Portfolio

创建 Portfolio 对象以进行均值-方差投资组合优化和分析

说明

使用 Portfolio 函数创建一个 Portfolio 对象,用于均值-方差投资组合优化。

投资组合优化的主要工作流是创建一个 Portfolio 对象实例来完整指定一个投资组合优化问题,并使用支持的函数对 Portfolio 对象进行运算,以求取和分析有效投资组合。有关此工作流的详细信息,请参阅 Portfolio 对象工作流。

您可通过几种方式使用 Portfolio 对象。要使用 Portfolio 对象创建投资组合优化问题,最简单的语法是:

p = Portfolio;

Portfolio 对象 p,其中所有对象属性都为空。 Portfolio 对象也接受用一系列名称-值对组参量指定属性及其值。Portfolio 对象接受采用以下一般语法的输入作为属性:

p = Portfolio('property1',value1,'property2',value2, ... );如果已有 Portfolio 对象,则该语法允许且仅允许 Portfolio 对象的第一个参量为已有对象,后续名称-值对组参量则表示要添加或修改的属性。例如,假定已有 Portfolio 对象 p,一般语法为:

p = Portfolio(p,'property1',value1,'property2',value2, ... );

输入参量名称不区分大小写,但必须完整指定。此外,部分属性可采用简写参量名称指定(请参阅 简写属性名称)。Portfolio 对象会尝试从输入中检测问题的维度,一旦确定,则对后续输入进行各种标量或矩阵扩展运算,从而简化构建问题的整个过程。此外,Portfolio 对象是值对象,因此,假定有投资组合 p,则以下代码将创建一个不同于 p 的新对象 q:

q = Portfolio(p, ...)

创建 Portfolio 对象后,您可以使用关联的对象函数来设置投资组合约束,分析有效边界并验证投资组合模型。

有关均值-方差优化理论基础的详细信息,请参阅 投资组合优化理论。

创建对象

描述

p = PortfolioPortfolio 对象,用于均值-方差投资组合优化和分析。然后,您可以使用支持的 "add" 和 "set" 函数将元素添加到 Portfolio 对象。有关详细信息,请参阅创建 Portfolio 对象。

输入参量

输出参量

属性

对象函数

setAssetList | Set up list of identifiers for assets |

setInitPort | Set up initial or current portfolio |

setDefaultConstraints | 使用总和为 1 的非负权重设置投资组合约束 |

getAssetMoments | 从 Portfolio 对象获取资产收益的均值和协方差 |

setAssetMoments | 设置 Portfolio 对象资产收益的矩(均值和协方差) |

estimateAssetMoments | Estimate mean and covariance of asset returns from data |

setCosts | Set up proportional transaction costs for portfolio |

addEquality | Add linear equality constraints for portfolio weights to existing constraints |

addGroupRatio | Add group ratio constraints for portfolio weights to existing group ratio constraints |

addGroups | Add group constraints for portfolio weights to existing group constraints |

addInequality | Add linear inequality constraints for portfolio weights to existing constraints |

getBounds | Obtain bounds for portfolio weights from portfolio object |

getBudget | Obtain budget constraint bounds from portfolio object |

getCosts | Obtain buy and sell transaction costs from portfolio object |

getEquality | Obtain equality constraint arrays from portfolio object |

getGroupRatio | Obtain group ratio constraint arrays from portfolio object |

getGroups | Obtain group constraint arrays from portfolio object |

getInequality | Obtain inequality constraint arrays from portfolio object |

getOneWayTurnover | Obtain one-way turnover constraints from portfolio object |

setGroups | Set up group constraints for portfolio weights |

setInequality | Set up linear inequality constraints for portfolio weights |

setBounds | Set up bounds for portfolio weights for portfolio |

setBudget | Set up budget constraints for portfolio |

setConditionalBudget | Set up conditional budget constraints for portfolio |

setCosts | Set up proportional transaction costs for portfolio |

setEquality | Set up linear equality constraints for portfolio weights |

setGroupRatio | Set up group ratio constraints for portfolio weights |

setOneWayTurnover | Set up one-way portfolio turnover constraints |

setTurnover | Set up maximum portfolio turnover constraint |

setTrackingPort | Set up benchmark portfolio for tracking error constraint |

setTrackingError | Set up maximum portfolio tracking error constraint |

setMinMaxNumAssets | Set cardinality constraints on the number of assets invested in a portfolio |

checkFeasibility | Check feasibility of input portfolios against portfolio object |

estimateBounds | Estimate global lower and upper bounds for set of portfolios |

estimateFrontier | 估计有效边界上指定数量的最优投资组合 |

estimateFrontierByReturn | Estimate optimal portfolios with targeted portfolio returns |

estimateFrontierByRisk | Estimate optimal portfolios with targeted portfolio risks |

estimateFrontierLimits | Estimate optimal portfolios at endpoints of efficient frontier |

plotFrontier | 绘制有效边界 |

estimateMaxSharpeRatio | 估计有效投资组合以最大化 Portfolio 对象的夏普比率 |

estimatePortMoments | 估计 Portfolio 对象的投资组合收益矩 |

estimatePortReturn | 估计投资组合收益均值 |

estimatePortRisk | Estimate portfolio risk according to risk proxy associated with corresponding object |

estimateCustomObjectivePortfolio | Estimate optimal portfolio for user-defined objective function for

Portfolio object |

setSolver | Choose main solver and specify associated solver options for portfolio optimization |

setSolverMINLP | Choose mixed integer nonlinear programming (MINLP) solver for portfolio optimization |

示例

您可以创建一个不带输入参量的 Portfolio 对象 p,并使用 disp 显示该对象。

p = Portfolio; disp(p);

Portfolio with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

AssetMean: []

AssetCovar: []

TrackingError: []

TrackingPort: []

Turnover: []

BuyTurnover: []

SellTurnover: []

Name: []

NumAssets: []

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: []

UpperBound: []

LowerBudget: []

UpperBudget: []

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

借助此方法,您可以使用 Portfolio 函数创建投资组合优化问题。然后,您可以使用相关的 set 函数来设置和修改 Portfolio 对象中的一系列属性。

您可以用变量 m 和 C 指定资产收益的均值和协方差,直接使用 Portfolio 对象来创建“标准”投资组合优化问题。

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('assetmean', m, 'assetcovar', C, ...

'lowerbudget', 1, 'upperbudget', 1, 'lowerbound', 0)p =

Portfolio with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

AssetMean: [4×1 double]

AssetCovar: [4×4 double]

TrackingError: []

TrackingPort: []

Turnover: []

BuyTurnover: []

SellTurnover: []

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

请注意,LowerBound 属性值进行标量扩展,因为 AssetMean 和 AssetCovar 提供问题的维度。

您也可以用变量 m 和 C 指定资产收益的均值和协方差(这也表明参量名称不区分大小写),采用多步设置来创建同样的“标准”投资组合优化问题。

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

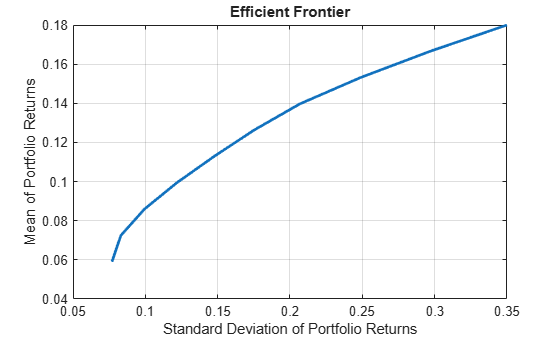

p = Portfolio;

p = Portfolio(p, 'assetmean', m, 'assetcovar', C);

p = Portfolio(p, 'lowerbudget', 1, 'upperbudget', 1);

p = Portfolio(p, 'lowerbound', 0);

plotFrontier(p);

这种方法之所以有效,是因为对 Portfolio 的调用是按此特定顺序进行的。在本例中,初始化 AssetMean 和 AssetCovar 的那次调用确定了问题的维度。如果您最后执行这次调用,则必须显式设置 LowerBound 属性的维度,如下所示:

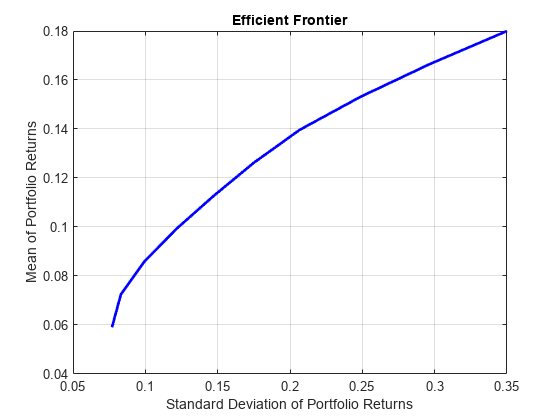

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio;

p = Portfolio(p, 'LowerBound', zeros(size(m)));

p = Portfolio(p, 'LowerBudget', 1, 'UpperBudget', 1);

p = Portfolio(p, 'AssetMean', m, 'AssetCovar', C);

plotFrontier(p);

如果未指定 LowerBound 的大小,而是输入标量参量,则 Portfolio 对象假设您正在定义单资产问题,并在设置包含四个资产的资产矩的调用中产生错误。

使用 Portfolio 创建 Portfolio 对象 p 时,您可以使用简写属性名称。

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('mean', m, 'covar', C, 'budget', 1, 'lb', 0)p =

Portfolio with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

AssetMean: [4×1 double]

AssetCovar: [4×4 double]

TrackingError: []

TrackingPort: []

Turnover: []

BuyTurnover: []

SellTurnover: []

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

虽然不推荐,但您可以直接设置属性,然而系统不会对输入进行错误检查。

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio;

p.NumAssets = numel(m);

p.AssetMean = m;

p.AssetCovar = C;

p.LowerBudget = 1;

p.UpperBudget = 1;

p.LowerBound = zeros(size(m));

disp(p) Portfolio with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

AssetMean: [4×1 double]

AssetCovar: [4×4 double]

TrackingError: []

TrackingPort: []

Turnover: []

BuyTurnover: []

SellTurnover: []

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

创建有效投资组合:

load CAPMuniverse p = Portfolio('AssetList',Assets(1:12)); p = estimateAssetMoments(p, Data(:,1:12),'missingdata',true); p = setDefaultConstraints(p); plotFrontier(p);

pwgt = estimateFrontier(p, 5); pnames = cell(1,5); for i = 1:5 pnames{i} = sprintf('Port%d',i); end Blotter = dataset([{pwgt},pnames],'obsnames',p.AssetList); disp(Blotter);

Port1 Port2 Port3 Port4 Port5

AAPL 0.017926 0.058247 0.097816 0.12955 0

AMZN 1.782e-13 1.5832e-11 2.1265e-10 2.0669e-11 0

CSCO 1.3365e-14 7.4305e-13 5.1756e-11 2.798e-12 0

DELL 0.0041906 4.0213e-10 2.9535e-09 1.0249e-10 0

EBAY 1.2686e-14 1.6093e-12 1.0334e-10 1.0811e-11 0

GOOG 0.16144 0.35678 0.55228 0.75116 1

HPQ 0.052566 0.032302 0.011186 6.1882e-09 0

IBM 0.46422 0.36045 0.25577 0.11928 0

INTC 4.5883e-14 2.0534e-11 3.845e-08 1.8432e-08 0

MSFT 0.29966 0.19222 0.082949 1.7512e-09 0

ORCL 1.9196e-14 1.5317e-12 1.0064e-10 7.6664e-12 0

YHOO 5.4342e-15 1.1905e-13 1.3146e-11 3.7126e-13 0

此示例说明如何求解具有选定资产数量或条件(半连续)边界约束的均值方差投资组合优化问题。若要求解此问题,您可以使用 Portfolio 对象以及不同的混合整数非线性规划 (MINLP) 求解器。

均值-方差投资组合

加载 CAPMuniverse.mat 中的收益数据。然后,使用默认约束创建一个权重总和为 1 的纯多头投资组合均值方差 Portfolio 对象。对于此示例,您可以将权重 的可行域定义为

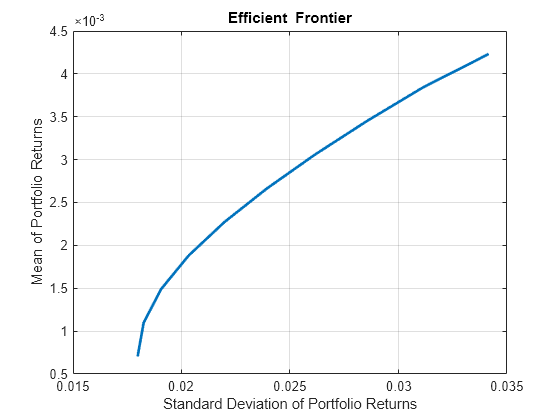

% Load data load CAPMuniverse.mat % Create a mean-variance Portfolio object with default constraints. p = Portfolio(AssetList=Assets(1:12)); p = estimateAssetMoments(p,Data(:,1:12)); p = setDefaultConstraints(p);

通过设置条件(半连续)边界来包含此场景的二元变量。条件边界是指 或 这样的边界。在此示例中,所有资产的边界为 。

% Set conditional bounds condLB = 0.1; condUB = 0.5; p = setBounds(p,condLB,condUB,BoundType="conditional");

使用 estimateFrontier 估计有效边界上的一组投资组合。有效边界是一条曲线,该曲线显示帕累托最优投资组合实现的收益和风险之间的平衡。对于给定的收益水平,有效边界上的投资组合是指在保持期望收益的同时将风险降至最低的投资组合。与之相对,对于给定的风险水平,有效边界上的投资组合是指在保持预期风险水平的同时最大化收益的投资组合。

% Compute the efficient frontier.

pwgt = estimateFrontier(p)pwgt = 12×10

0 0 0.1000 0.1253 0.1745 0.2236 0.2715 0.3327 0.4111 0.5000

0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

0.1350 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

0.1000 0.1450 0.1406 0.1910 0.2344 0.2778 0.3200 0.3726 0.4415 0.5000

0.1000 0.1609 0.1642 0.2121 0.2415 0.2709 0.3085 0.2947 0.1474 0

0.2354 0.1875 0.1290 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

0.4296 0.4066 0.3662 0.3717 0.2496 0.1277 0 0 0 0

0 0.1000 0.1000 0.1000 0.1000 0.1000 0.1000 0 0 0

0 0 0 0 0 0 0 0 0 0

% Compute risk and returns of the portfolios on the efficient frontier.

[rsk,ret] = estimatePortMoments(p,pwgt)rsk = 10×1

0.0076

0.0080

0.0085

0.0094

0.0105

0.0117

0.0132

0.0147

0.0168

0.0193

ret = 10×1

0.0008

0.0012

0.0017

0.0021

0.0026

0.0030

0.0034

0.0039

0.0043

0.0048

使用 plotFrontier 根据边界估计值绘制权重。生成的曲线呈分段凹形,凹区间之间有垂直跳跃(不连续性)。

% Plot the efficient frontier.

plotFrontier(p,pwgt)

更改 MINLP 求解器

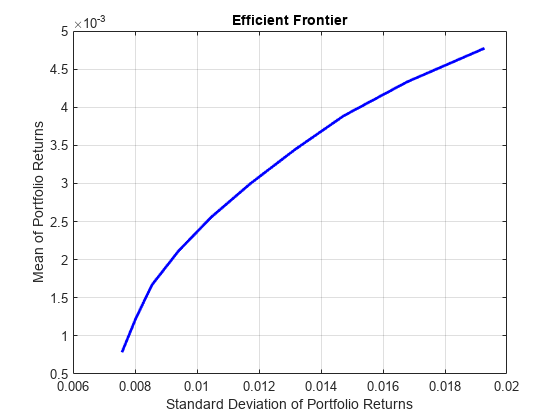

在上一部分,您使用了 estimateFrontier 的默认求解器。但其实您可以使用 setSolverMINLP 支持的下面三种算法中的任意一种来求解混合整数投资组合问题:OuterApproximation、ExtendedCP 和 TrustRegionCP。此外,OuterApproximation 算法在求解 Portfolio 问题时还接受一个额外的名称-值参量 (ExtendedFormulation),可以重新表述问题的二次函数形式,从而能够在扩展空间中进行处理,这通常会减少计算时间。包括 OuterApproximation 算法的扩展公式变体在内的所有算法,都会在数值精度范围内返回相同的值。可用的求解器包括:

OuterApproximation- 默认算法,该算法非常稳健,通常比ExtenedCP速度更快OuterApproximation,其中ExtendedFormulation设置为true- 一种稳健的算法,通常比其他算法更快,但仅支持求解Portfolio对象问题ExtendedCP- 该求解器稳健性最佳,但通常速度最慢TrustRegionCP- 该算法速度最快,但稳健性较差,可能提供次优解

有关混合整数投资组合问题求解器的详细信息,请参阅Choose MINLP Solvers for Portfolio Problems。

若要更改 MINLP 求解器,请使用 setSolverMINLP。

% Select the extended formulation version of 'OuterApproximation' as the % solver. p_EOA = setSolverMINLP(p,'OuterApproximation',... ExtendedFormulation=true); pwgt_EOA = estimateFrontier(p_EOA); [rskEOA,retEOA] = estimatePortMoments(p_EOA,pwgt_EOA); % Select 'TrustRegionCP' as the solver. p_TR = setSolverMINLP(p,'TrustRegionCP'); pwgt_TR = estimateFrontier(p_TR); [rskTR,retTR] = estimatePortMoments(p_TR,pwgt_TR); % Select 'ExtendedCP' as the solver using 'midway' cuts as 'CutGeneration'. p_ECP = setSolverMINLP(p,'ExtendedCP','CutGeneration','midway'); pwgt_ECP = estimateFrontier(p_ECP); [rskECP,retECP] = estimatePortMoments(p_ECP,pwgt_ECP);

比较使用不同的求解器得到的有效边界上的投资组合收益和风险。它们在数值精度内是相同的,其中绝对误差 。

retTable = table(ret,retEOA,retTR,retECP,... 'VariableNames',{'OA','EOA','TR','ECP'})

retTable=10×4 table

OA EOA TR ECP

__________ __________ __________ __________

0.00078336 0.00078336 0.00078336 0.00078344

0.0012267 0.0012267 0.0012267 0.0012267

0.00167 0.00167 0.00167 0.00167

0.0021133 0.0021133 0.0021133 0.0021133

0.0025566 0.0025566 0.0025566 0.0025566

0.0029999 0.0029999 0.0029999 0.0029999

0.0034432 0.0034432 0.0034432 0.0034432

0.0038865 0.0038865 0.0038865 0.0038865

0.0043298 0.0043298 0.0043298 0.0043298

0.0047731 0.0047731 0.0047731 0.0047731

rskTable = table(rsk,rskEOA,rskTR,rskECP,... 'VariableNames',{'OA','EOA','TR','ECP'})

rskTable=10×4 table

OA EOA TR ECP

_________ _________ _________ _________

0.0075778 0.0075778 0.0075778 0.0075778

0.0080234 0.0080234 0.0080235 0.0080235

0.0085488 0.0085488 0.0086052 0.0085489

0.0094024 0.0094024 0.0094051 0.0094025

0.010456 0.010456 0.010456 0.010456

0.011727 0.011727 0.011776 0.011728

0.013155 0.013155 0.013155 0.013155

0.014729 0.014729 0.014729 0.014729

0.016764 0.016764 0.016764 0.016764

0.019273 0.019273 0.019273 0.019273

% Compare the risks from the different OuterApproximation formulations.

norm(rskTable.OA-rskTable.EOA,Inf) <= 1e-4ans = logical

1

详细信息

参考

[1] For a complete list of references for the Portfolio object, see Portfolio Optimization.

版本历史记录

在 R2011a 中推出另请参阅

plotFrontier | estimateFrontier | PortfolioCVaR | PortfolioMAD | nearcorr | covarianceShrinkage | covarianceDenoising

主题

- 创建 Portfolio 对象

- Working with Portfolio Constraints Using Defaults

- 估计 Portfolio 对象整个有效边界上的有效投资组合

- Estimate Efficient Frontiers for Portfolio Object

- Asset Allocation Case Study

- 使用 Financial Toolbox 的投资组合优化示例

- Portfolio Optimization with Semicontinuous and Cardinality Constraints

- Black-Litterman Portfolio Optimization Using Financial Toolbox

- Portfolio Optimization Using Factor Models

- Bond Portfolio Optimization Using Portfolio Object

- Use Extended Formulation of OuterApproximation Solver Type

- Single Period Goal-Based Wealth Management

- Dynamic Portfolio Allocation in Goal-Based Wealth Management for Multiple Time Periods

- Multiperiod Goal-Based Wealth Management Using Reinforcement Learning

- Adding Constraints to Satisfy UCITS Directive

- 投资组合优化理论

- Portfolio 对象工作流

- Portfolio Object Properties and Functions

- Working with Portfolio Objects

- Setting and Getting Properties

- Displaying Portfolio Objects

- Saving and Loading Portfolio Objects

- Estimating Efficient Portfolios and Frontiers

- Arrays of Portfolio Objects

- Subclassing Portfolio Objects

- Conventions for Representation of Data

- 使用 Portfolio 对象进行投资组合优化支持的约束

- Role of Convexity in Portfolio Problems

- When to Use Portfolio Objects Over Optimization Toolbox

- Solver Guidelines for Portfolio Objects

- Choosing and Controlling the Solver for Mean-Variance Portfolio Optimization

- Choose MINLP Solvers for Portfolio Problems