ______ ______ ______ ______ ______ ______ ______

01-Feb-2006 0 1401.2 682.17 795.14 2186.8 1900.1 1874.9 1159.8

02-Feb-2006 0 1402.8 673.74 789.74 2170.8 1883.5 1863.6 1145

03-Feb-2006 1.0987e-12 1386.5 671.2 787.2 2167.3 1854.3 1890.5 1139

06-Feb-2006 1.0971e-12 1391.9 676.78 785.62 2161.1 1843.6 1899.1 1123.8

07-Feb-2006 0 1400 661.66 840.23 2131.9 1851.6 1902.3 1114.5

08-Feb-2006 -2.2198e-12 1409.8 677.9 846.58 2160.4 1878.2 1911 1113.2

09-Feb-2006 0 1414.8 674.35 840.87 2172.2 1869 1908.3 1102.6

10-Feb-2006 0 1425.1 677.29 839.6 2195.8 1890.6 1909.3 1103.9

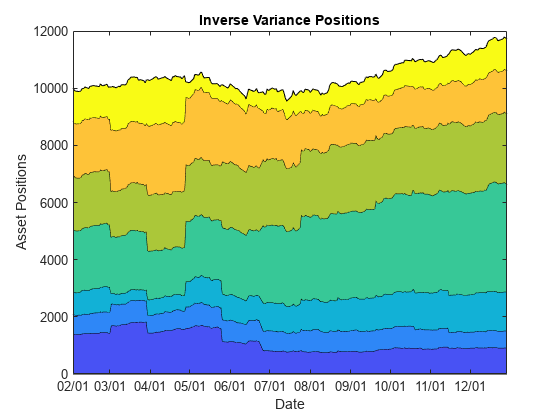

% Plot the change of asset allocation over time t = backtester.Positions.InverseVariance.Time; positions = backtester.Positions.InverseVariance.Variables; h = area(t,positions); title('Inverse Variance Positions'); xlabel('Date'); ylabel('Asset Positions'); xtickformat('MM/dd'); ylim([0 12000]) xlim([t(1) t(end)]) cm = parula(numel(h)); for i = 1:numel(h) set(h(i),'FaceColor',cm(i,:)); end

Turnover

The Turnover timetable holds the per-time-step portfolio turnover.

head(backtester.Turnover)

Time EqualWeighted InverseVariance

___________ _____________ _______________

02-Feb-2006 0 0

03-Feb-2006 0 0

06-Feb-2006 0 0

07-Feb-2006 0 0

08-Feb-2006 0 0

09-Feb-2006 0 0

10-Feb-2006 0 0

13-Feb-2006 0 0

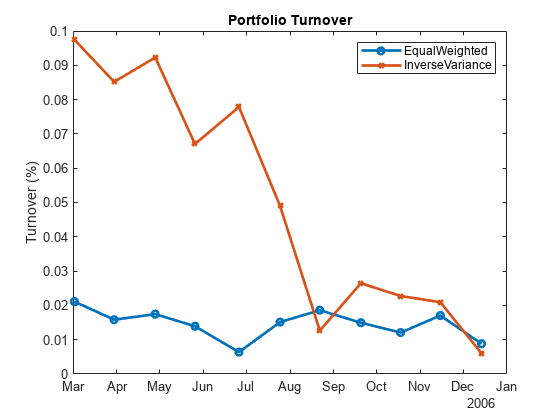

Depending on your rebalance frequency, the Turnover table can contain mostly zeros. Removing these zeros when you visualize the portfolio turnover is useful.

nonZeroIdx = sum(backtester.Turnover.Variables,2) > 0; to = backtester.Turnover(nonZeroIdx,:); plot(to.Time,to.EqualWeighted,'-o',to.Time,to.InverseVariance,'-x',... 'LineWidth',2,'MarkerSize',5); legend([strategies.Name]); title('Portfolio Turnover'); ylabel('Turnover (%)');

BuyCost and SellCost

The BuyCost and SellCost timetables hold the per-time-step transaction fees for each type of transaction, purchases, and sales.

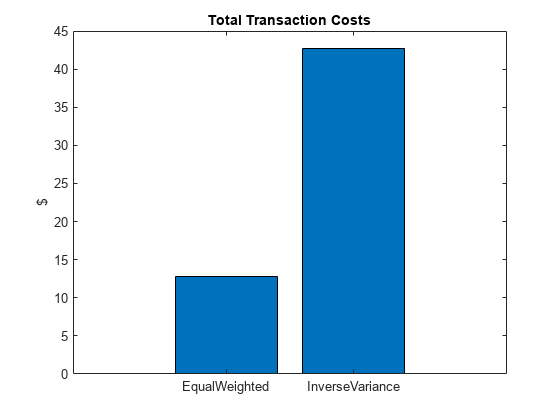

totalCost = sum(backtester.BuyCost{:,:}) + sum(backtester.SellCost{:,:});

bar(totalCost);

title('Total Transaction Costs');

ylabel('$')

set(gca,'xticklabel',[strategies.Name])

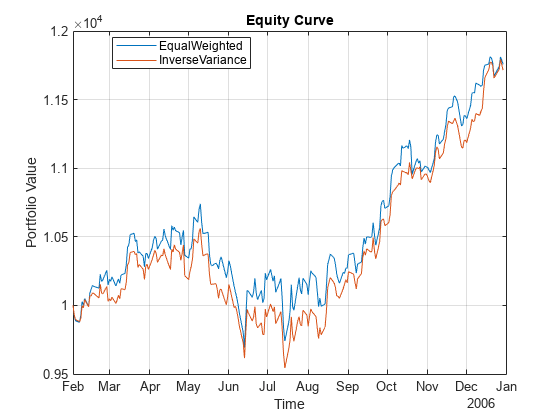

Generate Equity Curve

Use equityCurve to plot the equity curve for the equal weighted and inverse variance strategies.

equityCurve(backtester)

Rebalance Functions

This section contains the implementation of the strategy rebalance functions. For more information on creating strategies and writing rebalance functions, see backtestStrategy.

function new_weights = equalWeightFcn(current_weights, pricesTT) %#ok<INUSL> % Equal weighted portfolio allocation nAssets = size(pricesTT, 2); new_weights = ones(1,nAssets); new_weights = new_weights / sum(new_weights); end

function new_weights = inverseVarianceFcn(current_weights, pricesTT) %#ok<INUSL> % Inverse-variance portfolio allocation assetReturns = tick2ret(pricesTT); assetCov = cov(assetReturns{:,:}); new_weights = 1 ./ diag(assetCov); new_weights = new_weights / sum(new_weights); end

Input Arguments

Output Arguments

Version History

Introduced in R2020b

See Also

backtestStrategy | backtestEngine | runBacktest | equityCurve