绩效度量说明

使用三个金融时间序列对象,并结合以下各项的绩效数据,以便说明投资绩效度量的函数:

一个积极管理的大盘股价值共同基金

一个大盘市场指数

90 天期国库券

这些数据是覆盖五年期间的每月总收益价格。

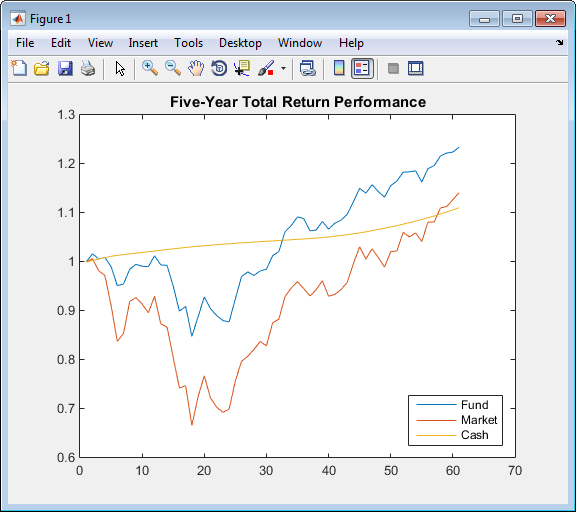

下图说明在 5 年期开始时初始投资 1 美元后,每个序列的总收益绩效:

load FundMarketCash plot(TestData) hold on title('\bfFive-Year Total Return Performance'); legend('Fund','Market','Cash','Location','SouthEast'); hold off

每个序列收益的均值 (Mean) 和标准差 (Sigma) 为

Returns = tick2ret(TestData); Assets Mean = mean(Returns) Sigma = std(Returns, 1)

这得到以下结果:

Assets =

'Fund' 'Market' 'Cash'

Mean =

0.0038 0.0030 0.0017

Sigma =

0.0229 0.0389 0.0009

另请参阅

sharpe | inforatio | portalpha | lpm | elpm | maxdrawdown | emaxdrawdown | ret2tick | tick2ret