creditscorecard

Create creditscorecard object to build credit scorecard

model

Description

Build a credit scorecard model by creating a

creditscorecard object and specify input data in a table

format.

After creating a creditscorecard object, you can use the

associated object functions to bin the data and perform logistic regression analysis

to develop a credit scorecard model to guide credit decisions. This workflow shows

how to develop a credit scorecard model.

Use

screenpredictors(Risk Management Toolbox) from Risk Management Toolbox™ to pare down a potentially large set of predictors to a subset that is most predictive of the credit score card response variable. Use this subset of predictors when creating thecreditscorecardobject.Create a

creditscorecardobject (see Create creditscorecard and Properties).Bin the data using

autobinning.Fit a logistic regression model using

fitmodelorfitConstrainedModel.Review and format the credit scorecard points using

displaypointsandformatpoints. At this point in the workflow, if you have a license for Risk Management Toolbox, you have the option to create acompactCreditScorecardobject (csc) using thecompactfunction. You can then use the following functionsdisplaypoints(Risk Management Toolbox),score(Risk Management Toolbox), andprobdefault(Risk Management Toolbox) from the Risk Management Toolbox with thecscobject.Score the data using

score.Calculate the probabilities of default for the data using

probdefault.Validate the quality of the credit scorecard model using

validatemodel.

For more detailed information on this workflow, see Credit Scorecard Modeling Workflow.

Creation

Description

sc = creditscorecard(___,Name,Value)sc =

creditscorecard(data,'GoodLabel',0,'IDVar','CustID','ResponseVar','status','PredictorVars',{'CustAge','CustIncome'},'WeightsVar','RowWeights','BinMissingData',true).

You can specify multiple name-value pairs.

Note

To use observation (sample) weights in the credit scorecard

workflow, when creating a creditscorecard object,

you must use the optional name-value pair

WeightsVar to define which column in the

data contains the weights.

Input Arguments

Name-Value Arguments

Output Arguments

Properties

Object Functions

autobinning | Perform automatic binning of given predictors |

bininfo | Return predictor’s bin information |

predictorinfo | Summary of credit scorecard predictor properties |

modifypredictor | Set properties of credit scorecard predictors |

fillmissing | Replace missing values for credit scorecard predictors |

modifybins | Modify predictor’s bins |

bindata | Binned predictor variables |

plotbins | Plot histogram counts for predictor variables |

fitmodel | Fit logistic regression model to Weight of Evidence (WOE) data |

fitConstrainedModel | Fit logistic regression model to Weight of Evidence (WOE) data subject to constraints on model coefficients |

setmodel | Set model predictors and coefficients |

displaypoints | Return points per predictor per bin |

formatpoints | Format scorecard points and scaling |

score | Compute credit scores for given data |

probdefault | Likelihood of default for given data set |

validatemodel | Validate quality of credit scorecard model |

compact | Create compact credit scorecard |

Examples

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011).

load CreditCardData

sc = creditscorecard(data)sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustID' 'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: ''

PredictorVars: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

Use the CreditCardData.mat file to load the data (dataWeights) that contains a column (RowWeights) for the weights (using a dataset from Refaat 2011).

load CreditCardDataCreate a creditscorecard object using the optional name-value pair argument for 'WeightsVar'.

sc = creditscorecard(dataWeights,'WeightsVar','RowWeights')

sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: 'RowWeights'

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'RowWeights' 'status'}

NumericPredictors: {'CustID' 'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: ''

PredictorVars: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×12 table]

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011).

load CreditCardData

sc = creditscorecard(data)sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustID' 'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: ''

PredictorVars: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

To display the creditscorecard object properties, use dot notation.

sc.PredictorVars

ans = 1×10 cell

{'CustID'} {'CustAge'} {'TmAtAddress'} {'ResStatus'} {'EmpStatus'} {'CustIncome'} {'TmWBank'} {'OtherCC'} {'AMBalance'} {'UtilRate'}

sc.VarNames

ans = 1×11 cell

{'CustID'} {'CustAge'} {'TmAtAddress'} {'ResStatus'} {'EmpStatus'} {'CustIncome'} {'TmWBank'} {'OtherCC'} {'AMBalance'} {'UtilRate'} {'status'}

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011).

load CreditCardData

sc = creditscorecard(data)sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustID' 'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: ''

PredictorVars: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

Since the IDVar property has public access, you can change its value at the command line.

sc.IDVar = 'CustID'sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: 'CustID'

PredictorVars: {'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011).

load CreditCardData

sc = creditscorecard(data)sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustID' 'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: ''

PredictorVars: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

In this example, the default values for the properties ResponseVar, PredictorVars and GoodLabel are assigned when this object is created. By default, the property ResponseVar is set to the variable name that is in the last column of the input data ('status' in this example). The property PredictorVars contains the names of all the variables that are in VarNames, but excludes IDVar and ResponseVar. Also, by default in the previous example, GoodLabel is set to 0, since it is the value in the response variable (ResponseVar) with the highest count.

Display the creditscorecard object properties using dot notation.

sc.PredictorVars

ans = 1×10 cell

{'CustID'} {'CustAge'} {'TmAtAddress'} {'ResStatus'} {'EmpStatus'} {'CustIncome'} {'TmWBank'} {'OtherCC'} {'AMBalance'} {'UtilRate'}

sc.VarNames

ans = 1×11 cell

{'CustID'} {'CustAge'} {'TmAtAddress'} {'ResStatus'} {'EmpStatus'} {'CustIncome'} {'TmWBank'} {'OtherCC'} {'AMBalance'} {'UtilRate'} {'status'}

Since IDVar and PredictorVars have public access, you can change their values at the command line.

sc.IDVar = 'CustID'sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: 'CustID'

PredictorVars: {'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

sc.PredictorVars = {'CustIncome','ResStatus','AMBalance'}sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustIncome' 'AMBalance'}

CategoricalPredictors: {'ResStatus'}

BinMissingData: 0

IDVar: 'CustID'

PredictorVars: {'ResStatus' 'CustIncome' 'AMBalance'}

Data: [1200×11 table]

disp(sc)

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustIncome' 'AMBalance'}

CategoricalPredictors: {'ResStatus'}

BinMissingData: 0

IDVar: 'CustID'

PredictorVars: {'ResStatus' 'CustIncome' 'AMBalance'}

Data: [1200×11 table]

Create a creditscorecard object using the CreditCardData.mat file to load the data (using a dataset from Refaat 2011). Then use name-value pair arguments for creditscorecard to define GoodLabel and ResponseVar.

load CreditCardData sc = creditscorecard(data,'IDVar','CustID','GoodLabel',0,'ResponseVar','status')

sc =

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 0

IDVar: 'CustID'

PredictorVars: {'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

GoodLabel and ResponseVar can only be set (enforced) when creating a creditscorecard object using creditscorecard.

Create a creditscorecard object using the CreditCardData.mat file to load the dataMissing with missing values.

load CreditCardData

head(dataMissing,5) CustID CustAge TmAtAddress ResStatus EmpStatus CustIncome TmWBank OtherCC AMBalance UtilRate status

______ _______ ___________ ___________ _________ __________ _______ _______ _________ ________ ______

1 53 62 <undefined> Unknown 50000 55 Yes 1055.9 0.22 0

2 61 22 Home Owner Employed 52000 25 Yes 1161.6 0.24 0

3 47 30 Tenant Employed 37000 61 No 877.23 0.29 0

4 NaN 75 Home Owner Employed 53000 20 Yes 157.37 0.08 0

5 68 56 Home Owner Employed 53000 14 Yes 561.84 0.11 0

fprintf('Number of rows: %d\n',height(dataMissing))Number of rows: 1200

fprintf('Number of missing values CustAge: %d\n',sum(ismissing(dataMissing.CustAge)))Number of missing values CustAge: 30

fprintf('Number of missing values ResStatus: %d\n',sum(ismissing(dataMissing.ResStatus)))Number of missing values ResStatus: 40

Use creditscorecard with the name-value argument 'BinMissingData' set to true to bin the missing data in a separate bin.

sc = creditscorecard(dataMissing,'IDVar','CustID','BinMissingData',true); sc = autobinning(sc); disp(sc)

creditscorecard with properties:

GoodLabel: 0

ResponseVar: 'status'

WeightsVar: ''

VarNames: {'CustID' 'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate' 'status'}

NumericPredictors: {'CustAge' 'TmAtAddress' 'CustIncome' 'TmWBank' 'AMBalance' 'UtilRate'}

CategoricalPredictors: {'ResStatus' 'EmpStatus' 'OtherCC'}

BinMissingData: 1

IDVar: 'CustID'

PredictorVars: {'CustAge' 'TmAtAddress' 'ResStatus' 'EmpStatus' 'CustIncome' 'TmWBank' 'OtherCC' 'AMBalance' 'UtilRate'}

Data: [1200×11 table]

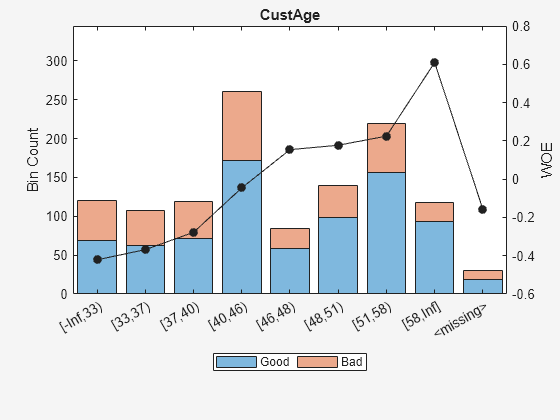

Display bin information for numeric data for 'CustAge' that includes missing data in a separate bin labelled <missing>.

bi = bininfo(sc,'CustAge');

disp(bi) Bin Good Bad Odds WOE InfoValue

_____________ ____ ___ ______ ________ __________

{'[-Inf,33)'} 69 52 1.3269 -0.42156 0.018993

{'[33,37)' } 63 45 1.4 -0.36795 0.012839

{'[37,40)' } 72 47 1.5319 -0.2779 0.0079824

{'[40,46)' } 172 89 1.9326 -0.04556 0.0004549

{'[46,48)' } 59 25 2.36 0.15424 0.0016199

{'[48,51)' } 99 41 2.4146 0.17713 0.0035449

{'[51,58)' } 157 62 2.5323 0.22469 0.0088407

{'[58,Inf]' } 93 25 3.72 0.60931 0.032198

{'<missing>'} 19 11 1.7273 -0.15787 0.00063885

{'Totals' } 803 397 2.0227 NaN 0.087112

plotbins(sc,'CustAge')

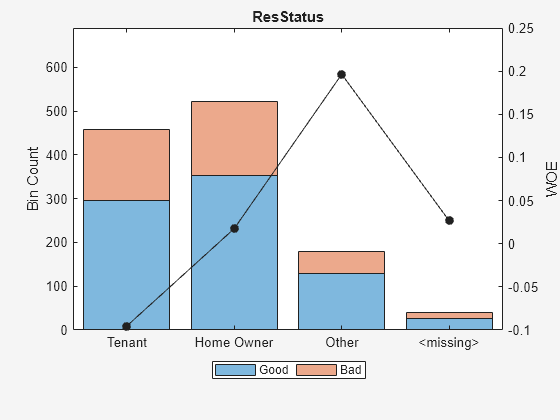

Display bin information for categorical data for 'ResStatus' that includes missing data in a separate bin labelled <missing>.

bi = bininfo(sc,'ResStatus');

disp(bi) Bin Good Bad Odds WOE InfoValue

______________ ____ ___ ______ _________ __________

{'Tenant' } 296 161 1.8385 -0.095463 0.0035249

{'Home Owner'} 352 171 2.0585 0.017549 0.00013382

{'Other' } 128 52 2.4615 0.19637 0.0055808

{'<missing>' } 27 13 2.0769 0.026469 2.3248e-05

{'Totals' } 803 397 2.0227 NaN 0.0092627

plotbins(sc,'ResStatus')

References

[1] Anderson, R. The Credit Scoring Toolkit. Oxford University Press, 2007.

[2] Refaat, M. Data Preparation for Data Mining Using SAS. Morgan Kaufmann, 2006.

[3] Refaat, M. Credit Risk Scorecards: Development and Implementation Using SAS. lulu.com, 2011.

Version History

Introduced in R2014b

See Also

Functions

screenpredictors(Risk Management Toolbox) |autobinning|modifybins|bindata|bininfo|fillmissing|predictorinfo|modifypredictor|plotbins|fitmodel|fitConstrainedModel|displaypoints|formatpoints|score|setmodel|validatemodel|probdefault|table

Apps

- Binning Explorer (Risk Management Toolbox)

Topics

- Case Study for Credit Scorecard Analysis

- Credit Scorecards with Constrained Logistic Regression Coefficients

- Credit Scorecard Modeling with Missing Values

- Credit Scoring Using Logistic Regression and Decision Trees (Risk Management Toolbox)

- Use Reject Inference Techniques with Credit Scorecards (Risk Management Toolbox)

- compactCreditScorecard Object Workflow (Risk Management Toolbox)

- Troubleshooting Credit Scorecard Results

- Bin Data to Create Credit Scorecards Using Binning Explorer (Risk Management Toolbox)

- Explore Fairness Metrics for Credit Scoring Model (Risk Management Toolbox)

- Bias Mitigation in Credit Scoring by Reweighting (Risk Management Toolbox)

- Bias Mitigation in Credit Scoring by Disparate Impact Removal (Risk Management Toolbox)

- Interpretability and Explainability for Credit Scoring (Risk Management Toolbox)

- Credit Scorecard Modeling Workflow

- About Credit Scorecards

- Credit Scorecard Modeling Using Observation Weights

- Overview of Binning Explorer (Risk Management Toolbox)