fitckernel

Fit binary Gaussian kernel classifier using random feature expansion

Syntax

Description

fitckernel trains or cross-validates a binary Gaussian

kernel classification model for nonlinear classification.

fitckernel is more practical for big data applications that

have large training sets but can also be applied to smaller data sets that fit in

memory.

fitckernel maps data in a low-dimensional space into a

high-dimensional space, then fits a linear model in the high-dimensional space by

minimizing the regularized objective function. Obtaining the linear model in the

high-dimensional space is equivalent to applying the Gaussian kernel to the model in the

low-dimensional space. Available linear classification models include regularized

support vector machine (SVM) and logistic regression models.

To train a nonlinear SVM model for binary classification of in-memory data, see

fitcsvm.

Mdl = fitckernel(X,Y)X and the corresponding class labels in

Y. The fitckernel function maps

the predictors in a low-dimensional space into a high-dimensional space, then

fits a binary SVM model to the transformed predictors and class labels. This

linear model is equivalent to the Gaussian kernel classification model in the

low-dimensional space.

Mdl = fitckernel(Tbl,ResponseVarName)Mdl trained using the

predictor variables contained in the table Tbl and the

class labels in Tbl.ResponseVarName.

Mdl = fitckernel(___,Name,Value)

[

also returns the hyperparameter optimization results when you specify

Mdl,FitInfo,HyperparameterOptimizationResults] = fitckernel(___)OptimizeHyperparameters.

[

also returns Mdl,FitInfo,AggregateOptimizationResults] = fitckernel(___)AggregateOptimizationResults, which contains

hyperparameter optimization results when you specify the

OptimizeHyperparameters and

HyperparameterOptimizationOptions name-value arguments.

You must also specify the ConstraintType and

ConstraintBounds options of

HyperparameterOptimizationOptions. You can use this

syntax to optimize on compact model size instead of cross-validation loss, and

to perform a set of multiple optimization problems that have the same options

but different constraint bounds.

Examples

Train a binary kernel classification model using SVM.

Load the ionosphere data set. This data set has 34 predictors and 351 binary responses for radar returns, either bad ('b') or good ('g').

load ionosphere

[n,p] = size(X)n = 351

p = 34

resp = unique(Y)

resp = 2×1 cell

{'b'}

{'g'}

Train a binary kernel classification model that identifies whether the radar return is bad ('b') or good ('g'). Extract a fit summary to determine how well the optimization algorithm fits the model to the data.

rng('default') % For reproducibility [Mdl,FitInfo] = fitckernel(X,Y)

Mdl =

ClassificationKernel

ResponseName: 'Y'

ClassNames: {'b' 'g'}

Learner: 'svm'

NumExpansionDimensions: 2048

KernelScale: 1

Lambda: 0.0028

BoxConstraint: 1

Properties, Methods

FitInfo = struct with fields:

Solver: 'LBFGS-fast'

LossFunction: 'hinge'

Lambda: 0.0028

BetaTolerance: 1.0000e-04

GradientTolerance: 1.0000e-06

ObjectiveValue: 0.2604

GradientMagnitude: 0.0028

RelativeChangeInBeta: 8.2512e-05

FitTime: 0.0670

History: []

Mdl is a ClassificationKernel model. To inspect the in-sample classification error, you can pass Mdl and the training data or new data to the loss function. Or, you can pass Mdl and new predictor data to the predict function to predict class labels for new observations. You can also pass Mdl and the training data to the resume function to continue training.

FitInfo is a structure array containing optimization information. Use FitInfo to determine whether optimization termination measurements are satisfactory.

For better accuracy, you can increase the maximum number of optimization iterations ('IterationLimit') and decrease the tolerance values ('BetaTolerance' and 'GradientTolerance') by using the name-value pair arguments. Doing so can improve measures like ObjectiveValue and RelativeChangeInBeta in FitInfo. You can also optimize model parameters by using the 'OptimizeHyperparameters' name-value pair argument.

Load the ionosphere data set. This data set has 34 predictors and 351 binary responses for radar returns, either bad ('b') or good ('g').

load ionosphere rng('default') % For reproducibility

Cross-validate a binary kernel classification model. By default, the software uses 10-fold cross-validation.

CVMdl = fitckernel(X,Y,'CrossVal','on')

CVMdl =

ClassificationPartitionedKernel

CrossValidatedModel: 'Kernel'

ResponseName: 'Y'

NumObservations: 351

KFold: 10

Partition: [1×1 cvpartition]

ClassNames: {'b' 'g'}

ScoreTransform: 'none'

Properties, Methods

numel(CVMdl.Trained)

ans = 10

CVMdl is a ClassificationPartitionedKernel model. Because fitckernel implements 10-fold cross-validation, CVMdl contains 10 ClassificationKernel models that the software trains on training-fold (in-fold) observations.

Estimate the cross-validated classification error.

kfoldLoss(CVMdl)

ans = 0.0940

The classification error rate is approximately 9%.

Optimize hyperparameters automatically using the OptimizeHyperparameters name-value argument.

Load the ionosphere data set. This data set has 34 predictors and 351 binary responses for radar returns, either bad ('b') or good ('g').

load ionosphereFind hyperparameters that minimize five-fold cross-validation loss by using automatic hyperparameter optimization. Specify OptimizeHyperparameters as 'auto' so that fitckernel finds optimal values of the KernelScale, Lambda, and Standardize name-value arguments. For reproducibility, set the random seed and use the 'expected-improvement-plus' acquisition function.

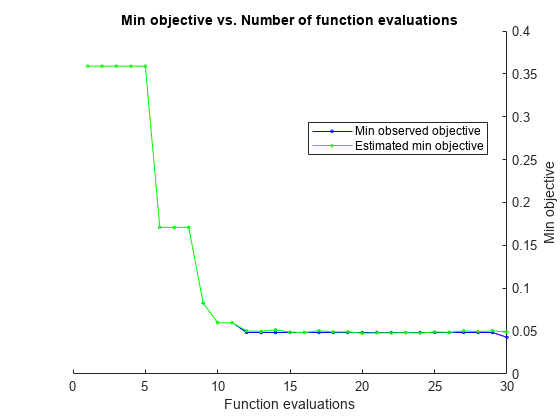

rng('default') [Mdl,FitInfo,HyperparameterOptimizationResults] = fitckernel(X,Y,'OptimizeHyperparameters','auto',... 'HyperparameterOptimizationOptions',struct('AcquisitionFunctionName','expected-improvement-plus'))

|====================================================================================================================|

| Iter | Eval | Objective | Objective | BestSoFar | BestSoFar | KernelScale | Lambda | Standardize |

| | result | | runtime | (observed) | (estim.) | | | |

|====================================================================================================================|

| 1 | Best | 0.35897 | 1.0989 | 0.35897 | 0.35897 | 3.8653 | 2.7394 | true |

| 2 | Accept | 0.35897 | 0.19983 | 0.35897 | 0.35897 | 429.99 | 0.0006775 | false |

| 3 | Accept | 0.35897 | 0.46283 | 0.35897 | 0.35897 | 0.11801 | 0.025493 | false |

| 4 | Accept | 0.41311 | 0.44156 | 0.35897 | 0.35898 | 0.0010694 | 9.1346e-06 | true |

| 5 | Accept | 0.4245 | 0.43444 | 0.35897 | 0.35898 | 0.0093918 | 2.8526e-06 | false |

| 6 | Best | 0.17094 | 0.32368 | 0.17094 | 0.17102 | 15.285 | 0.0038931 | false |

| 7 | Accept | 0.18234 | 0.31235 | 0.17094 | 0.17099 | 9.9078 | 0.0090818 | false |

| 8 | Accept | 0.35897 | 0.22198 | 0.17094 | 0.17097 | 26.961 | 0.46727 | false |

| 9 | Best | 0.082621 | 0.43261 | 0.082621 | 0.082677 | 7.7184 | 0.0025676 | false |

| 10 | Best | 0.059829 | 0.61709 | 0.059829 | 0.059839 | 5.6125 | 0.0013416 | false |

| 11 | Accept | 0.062678 | 0.62037 | 0.059829 | 0.059793 | 7.3294 | 0.00062394 | false |

| 12 | Best | 0.048433 | 0.93143 | 0.048433 | 0.050198 | 3.7772 | 0.00032964 | false |

| 13 | Accept | 0.051282 | 0.73324 | 0.048433 | 0.049662 | 3.4417 | 0.00077524 | false |

| 14 | Accept | 0.054131 | 0.73928 | 0.048433 | 0.051494 | 4.3694 | 0.00055199 | false |

| 15 | Accept | 0.051282 | 0.96946 | 0.048433 | 0.04872 | 1.7463 | 0.00012886 | false |

| 16 | Accept | 0.048433 | 0.71638 | 0.048433 | 0.048475 | 3.9086 | 3.1147e-05 | false |

| 17 | Accept | 0.054131 | 0.86538 | 0.048433 | 0.050325 | 3.1489 | 9.1315e-05 | false |

| 18 | Accept | 0.051282 | 0.65002 | 0.048433 | 0.049131 | 2.3414 | 4.8238e-06 | false |

| 19 | Accept | 0.062678 | 0.93699 | 0.048433 | 0.049062 | 7.2203 | 3.2694e-06 | false |

| 20 | Accept | 0.054131 | 0.56964 | 0.048433 | 0.051225 | 3.5381 | 1.0341e-05 | false |

|====================================================================================================================|

| Iter | Eval | Objective | Objective | BestSoFar | BestSoFar | KernelScale | Lambda | Standardize |

| | result | | runtime | (observed) | (estim.) | | | |

|====================================================================================================================|

| 21 | Accept | 0.068376 | 0.55637 | 0.048433 | 0.05111 | 1.4267 | 1.7614e-05 | false |

| 22 | Accept | 0.054131 | 0.72054 | 0.048433 | 0.05127 | 3.2173 | 2.9573e-06 | false |

| 23 | Accept | 0.05698 | 0.83249 | 0.048433 | 0.051187 | 2.4241 | 0.0003272 | false |

| 24 | Accept | 0.059829 | 0.96871 | 0.048433 | 0.051097 | 2.5948 | 4.5059e-05 | false |

| 25 | Accept | 0.059829 | 0.56318 | 0.048433 | 0.051018 | 7.2989 | 2.6908e-05 | false |

| 26 | Accept | 0.068376 | 1.0088 | 0.048433 | 0.048938 | 3.9585 | 6.9173e-06 | false |

| 27 | Accept | 0.05698 | 0.92743 | 0.048433 | 0.051222 | 4.2751 | 0.0002231 | false |

| 28 | Accept | 0.062678 | 0.44954 | 0.048433 | 0.051232 | 1.4533 | 2.8533e-06 | false |

| 29 | Accept | 0.051282 | 0.67025 | 0.048433 | 0.051122 | 3.8449 | 0.00059747 | false |

| 30 | Accept | 0.21083 | 0.92541 | 0.048433 | 0.0512 | 45.588 | 3.056e-06 | false |

__________________________________________________________

Optimization completed.

MaxObjectiveEvaluations of 30 reached.

Total function evaluations: 30

Total elapsed time: 26.8064 seconds

Total objective function evaluation time: 19.9001

Best observed feasible point:

KernelScale Lambda Standardize

___________ __________ ___________

3.7772 0.00032964 false

Observed objective function value = 0.048433

Estimated objective function value = 0.05162

Function evaluation time = 0.93143

Best estimated feasible point (according to models):

KernelScale Lambda Standardize

___________ __________ ___________

3.8449 0.00059747 false

Estimated objective function value = 0.0512

Estimated function evaluation time = 0.75141

Mdl =

ClassificationKernel

ResponseName: 'Y'

ClassNames: {'b' 'g'}

Learner: 'svm'

NumExpansionDimensions: 2048

KernelScale: 3.8449

Lambda: 5.9747e-04

BoxConstraint: 4.7684

Properties, Methods

FitInfo = struct with fields:

Solver: 'LBFGS-fast'

LossFunction: 'hinge'

Lambda: 5.9747e-04

BetaTolerance: 1.0000e-04

GradientTolerance: 1.0000e-06

ObjectiveValue: 0.1006

GradientMagnitude: 0.0114

RelativeChangeInBeta: 9.3027e-05

FitTime: 0.1684

History: []

HyperparameterOptimizationResults =

SupervisedLearningBayesianOptimization

ObjectiveFcn: @createObjFcn/inMemoryObjFcn

VariableDescriptions: [5×1 optimizableVariable]

Options: [1×1 struct]

MinObjective: 0.0484

XAtMinObjective: [1×3 table]

MinEstimatedObjective: 0.0512

XAtMinEstimatedObjective: [1×3 table]

NumObjectiveEvaluations: 30

TotalElapsedTime: 26.8064

NextPoint: [1×3 table]

XTrace: [30×3 table]

ObjectiveTrace: [30×1 double]

LossFun: 'classiferror'

LossTrace: [30×1 double]

ConstraintsTrace: []

UserDataTrace: {30×1 cell}

ObjectiveEvaluationTimeTrace: [30×1 double]

IterationTimeTrace: [30×1 double]

ErrorTrace: [30×1 double]

FeasibilityTrace: [30×1 logical]

FeasibilityProbabilityTrace: [30×1 double]

IndexOfMinimumTrace: [30×1 double]

ObjectiveMinimumTrace: [30×1 double]

EstimatedObjectiveMinimumTrace: [30×1 double]

For big data, the optimization procedure can take a long time. If the data set is too large to run the optimization procedure, you can try to optimize the parameters using only partial data. Use the datasample function and specify 'Replace','false' to sample data without replacement.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

Standardizing predictors before training a model can be helpful.

You can standardize training data and scale test data to have the same scale as the training data by using the

normalizefunction.Alternatively, use the

Standardizename-value argument to standardize the numeric predictors before training. The returned model includes the predictor means and standard deviations in itsMuandSigmaproperties, respectively. (since R2023b)

After training a model, you can generate C/C++ code that predicts labels for new data. Generating C/C++ code requires MATLAB Coder™. For details, see Introduction to Code Generation for Statistics and Machine Learning Functions.

Algorithms

fitckernelminimizes the regularized objective function using a Limited-memory Broyden-Fletcher-Goldfarb-Shanno (LBFGS) solver with ridge (L2) regularization. To find the type of LBFGS solver used for training, typeFitInfo.Solverin the Command Window.'LBFGS-fast'— LBFGS solver.'LBFGS-blockwise'— LBFGS solver with a block-wise strategy. Iffitckernelrequires more memory than the value ofBlockSizeto hold the transformed predictor data, then the function uses a block-wise strategy.'LBFGS-tall'— LBFGS solver with a block-wise strategy for tall arrays.

When

fitckerneluses a block-wise strategy, it implements LBFGS by distributing the calculation of the loss and gradient among different parts of the data at each iteration. Also,fitckernelrefines the initial estimates of the linear coefficients and the bias term by fitting the model locally to parts of the data and combining the coefficients by averaging. If you specify'Verbose',1, thenfitckerneldisplays diagnostic information for each data pass and stores the information in theHistoryfield ofFitInfo.When

fitckerneldoes not use a block-wise strategy, the initial estimates are zeros. If you specify'Verbose',1, thenfitckerneldisplays diagnostic information for each iteration and stores the information in theHistoryfield ofFitInfo.If you specify the

Cost,Prior, andWeightsname-value arguments, the output model object stores the specified values in theCost,Prior, andWproperties, respectively. TheCostproperty stores the user-specified cost matrix (C) without modification. ThePriorandWproperties store the prior probabilities and observation weights, respectively, after normalization. For model training, the software updates the prior probabilities and observation weights to incorporate the penalties described in the cost matrix. For details, see Misclassification Cost Matrix, Prior Probabilities, and Observation Weights.