simByHybrid

Description

[

specifies options using one or more name-value arguments in addition to the input

arguments in the previous syntax.Paths,Times,Z] = simByHybrid(___,Name=Value)

You can perform quasi-Monte Carlo simulations using the name-value arguments for

MonteCarloMethod, QuasiSequence, and

BrownianMotionMethod. For more information, see Quasi-Monte Carlo Simulation.

Examples

Input Arguments

Name-Value Arguments

Output Arguments

More About

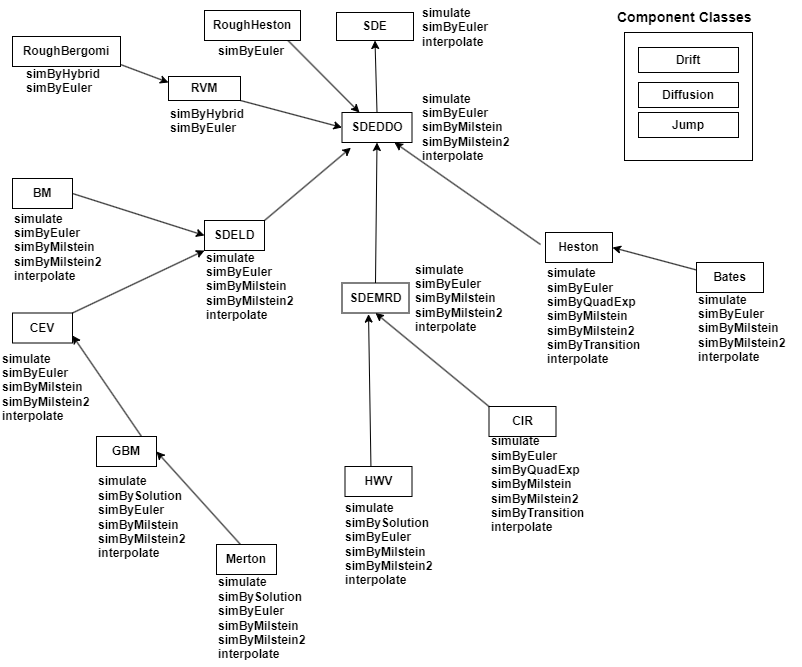

There are inheritance relationships among the SDE classes.

The following figure illustrates the inheritance relationships.

For more information, see SDE Class Hierarchy.

Algorithms

This function simulates any vector-valued SDE of the form

where:

X is an NVars-by-

1state vector of process variables (for example, short rates or equity prices) to simulate.W is an NBrowns-by-

1Brownian motion vector.F is an NVars-by-

1vector-valued drift-rate function.G is an NVars-by-NBrowns matrix-valued diffusion-rate function.

simByHybrid simulates NTrials

sample paths of NVars correlated state variables driven by

NBrowns Brownian motion sources of risk over

NPeriods consecutive observation periods, using the hybrid method

to approximate continuous-time stochastic processes.

This simulation engine provides a discrete-time approximation of the underlying generalized continuous-time process. The simulation is derived directly from the stochastic differential equation of motion. Thus, the discrete-time process approaches the true continuous-time process only as

DeltaTimeapproaches zero.The input argument

Zallows you to directly specify the noise-generation process. This process takes precedence over theCorrelationparameter of thervmorroughbergomiobject and the value of theAntitheticinput flag and theQuasiMonteCarloargument. If you do not specify a value forZ,simByHybridgenerates correlated Gaussian variates, with or without antithetic sampling as requested.The end-of-period

Processesargument allows you to terminate a given trial early. At the end of each time step,simByHybridtests the state vector Xt for an all-NaNcondition. Thus, to signal an early termination of a given trial, all elements of the state vector Xt must beNaN. This test enables a user-definedProcessesfunction to signal early termination of a trial, and offers significant performance benefits in some situations (for example, pricing down-and-out barrier options).

References

[1] Bennedsen, M., A. Lunde and M.S. Pakkanen. “Hybrid Scheme for Brownian Semistationary.” Finance and Stochastics, 2017, Vol. 21, No. 4, pp. 931–965.

Version History

Introduced in R2023bSee Also

rvm | simByEuler | roughbergomi

Topics

- Implementing Multidimensional Equity Market Models, Implementation 5: Using the simByEuler Method

- Simulating Equity Prices

- Simulating Interest Rates

- Stratified Sampling

- Price American Basket Options Using Standard Monte Carlo and Quasi-Monte Carlo Simulation

- Base SDE Models

- Drift and Diffusion Models

- Linear Drift Models

- Parametric Models

- SDEs

- SDE Models

- SDE Class Hierarchy

- Quasi-Monte Carlo Simulation

- Performance Considerations