portsim

Monte Carlo simulation of correlated asset returns

Syntax

Description

RetSeries = portsim(ExpReturn,ExpCovariance,NumObs)NASSETS assets over

NUMOBS consecutive observation intervals. Asset returns are simulated

as the proportional increments of constant drift, constant volatility stochastic

processes, thereby approximating continuous-time geometric Brownian motion.

Note

An alternative for portfolio optimization is to use the Portfolio object for mean-variance portfolio optimization. This object

supports gross or net portfolio returns as the return proxy, the variance of portfolio

returns as the risk proxy, and a portfolio set that is any combination of the

specified constraints to form a portfolio set. For information on the workflow when

using Portfolio objects, see Portfolio Object Workflow.

RetSeries = portsim(___,RetIntervals,NumSim,Method)

Examples

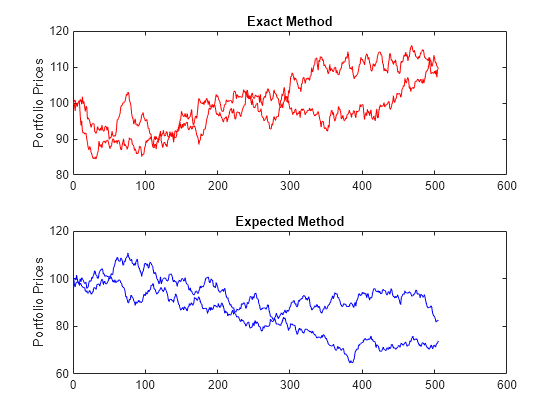

This example shows the distinction between the Exact and Expected methods of simulation.

Consider a portfolio of five assets with the following expected returns, standard deviations, and correlation matrix based on daily asset returns (where ExpReturn and Sigmas are divided by 100 to convert percentages to returns).

ExpReturn = [0.0246 0.0189 0.0273 0.0141 0.0311]/100;

Sigmas = [0.9509 1.4259 1.5227 1.1062 1.0877]/100;

Correlations = [1.0000 0.4403 0.4735 0.4334 0.6855

0.4403 1.0000 0.7597 0.7809 0.4343

0.4735 0.7597 1.0000 0.6978 0.4926

0.4334 0.7809 0.6978 1.0000 0.4289

0.6855 0.4343 0.4926 0.4289 1.0000];Convert the correlations and standard deviations to a covariance matrix.

ExpCovariance = corr2cov(Sigmas, Correlations)

ExpCovariance = 5×5

10-3 ×

0.0904 0.0597 0.0686 0.0456 0.0709

0.0597 0.2033 0.1649 0.1232 0.0674

0.0686 0.1649 0.2319 0.1175 0.0816

0.0456 0.1232 0.1175 0.1224 0.0516

0.0709 0.0674 0.0816 0.0516 0.1183

Assume that there are 252 trading days in a calendar year, and simulate two sample paths (realizations) of daily returns over a two-year period. Since ExpReturn and ExpCovariance are expressed daily, set RetIntervals = 1.

StartPrice = 100; NumObs = 504; % two calendar years of daily returns NumSim = 2; RetIntervals = 1; % one trading day NumAssets = 5;

To illustrate the distinction between methods, simulate two paths by each method, starting with the same random number state.

rng('default'); RetExact = portsim(ExpReturn, ExpCovariance, NumObs, ... RetIntervals, NumSim, 'Exact'); rng(0); RetExpected = portsim(ExpReturn, ExpCovariance, NumObs, ... RetIntervals, NumSim, 'Expected');

Compare the mean and covariance of RetExact with the inputs (ExpReturn and ExpCovariance), you will observe that they are almost identical.

At this point, RetExact and RetExpected are both 504-by-5-by-2 arrays. Now assume an equally weighted portfolio formed from the five assets and create arrays of portfolio returns in which each column represents the portfolio return of the corresponding sample path of the simulated returns of the five assets. The portfolio arrays PortRetExact and PortRetExpected are 504-by-2 matrices.

Weights = ones(NumAssets, 1)/NumAssets; PortRetExact = zeros(NumObs, NumSim); PortRetExpected = zeros(NumObs, NumSim); for i = 1:NumSim PortRetExact(:,i) = RetExact(:,:,i) * Weights; PortRetExpected(:,i) = RetExpected(:,:,i) * Weights; end

Finally, convert the simulated portfolio returns to prices and plot the data. In particular, note that since the Exact method matches expected return and covariance, the terminal portfolio prices are virtually identical for each sample path. This is not true for the Expected simulation method. Although this example examines portfolios, the same methods apply to individual assets as well. Thus, Exact simulation is most appropriate when unique paths are required to reach the same terminal prices.

PortExact = ret2tick(PortRetExact, ... repmat(StartPrice,1,NumSim)); PortExpected = ret2tick(PortRetExpected, ... repmat(StartPrice,1,NumSim)); subplot(2,1,1), plot(PortExact, '-r') ylabel('Portfolio Prices') title('Exact Method') subplot(2,1,2), plot(PortExpected, '-b') ylabel('Portfolio Prices') title('Expected Method')

This example shows the interplay among ExpReturn,

ExpCovariance, and RetIntervals. Recall that

portsim simulates correlated asset returns over an interval of length

dt, given by the equation

where S is the asset price, μ is the expected rate of return, σ is the volatility of the asset price, and ε represents a random drawing from a standardized normal distribution.

The time increment dt is determined by the optional input

RetIntervals, either as an explicit input argument or as a unit time

increment by default. Regardless, the periodicity of ExpReturn,

ExpCovariance, and RetIntervals must be

consistent. For example, if ExpReturn and

ExpCovariance are annualized, then RetIntervals

must be in years. This point is often misunderstood.

To illustrate the interplay among ExpReturn,

ExpCovariance, and RetIntervals, consider a

portfolio of five assets with the following expected returns, standard deviations, and

correlation matrix based on daily asset returns.

ExpReturn = [0.0246 0.0189 0.0273 0.0141 0.0311]/100;

Sigmas = [0.9509 1.4259 1.5227 1.1062 1.0877]/100;

Correlations = [1.0000 0.4403 0.4735 0.4334 0.6855

0.4403 1.0000 0.7597 0.7809 0.4343

0.4735 0.7597 1.0000 0.6978 0.4926

0.4334 0.7809 0.6978 1.0000 0.4289

0.6855 0.4343 0.4926 0.4289 1.0000];

Convert the correlations and standard deviations to a covariance matrix of daily returns.

ExpCovariance = corr2cov(Sigmas, Correlations);

Assume 252 trading days per calendar year, and simulate a single sample path of

daily returns over a four-year period. Since the ExpReturn and

ExpCovariance inputs are expressed daily, set

RetIntervals = 1.

StartPrice = 100; NumObs = 1008; % four calendar years of daily returns RetIntervals = 1; % one trading day NumAssets = length(ExpReturn); randn('state',0); RetSeries1 = portsim(ExpReturn, ExpCovariance, NumObs, ... RetIntervals, 1, 'Expected');

Now annualize the daily data, thereby changing the periodicity of the data, by

multiplying ExpReturn and ExpCovariance by 252 and

dividing RetIntervals by 252 (RetIntervals = 1/252

of a year). Resetting the random number generator to its initial state, you can

reproduce the results.

rng('default'); RetSeries2 = portsim(ExpReturn*252, ExpCovariance*252, ... NumObs, RetIntervals/252, 1, 'Expected');

Assume an equally weighted portfolio and compute portfolio returns associated with each simulated return series.

Weights = ones(NumAssets, 1)/NumAssets; PortRet1 = RetSeries2 * Weights; PortRet2 = RetSeries2 * Weights;

Comparison of the data reveals that PortRet1 and

PortRet2 are identical.

This example shows how to simulate a univariate geometric Brownian motion process. It is based on an example found in Hull, Options, Futures, and Other Derivatives, 5th Edition (see example 12.2 on page 236). In addition to verifying Hull's example, it also graphically illustrates the lognormal property of terminal stock prices by a rather large Monte Carlo simulation.

Assume that you own a stock with an initial price of $20, an annualized expected return of 20% and volatility of 40%. Simulate the daily price process for this stock over the course of one full calendar year (252 trading days).

StartPrice = 20; ExpReturn = 0.2; ExpCovariance = 0.4^2; NumObs = 252; NumSim = 10000; RetIntervals = 1/252;

RetIntervals is expressed in years, consistent with the fact that

ExpReturn and ExpCovariance are annualized.

Also, ExpCovariance is entered as a variance rather than the more

familiar standard deviation (volatility).

Set the random number generator state, and simulate 10,000 trials (realizations) of stock returns over a full calendar year of 252 trading days.

rng('default'); RetSeries = squeeze(portsim(ExpReturn, ExpCovariance, NumObs, ... RetIntervals, NumSim, 'Expected'));

The squeeze function reformats the output array of simulated

returns from a

252-by-1-by-10000 array to

more convenient 252-by-10000 array. (Recall that

portsim is fundamentally a multivariate simulation engine).

In accordance with Hull's equations 12.4 and 12.5 on page 236

convert the simulated return series to a price series and compute the sample mean and the variance of the terminal stock prices.

StockPrices = ret2tick(RetSeries, repmat(StartPrice, 1, NumSim)); SampMean = mean(StockPrices(end,:)) SampVar = var(StockPrices(end,:))

SampMean = 24.4489 SampVar = 101.4243

Compare these values with the values you obtain by using Hull's equations.

ExpValue = StartPrice*exp(ExpReturn) ExpVar = ... StartPrice*StartPrice*exp(2*ExpReturn)*(exp((ExpCovariance)) - 1)

ExpValue = 24.4281 ExpVar = 103.5391

These results are very close to the results shown in Hull's example 12.2.

Display the sample density function of the terminal stock price after one calendar year. From the sample density function, the lognormal distribution of terminal stock prices is apparent.

[count, BinCenter] = hist(StockPrices(end,:), 30); figure bar(BinCenter, count/sum(count), 1, 'r') xlabel('Terminal Stock Price') ylabel('Probability') title('Lognormal Terminal Stock Prices')

Input Arguments

Output Arguments

References

[1] Hull, J. C. Options, Futures, and Other Derivatives. Prentice-Hall, 2003.

Version History

Introduced before R2006a