simByEuler

Simulate Bates sample paths by Euler

approximation

Description

[

simulates Paths,Times,Z,N] = simByEuler(MDL,NPeriods)NTrials sample paths of Bates bivariate models driven

by NBrowns Brownian motion sources of risk and

NJumps compound Poisson processes representing the arrivals

of important events over NPeriods consecutive observation

periods. The simulation approximates continuous-time stochastic processes by the

Euler approach.

[

specifies options using one or more name-value pair arguments in addition to the

input arguments in the previous syntax.Paths,Times,Z,N] = simByEuler(___,Name,Value)

You can perform quasi-Monte Carlo simulations using the name-value arguments for

MonteCarloMethod, QuasiSequence, and

BrownianMotionMethod. For more information, see Quasi-Monte Carlo Simulation.

Examples

Input Arguments

Name-Value Arguments

Output Arguments

More About

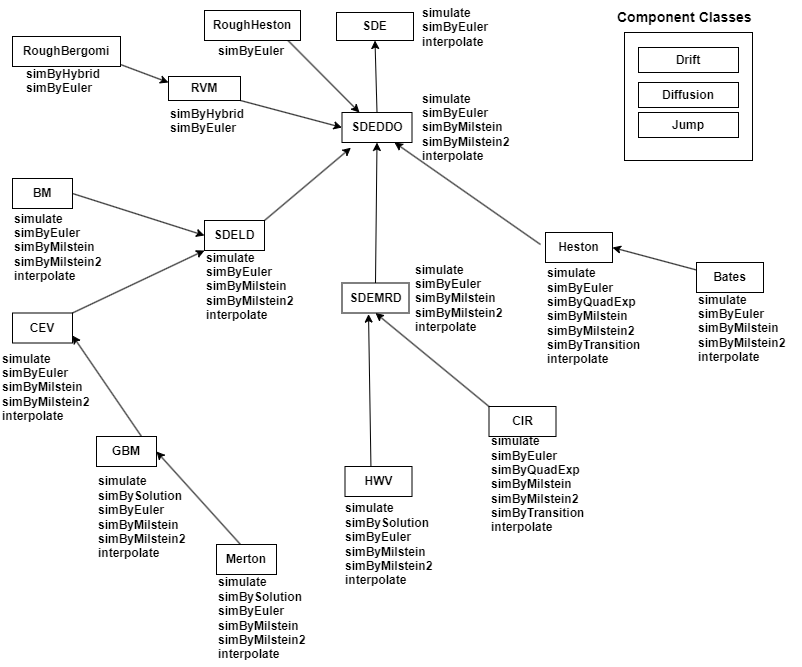

There are inheritance relationships among the SDE classes.

The following figure illustrates the inheritance relationships.

For more information, see SDE Class Hierarchy.

Algorithms

Bates models are bivariate composite models. Each Bates model consists of two coupled univariate models.

One model is a geometric Brownian motion (

gbm) model with a stochastic volatility function and jumps.This model usually corresponds to a price process whose volatility (variance rate) is governed by the second univariate model.

The other model is a Cox-Ingersoll-Ross (

cir) square root diffusion model.This model describes the evolution of the variance rate of the coupled Bates price process.

This simulation engine provides a discrete-time approximation of the underlying

generalized continuous-time process. The simulation is derived directly from the

stochastic differential equation of motion. Thus, the discrete-time process approaches

the true continuous-time process only as DeltaTime approaches

zero.

References

[1] Deelstra, Griselda, and Freddy Delbaen. “Convergence of Discretized Stochastic (Interest Rate) Processes with Stochastic Drift Term.” Applied Stochastic Models and Data Analysis, Vol. 14, No. 1, 1998, pp. 77–84.

[2] Higham, Desmond, and Xuerong Mao. “Convergence of Monte Carlo Simulations Involving the Mean-Reverting Square Root Process.” The Journal of Computational Finance, Vol. 8, No. 3, (2005): 35–61.

[3] Lord, Roger, Remmert Koekkoek, and Dick Van Dijk. “A Comparison of Biased Simulation Schemes for Stochastic Volatility Models.” Quantitative Finance, Vol. 10, No. 2 (February 2010): 177–94.

Version History

Introduced in R2020aSee Also

Topics

- Implementing Multidimensional Equity Market Models, Implementation 5: Using the simByEuler Method

- Simulating Equity Prices

- Simulating Interest Rates

- Stratified Sampling

- Price American Basket Options Using Standard Monte Carlo and Quasi-Monte Carlo Simulation

- Base SDE Models

- Drift and Diffusion Models

- Linear Drift Models

- Parametric Models

- SDEs

- SDE Models

- SDE Class Hierarchy

- Quasi-Monte Carlo Simulation

- Performance Considerations